January 21, 2021 2:59 PM

SARB leaves rates unchanged amid new variant of coronavirus: USD/ZAR, GBP/ZAR

Little is discussed regarding the effect of the coronavirus (and its variant) on the South African economy. Earlier today, the South African Reserve Bank (SARB) left rates unchanged at 3.5%, a record low. The central bank had cut interest rates by 300 bps over the last year, however the decision makers determined that risks to growth and inflation were balanced, despite South Africa having 1.3 million coronavirus cases of its own, including a new variant strain which is said to be 50% more infectious. Additionally, the richest country in Africa has yet to roll out vaccines, saying that they will begin vaccinating people in the first half of 2021! Do Rand traders agree with the SARB?

USD/ZAR had put in an all time high on April 6th, 2020 at 19.3390. Since then, the pair has been moving steadily lower and put in a recent low near 14.5050 on January 4th, which is near pre-pandemic levels. USD/ZAR bounced to a downward sloping trendline from the April highs near 15.6610 on January 11th and began moving lower again.

Source: Tradingview, City Index

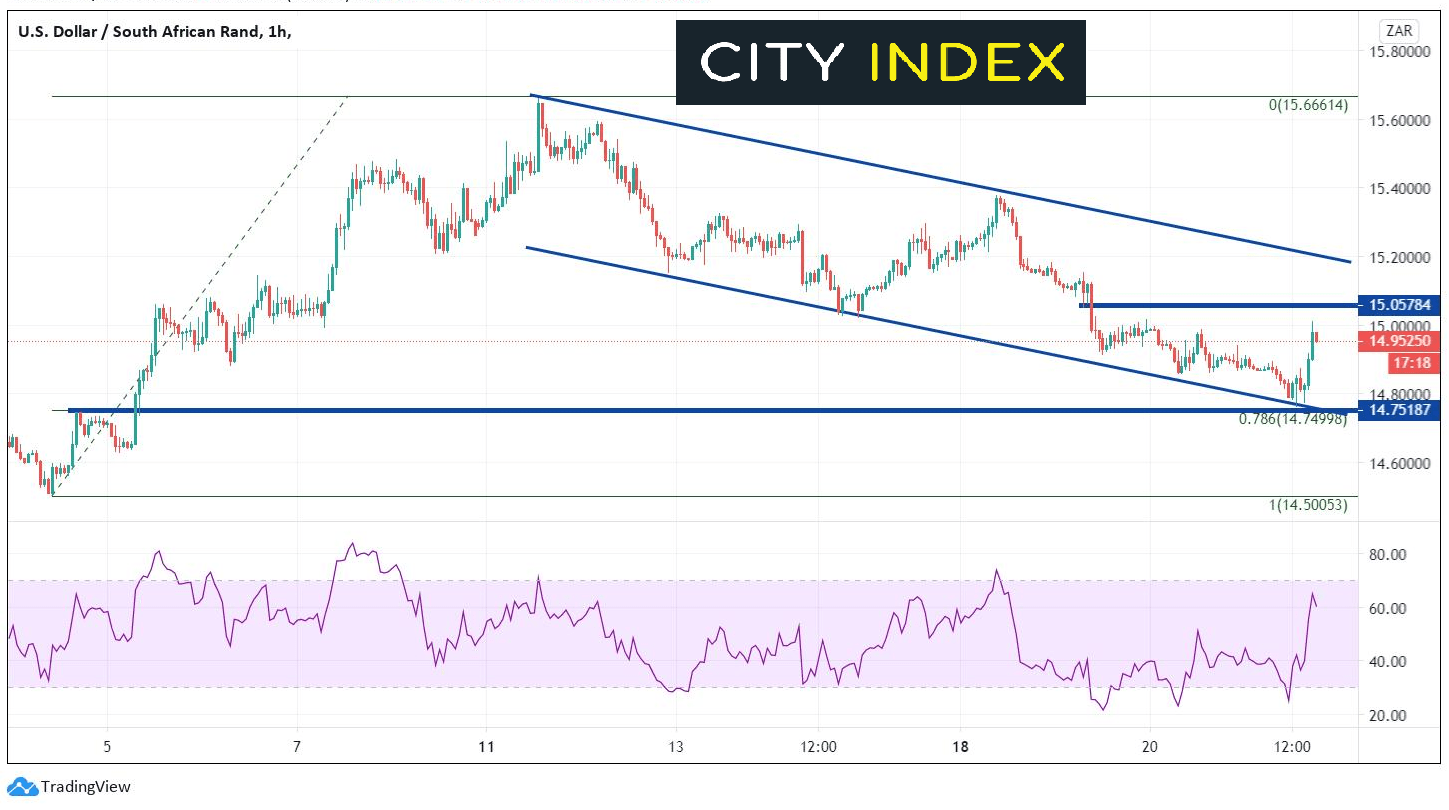

On a 60-minute timeframe, the pair USD/ZAR has been moving in a downward sloping channel and retraced to the 78.6% Fibonacci level from the lows of January 4th to the highs of January 11th, near 14.7500. This level confluences with horizontal support and short-term trendline support. After the SARB announcement, the pair bounced. First horizontal resistance above is at 15.0525. If price can move above there, sellers will be sitting at the top trendline of the downward sloping channel near 15.2000. Support is back at today’s lows near 14.7500, then the January 4th lows near 14.5000.

