Scottish Independence Referendum Live Blog

Join us for our live daily blog of the Scottish referendum. We’ll be bringing you all the reaction live from the trading floor, as well […]

Join us for our live daily blog of the Scottish referendum. We’ll be bringing you all the reaction live from the trading floor, as well […]

Join us for our live daily blog of the Scottish referendum. We’ll be bringing you all the reaction live from the trading floor, as well as analysis from City Index’s Ashraf Laidi, Joshua Raymond, Ken Odeluga and more.

This page doesn’t update automatically. Hit the refresh button on your browser or F5 on your keyboard to keep completely up-to-date.

That’s it from our Live Scottish Referendum blog. We hope you’ve enjoyed keeping up-to-date with our stats and stories throughout this historic week in UK politics.

Alex Salmond is to step down as Scotland’s First Minister. He said: ““We lost the referendum vote but Scotland can still carry the political initiative. For me as leader my time is nearly over but for Scotland the campaign continues and the dream shall never die.”

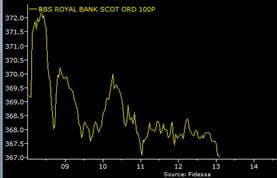

City Index’s Michael Wills: “Scottish based blue chips are still broadly positive following the referendum as was expected. However we’ve seen gains in these shares ease from their highs earlier, most of the below are now trading at or close to daily lows. The RBS chart below is fairly typical of UK equities after the first half of trading today. Not necessarily characteristic of any negative sentiment, most likely the drop is a result of profit taking.”

Nick Serff, City Index’s Senior Market Maker for Indices: “FTSE still undecided what to do after Scotland voted to remain part of the United Kingdom. Trading has remained in a tight sideways range since the opening rotations, with trading a lot more subdued after the earlier volatility. UK government bonds yields are trading a touch lower and Sterling has pulled back off its overnight highs, now trading down on the day at 1.635 against the dollar. Elsewhere, the DAX and Spain’s IBEX have come under pressure, giving back their earlier gains on news story’s out of Catalonia that the Catalan independence bid won’t be slowed by the Scottish result.”

Ken Odeluga, City Index’s Market Analyst:”A rally in UK stocks following news that Scotland voted ‘No’ in Thursday’s independence referendum has eased off somewhat, with the market apparently unwilling to push major shares too close to multi-year highs.

The UK’s benchmark FTSE 100 index traded as high as 6872.82 this morning, an 0.8% gain, which in itself was quite modest.

However the index is now trading about 0.7% higher having eased its gain on the day to as little as 0.5% a while ago.

Financial stocks are by far and away the sector making the most gains.

Shares of Lloyds Banking Group, and Royal Bank of Scotland, two of Britain’s largest banks with strong historical and continuing links to Scotland, traded around 2% and 3% firmer respectively.

Their managements had come out strongly in support of the ‘No’ vote in recent weeks.

They were particularly concerned about the risk of disruption to the UK’s financial system from a vote in favour of Scottish independence bearing in mind separatist leaders’ demands for currency union using the pound, whilst English politicians were emphatically against one.”

Nick Serff, City Index’s Senior Market Maker for Indices: “The ‘no’ vote bid still remains in the FTSE currently trading up 0.65% at 6863. However, the market hasn’t yet managed to regain the levels seen overnight on the futures market. At one stage the pre-opening call for the cash market was as high as 6900, matching the high seen at the beginning of the month. Where next is going to be the big question? Do we push back down and fill the overnight gap, or push higher and have a look at those early September highs?”

Ashraf Laidi, City Index’s Chief Global Strategist: “Scotland ‘no’ shadowed by JPY and USD strength

Scotland’s rejection of independence, by 55% to 45%, initially boosted sterling and the FTSE, while dragging gilt yields, with the bulk of these developments occurring in the aftermath of the preliminary results. But as the results were finalized about two hours before the London open, GBP gains waned across the board to the benefit of the yen and the dollar.

