Sainsbury s review earnings come amid heightened anticipation

Sainsbury’s CEO created quite a potential rod for the supermarket group’s back (and his) just over a month ago. That’s when the group announced a […]

Sainsbury’s CEO created quite a potential rod for the supermarket group’s back (and his) just over a month ago. That’s when the group announced a […]

Sainsbury’s CEO created quite a potential rod for the supermarket group’s back (and his) just over a month ago.

That’s when the group announced a wide-ranging strategic review after reporting a sales slump thatpushed the retailer’s shares to a six-year low and down dragged sector peers too, when they were already under pressure from Tesco’s debacle.

The third-largest supermarket chain by market share also cut sales forecasts for the year, to an expectation of a 2% fall having previously seen a small increase.

But the idea of a strategic review that would leave “no stone unturned”, according to Sainsbury’s CEO Mike Coupe, raised some eyebrows in The City.

After all, Coupe was a colleague of former CEO Justin King from 2004 onwards, present for the entire tenure of his former boss, and seven years of that as a board member.

That begged the question of why, precisely, Coupe needed a strategic review.

The answer may of course be that Coupe didn’t.

But the market perhaps did.

The review could be, at least partly, a wily PR exercise, with an outcome which the initiator had a fair idea of before setting it in motion.

There is a risk it could backfire, but either way, it’s not the only challenge facing Sainsbury’s ahead of its half-yearly interim results to be released on Wednesday 12th November.

The scene is set for a Sainsbury’s update with two broad themes: the unveiling of the strategic review and announcement of latest earnings and forecasts.

That’s where the straightforward forecasts end though.

Beyond the basic earnings, wider and deeper expectations for Sainsbury’s are bound up in the tortuous fortunes currently assailing the UK’s established grocers.

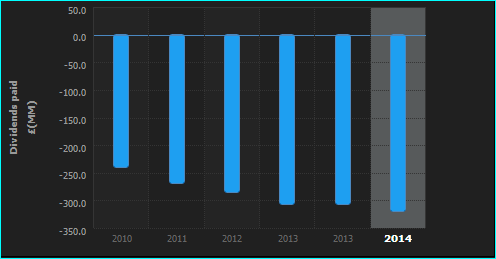

First and centre among these: the dividend.

With increasing difficulty in evaluating the UK’s major retail stocks on a price-to-earnings basis, dividend yields have become an important means of deciding whether to hold supermarket stocks or not.

This isn’t just Sainsbury’s problem, naturally: but, again, it’s an even more closely-watched aspect of Sainsbury’s earnings because 1. For several years Sainsbury’s has been increasing annual pay-outs at a fair rate of knots.

Source: Thomson Reuters

2. CEO Coupe made a point of including Sainsbury’s generous dividend policy in its strategic review.

“You’d expect the dividend to be part of that full-scale review,” he said in October.

Unfortunately, it’s only too easy to be pessimistic about how the review will affect the dividend, because Sainsbury has clear guidelines.

Last fiscal year dividends per share were 17.3p, with coverage of 1.9 times EPS.

But the supermarket has pledged to keep ordinary dividend cover at least 1.5 times underlying EPS.

With the fall in underlying EPS forecast accelerate to around 37% in the first half of 2015, dividends probably need to be reduced sooner.

Market consensus currently expects the dividend for the full year of 2015 to be slashed 25.7%.

And there is more than a risk cuts could begin in the current interim.

A cut of around 30% for this interim to 3.5p compared to 5p at the last first half would be commensurate to the full-year cut expected for next year.

Sainsbury’s shares, like those of most other major UK retailers have enjoyed a bounce from the significant sell-off seen in the autumn—the selling was partly fuelled by Tesco’s various shockers, and partly down to wider sector challenges.

But Sainsbury’s stock alone has since recovered by more than 20% off lows of 223p in mid-October, to stand this evening at 269p.

It has to be said though, as Sainsbury’s results have drawn closer, trading in the stock has taken on the type of optimism which seems faintly brittle.

Below we have charted the variance (AKA ‘volatility’) of half-hourly trading intervals.

We can see two clear spikes in the last few days which suggest two sharp increases in reactiveness, or even ‘nerviness’.

If that is an underlying quality which has increased of late, perhaps we should expect sharp spikes (up or down) in the stock in the event of significant developments tomorrow.