Source: Tradingview, City Index

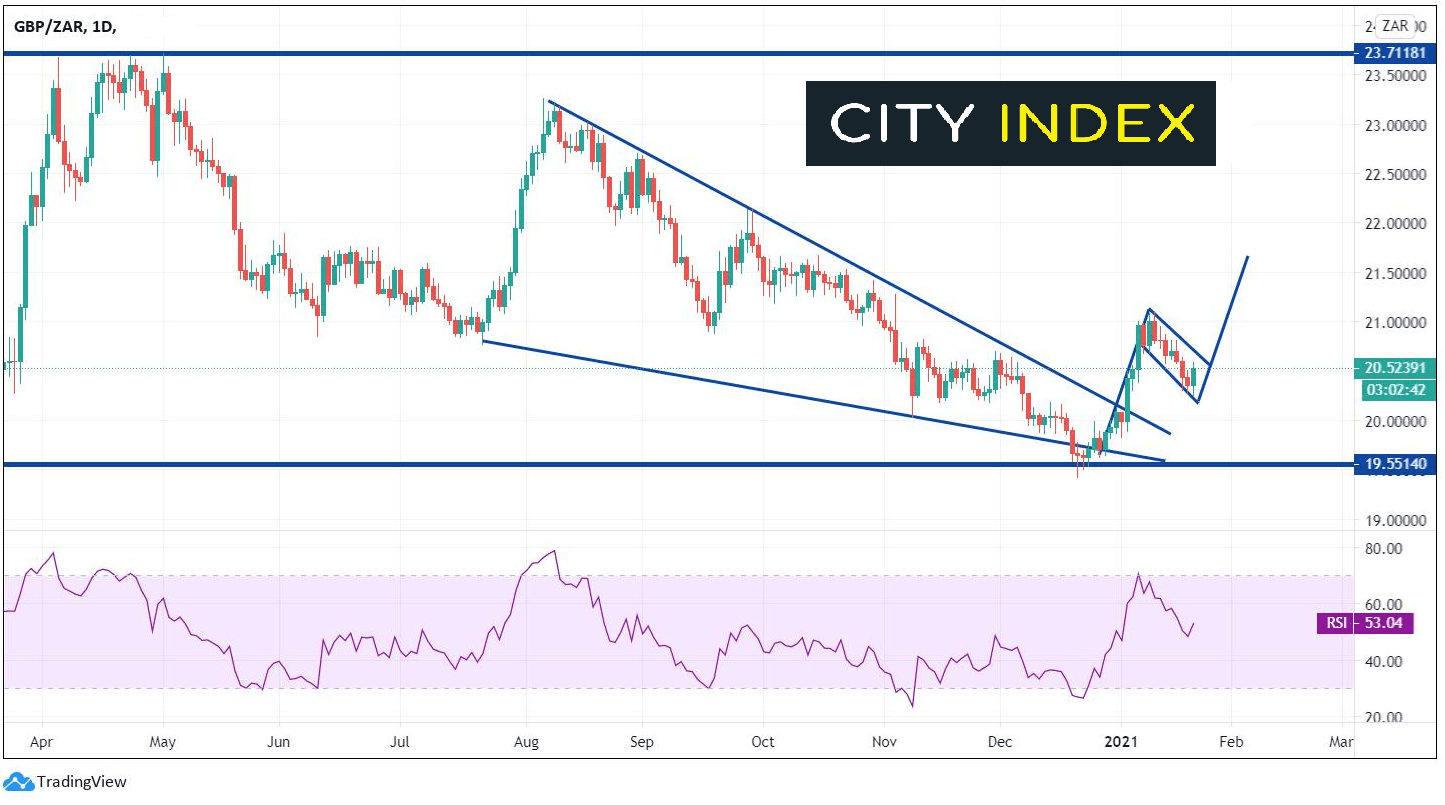

GBP/ZAR has followed a similar path to USD/ZAR, however, with more volatility! After peaking in April near 23.7118, the pair moved lower and had a large bounce in July. From there, the pair moved lower towards support at 19.5514, forming a descending wedge. GBP/ZAR put in shooting star reversal candle on December 21st at the support level, forming a false breakdown below the bottom trendline of the wedge. Price then reversed and broke out higher above the descending wedge (as one would expect) and is currently forming a flag pattern near 20.5250.