Comments from Japanese economy minister Akira Amari stating that “abrupt moves in currencies are not good” capped the yen’s gains, especially as ministers set to meet at this weekend’s G20 meeting in Sydney. Broad yen fluctuations have usually proven contentious ahead of G7 meetings, when ministers are likely to warn of Japanese devaluation or Tokyo complaining of excessive strength in its currency.

The lingering question of devolution will only become a matter of concern as we approach the pre-budget announcement in December, after which more pertinent decisions are made in spring leading to the UK elections.

FX traders will shift focus away from fear of the unknown towards more macro elements such as the erosion of slack in labour markets and the pace of recovery in real earnings.

GBP/USD is up 2.8% since plunging after the only poll showing a Yes majority 2 weeks ago, but re-emerging USD strength may cap cable at the 2-month trend line resistance. An unlikely breakout (close) above 1.6440s could encounter the next barrier at 1.6520, coinciding with the 55-week moving average. A revisit towards 1.6200 is not ruled out later this month as the Fed sets to exit QE3.”

Neil Looker, City Index’s Chief Forex Dealer: “My personal view is that Scotland can thank Rupert Murdoch and his YouGov poll, which 3 weeks ago revealed a 52% lead for the ‘yes’ campaign, subsequently sending the pound crashing and politicians heading north with an open cheque book.”

For the rest of Neil’s daily article click here.

The Financial Times’ Guy Chazan:

Our Chief Market Strategist Joshua Raymond had this to say on the open, “Even though the vote has been for no breaking of the union, this does not mean the political landscape hasn’t changed. There will be some who will still be shocked by how close the vote actually came – a margin of just 10%. This means that Alex Salmond has more power than ever before to negotiate with the UK government over a further devolution of power to Scotland. This could have far reaching consequences for UK governance and tax but in the very least, it’s the lesser of two evils to market uncertainty against a breaking of the union.

Make no mistake, Labour will be toasting this victory the most. They had so much to lose – namely 41 MP’s – and that could have had bigger consequences for their support in the next election. Still, we should not discount the 45% of voters who called to make Scotland independent as one which highlights the increased risk of UKIP stealing a large proportion of the vote in the 2015 general election next year either.

The relief rally has come – indeed it started at 10.30pm last night after the You Gov poll – and in sterling certainly its been rather short lived. There’s no surprise financials are leading the way higher in FTSE 100 trading either but the chances are this relief rally has already come and gone.”

Here’s a chart of 1 month implied volatility on the pound sterling. This chart highlights how the market perceived risk around the Scottish vote with moves higher showing nervousness in the market towards a breaking of the union. As polls over the past week eased concerns that the yes camp could win, that nervousness receded, triggering a fall in volatility.

FTSE 100 opens higher by 43pts to trade at 6863. RBS and SSE opens higher by 3%, whilst Weir also gains 2.5% in early trading.

10 minutes until the UK market opens. Joshua Raymond tells us that he expects a 2% move higher for Lloyds and RBS.

Here’s a chart of GBP/USD and EUR/GBP showing an inverse relationship between the two currency pairs as sterling strength continues.

Giles Watts, Head of Equities at City Index “should see UK banks pushing higher at the open. Standard Life and some of the other financials should see a positive open. We had a few clients taking risk off their long positions in the banks yesterday ahead of the vote so I would expect they could be getting back involved at the open.”

PM David Cameron says there is “a great opportunity to change the way Britain is governed and promises to give Scotland more powers in the next parliament.” The PM will also draft laws to give Scotland more powers to be published by January.

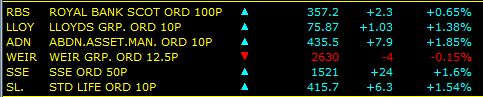

Latest prices from the trading floor:

Joshua Raymond, Chief Market Strategist, “We are seeing some strong gains in the pound sterling as the data started to confirm that there will not be a breaking of the union. Whilst some of early relief rally momentum in the pound has waned, more volumes will come through at 7am so it could get a second wind. The FTSE 100 is called to open higher by more than 70pts right now.”

Results continue to come in thick and fast with the ‘no camp’ set for victory

The no camp is seemingly on route for victory with most local authorities calling that Scotland has decided no.

We are expecting some of Scotland’s 32 local authorities to declare a result before 3am but most of the votes should be counted and released to the public by 5am tomorrow morning. Our team of analysts will be joining us back in on the trading floor bright and early to bring you how the markets are reacting to the result as Scotland decides. Keep an eye for our analysts on Twitter via @alaidi, @Josh_Cityindex and @ken_Cityindex for the latest developments.

Here’s the latest chart of the GBP/USD forex pair. GBP strength has deterioated a tad over the past hour or so.

Joshua Raymond, City Index’s Chief Global Strategist, “that You Gov poll has ignited the sterling market. The pound has rallied strongly and quickly as soon as it came out with the GBP/USD pair hitting a high of $1.6459. The pound has also hit a two-year high against the euro, with the EUR/GBP cross rate hitting a low of €0.7848.”

A final You Gov poll tracking 1,800 Scottish voters AFTER they have voted has resulted in a 54% victory for the ‘no camp’ with the ‘yes camp’ securing 46% of the vote. Whilst its still too early to call a formal victor and the You Gov poll has only tracked a mere 1,800 voters, it has sent a signal to the markets that the ‘no camp’ is on track to victory.

City Index’s Michael Wills: “Not much change at the end of the day for Scotland-based FTSE 100 firms. Further gains stifled by the uncertainty of tomorrow’s referendum result. European and US indices push on stronger in comparison. A rather flat afternoon for many British shares, was this the quiet before the storm tomorrow morning?”

Ashraf Laidi, City Index’s Chief Global Strategist: “No “buy on the news” rally in GBP after a “Yes” vote

Those expecting the pound to end up rallying in the event of a “Yes” on the basis of “sell of the rumour-by-the-fact” ought to think twice. A “yes” vote would be a shock to say the least, and a resulting sterling plunge is inevitable due to:

i) Uncertainty of Scotland’s paying of its union-debts may force the BoE to guarantee Scottish debt;

ii) Loss of oil revenues to England;

iii) Doubts over England’s path towards fiscal rectitude;

iv) Eroding chances of a 2015 rate hike from the BoE;

v) Political uncertainty in Westminster ahead of May 2015 elections and in the period following Scotland’s actual independence, likely in 2017

vi) Uncertainty over UK nuclear security if Scotland shuts down missiles and submarines in the river Clyde.

But any damage from a plunging sterling would be allayed in the long run by a boost to England as a place of business, as Scottish banks and financial services firms seek refuge to the certainty of London. Scotland’s exit from the union could be seen to be relieving the UK Treasury of public finance burden to Scotland.”

Ashraf Laidi, City Index’s Chief Global Strategist: “No other way but sterling for an independent Scotland

An independent Scotland will adopt sterling, whether the Bank of England wants it or not. Scotland will go with GBP. There is no other way. Asking how an independent Scotland will fare with the pound without a lender of last resort is the tricky part, especially as it would have to maintain sufficient currency reserves to meet its obligations as a new state.

EU-Scotland is far from a sure thing

In order for Scotland to be able to adopt the euro it would require acceptance by each of the 28 members of the European Union. Will each member accept a country that has just refused to repay its debt portion when it was an EU member? Although European Commissioner Juncker said the EU would not take any new members and “consolidate what has been echoed among the existing 28” nations, Brussels officials sought to calm nervousness in Scotland by explaining that Juncker was referring to new entrants from the Balkans and that Scotland was a “special case”. Juncker’s predecessor, Barroso, said it would be “very difficult if not impossible” to secure entry from all 28 members.”

Joshua Raymond, City Index’s Chief Market Strategist: “The pound sterling is now on track for its biggest one day gain against the US dollar. Guess the market is already toasting a victory for the no camp. I’d rather wait until we hear some more exit polls but it would appear the relief rally in sterling has already begun.”

Wondering why broadcasters are so quiet on #indyref today? Ofcom’s referendum rules, of course:

City Index’s Michael Wills: “Scotland-based FTSE 100 companies are for the most part positive at midday today. The UK Index is still lagging behind its European and US peers running into the referendum. However, positive equity sentiment is still holding up here. The ‘No’ campaign’s marginal lead seems to be reassuring investors somewhat.”

The final poll from Ipsos MORI shows a slight change from many of yesterday’s results, with 53% in the ‘no’ camp and 47% saying ‘yes’. A staggering 95% of people say that they will be turning out to vote today.

Here’s the expected timeline for the results announcement. It’s going to be a long night:

Former Federal Reserve Chairman, Alan Greenspan: “There’s no conceivable, credible way the Bank of England is going to sit there as a lender of last resort to a new Scotland.”

Rupert Murdoch and Alex Salmond have met on average every two months since May 2007, according to Private Eye. With the Scottish Sun and its English sister running opposing viewpoints on the #indyref it will surely be the Sun wot won it, no matter what the result.

Joshua Raymond, City Index’s Chief Market Strategist:”Here’s the GBP/USD pair in the last 24 hours. After the US dollar gained ground last night thanks to a rather hawkish move by the Federal Reserve, sterling buyers have re-emerged this morning on hopes of a victory for the no camp. The last 24 hours has seen a 100 pip range. Expect much more GBP volatility as exit polls start to come out throughout the day.”

Kit Juckes , Global Head of FX Strategy at Société Générale: “Slightly hungover in Paris, where ‘Le Schadenfreude’ seems to have local press rooting for a Scottish ‘Yes’.”

And let’s not forget, it’s not just the Scottish Referendum that traders are waking up to this morning. Last night was the hotly anticipated FOMC decision which triggered swings in the US dollar and US stocks. Here’s an article from Chief Global Strategist Ashraf Laidi explaining how the FOMC triggered a rallying trifecta in stocks, US dollar and yields.

The UK 100 (FTSE 100) has opened rather flat this morning with most asset classes treading water until investors have a better idea of how the exit polls are trending. We could start to see an increase in volatility as the day progresses and exit polls start to indicate how close the vote might be.

And the day has finally arrived. Welcome to our live blog as Scottish voters hit the polling stations to decide whether Scotland will remain within the union or not. We will be bringing you live updates from the markets and analysis from our experts throughout the day to keep you informed of the latest developments.

That’s all from us on the final day before the historic Scottish referendum. Join us again tomorrow morning for all the opinion and reaction from the trading floor.

Ashraf Laidi, City Index’s Chief Global Strategist: “Which GBP rebound? As the Scottish referendum looms close and GBP extends its rebound on the majority of polls indicating a steady lead for the “No” camp, these charts indicate the preferred currencies against which sterling gains is most likely to be amplified (in the event of a ‘No’ vote), namely CHF and NZD. Even if the Swiss National Bank does not cut interest rates at Thursday’s meeting, it could well make the case for further CHF selling if it reiterates the threat to: intervene in FX markets, remain on easing alert into subsequent meetings and issue lower forecasts for inflation. In the case of NZ, most economists have cut their forecasts for Fonterra’s 2014-15 payment to dairy farmers. Fonterra is NZ’s leading dairy company and the world’s largest exporter of dairy products. Adding Russia’s ban on food imports and weakening demand for dairy products, further declines in dairy products will likely extend Kiwi’s downward spiral.”

Ken Odeluga, City Index’s Market Analyst: “The Scottish independence vote tomorrow is a massive deal which will have far-reaching effects. The sterling market is aware of this and has responded to the political rhetoric from leaders of ‘yes’ and ‘no’ camps, demanding a currency union and denying one will be forthcoming, respectively.

But is the market panicking?

Not as such.”

Read Ken’s “Sterling market shows little sign of panic ahead of vote” article here.

The latest poll from Panelbase shows the same seemingly static 52% for ‘no’ and 48% for ‘yes’. How long can this too-close-to-call polling last?

Joshua Raymond, City Index’s Chief Market Strategist: “It should not be ignored that this referendum has the ability to dramatically change the governing landscape of the UK. Labour has 41 MP’s in Scottish constituencies. Labour absolutely have the most to lose politically from a yes vote. With recent UK polls for the 2015 general election showing both the Conservatives and Labour are neck and neck with around 34% of the vote each, we could see another hung parliament or minority government. In that case, the Conservatives may seek to call another election in 2016 if a yes vote sees Labour lose its 41 Scottish MP’s.”

Neil Looker, City Index’s Chief Forex Dealer: “Scottish independence polls released overnight caused further volatility to the proud pound as ICM originally reported a 52% outcome for the ‘yes’ campaign only to correct it to ‘no’ a few minutes later as polls from Opinium and Survation reflected the exact same outcome of 52% for the no vote.”

Read the rest of Neil’s latest article here.

Not too long ago Gordon Brown and David Cameron were trading blows at PMQs, now it seems they’ve forged an unlikely friendship in the heat of the #indyref debate, according to the Evening Standard.

David Cameron continues to make the case for a ‘no’ vote, although he admits he’s nervous ahead of Thursday’s poll. Speaking earlier today, he said: “Everyone who cares about our United Kingdom, and I care passionately about our United Kingdom, is nervous. But I’m confident we’ve set out how Scotland can have the best of both worlds – a successful economy with a growing number of jobs.”

Ashraf Laidi, City Index’s Chief Global Strategist: “GBP is a little firmer after last night’s polls and today’s jobs figures, with all measures of GBP options volatility currently pushing lower.

UK unemployment hit a fresh six-year low at 6.2% in the three months ending in July, from 6.4%, exceeding expectations of a 6.3% print. Separately, jobless claims dropped 37,200 in August, exceeding the 30,000 decline expected by the market. This means the number of unemployed people has fallen below 1 million for the first time since September 2008.

A 0.6% July increase in the highly scrutinized earnings figure was another positive element to the jobs figures, following a shock 0.1% contraction in June. But these figures meant real earnings (earnings minus inflation) remained negative at -0.8%, which confirmed that the Bank of England was unlikely to raise rates before February or March 2015.

GBP showed a short-lived rally to the jobs figures mainly due to the fact that real earnings remained negative.

Overnight, GBP remained muted to both the ICM and Survation polls, showing the ‘yes’ campaign leading with 52% versus 48% for the ‘no’, excluding undecided voters.

This month’s Bank of England minutes acknowledged rising volatility in the exchange-rate as investors “became more uncertain about the outcome of the referendum.”

Former Treasurer of the Conservative party, Lord Ashcroft, with a nod to the bookies’ prices:

Scotland’s first home-grown billionaire, Sir Tom Hunter, has been speaking to the BBC about his concerns should Scotland leave the union and have to argue its case to remain a part of the pound. He said: “I’ve got every faith in Alex Salmond, he’s a very good negotiator, but he would not have a very strong hand to negotiate. I think if anybody thinks in those circumstances the Bank of England is independent, they are living in cloud cuckoo land.”

SNP Finance Secretary, John Swinney, comments on the latest Scottish unemployment figures, which saw a fall of around 15,000 from May to July. He said: “These figures are a massive boost to the ‘Yes’ campaign. They are a huge vote of economic confidence in Scotland’s future and expose the scaremongering of the ‘No’ campaign. We now have the highest employment on record and unemployment, while still too high, is falling steadily.”

Ashraf Laidi, City Index’s Chief Global Strategist: “Even if Scotland ends up rejecting independence from the UK, we can’t rule out a massive surge in UK and global volatility during the plethora of exit polls, projections and corrections taking place on Thursday night into Friday late morning.

Stocks may decline as much 3% to 5% in a single day, bond yields could lose 6 to 10 basis points & yen surges alongside the USD by 2 to 4% versus high risk FX. This would be especially the case as the broadest margin between the “yes” and “no” camp is currently as little as three points.”

Ashraf warned of “A shock week in equities” last week. Will he be proved right?

Joshua Raymond, City Index’s Chief Market Strategist: “Those three polls overnight has triggered some sterling buying this morning with investors starting to think (once again) that the previously unthinkable won’t happen. But a 4p