Source: Tradingview, City Index

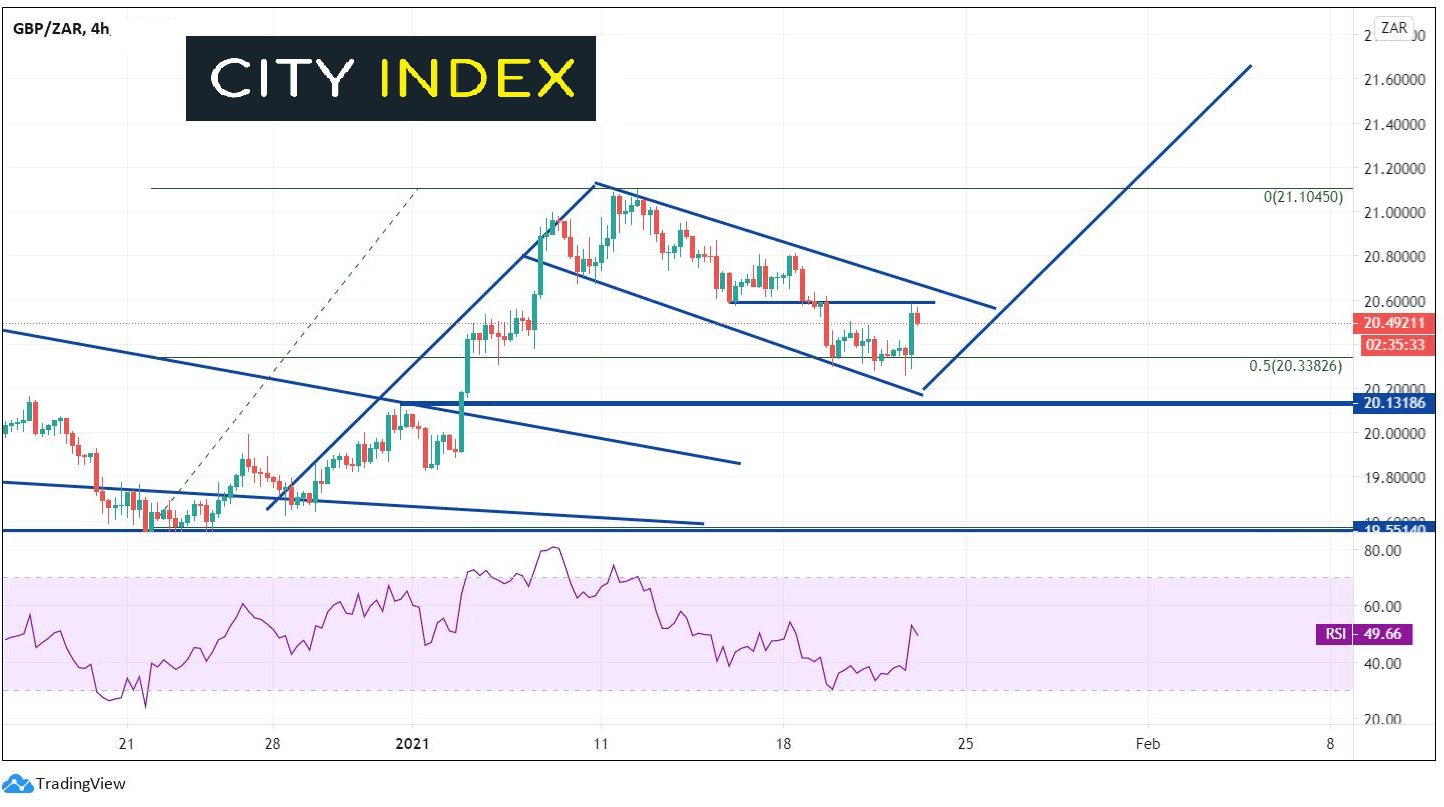

On a 240-minute timeframe, price pulled back to the 50% retracement from the January 11th highs to today’s lows near 20.2900 and bounced. GBP/ZAR is trading near current short-term resistance near 20.5768. Just above there is the top downward sloping trendline from the flag near 20.6575. On a breakout of the flag pattern the target is near 20.6550, however the pair must first get past the January 11th highs resistance at 21.1045. Today’s low acts as first support near 20.3860. Below there, bulls will be waiting at the bottom trendline of the flag and horizontal support near 20.1318.

Source: Tradingview, City Index

Although South Africa is going through grave problems with the coronavirus and its own variant, the SARB feels that risks are balanced current interest rates at 3.50% are appropriate. If South Africa continues to have trouble with the variant, perhaps more accommodation may be necessary. Watch for headlines related to the South African variant the ability for the country to obtain the vaccine.

Learn more about forex trading opportunities.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM