Sainsbury s in spotlight as retail shares show signs of life

Sainsbury’s set the cat among the retail pigeons last week with a surprising play for Home Retail Group. But attention is swinging back to the […]

Sainsbury’s set the cat among the retail pigeons last week with a surprising play for Home Retail Group. But attention is swinging back to the […]

Sainsbury’s set the cat among the retail pigeons last week with a surprising play for Home Retail Group.

But attention is swinging back to the industry’s ‘bread and butter’ of sales performance this week, and it’s uncertain whether there will be any let-up in the gloom.

That said there have been some surprises so far in the UK’s retail update season.

On Tuesday, Britain’s No.4 supermarket by market share, Morrisons, posted its first underlying sales growth since 2012.

And C-Suite and General Merchandise upheaval aside, Marks & Spencer’s comparable food sales have grown for 25 consecutive quarters, including in Q3 2015/16 reported last week.

Ignoring for the moment widespread scepticism about the type of ‘growth’ posted by Marks and Morrisons (fractions of percentage points) it looks like some retailers are beginning to find formulas to inch forward against the grain.

As well, growth in real terms suggests it would be incorrect to attribute this progress to the other over-used retail industry fall-back in recent years, discounting.

Dozens of names from Debenhams, to Next, to Carphone Warehouse and others have begun to withdraw from an over-reliance on promos, turning more selective about ‘investment in price’.

It hasn’t quite worked (yet) for Next (or Marks).

Blame the weird winter weather.

Though Next is budgeting for full-price 2016-2017 sales growth of 1%-6%.

By contrast, Debenhams outshone both on Tuesday.

It reported underlying sales for the 19 weeks to 9th January up 1.9%, beating a forecast rise of 0.3%.

It cited a combination of weaning itself off seemingly interminable ‘sales’ and tweaks of its product mix (perhaps at short notice, underlining that nimbleness is another quality to look out for).

The switch moved Debenhams away from winter stock to focus instead on beauty products, accessories, homeware, handbags and shoes.

Like most general retail, clothing and department store rivals though, Debenhams’ is still finding its feet online.

It lagged Britain’s biggest department store chain, John Lewis, which grew overall sales by 5.1%, against Debenhams growth of 1.8% for seven weeks to 9th January.

That was partly down to John Lewis’s industry leading 21.4% rise in web sales in six weeks ending on 2nd January.

Those sales took e-tailing to 40%-plus of John Lewis Partnership’s group total, including Waitrose.

It illustrates another change that divides the savviest UK retail transformers from the laggards.

Obviously pivoting faster online can make a big difference.

This was especially notable on Black Friday.

British Retail Consortium figures showed total sales on that day last November rose just 0.7% vs. +2.2% in 2014.

By contrast online sales of non-food products leapt by 11.8%.

Still, it’s worth keeping Internet sales in perspective.

They’re faster growing, yes.

But still just 10% of total UK retail sales, September figures from smartinsights.com suggest.

Uncertainty for the industry therefore remains high as updates from large UK consumer-facing companies rise to a deluge over the next several days.

Some of these firms still to report this week are listed below.

Please click image to enlarge

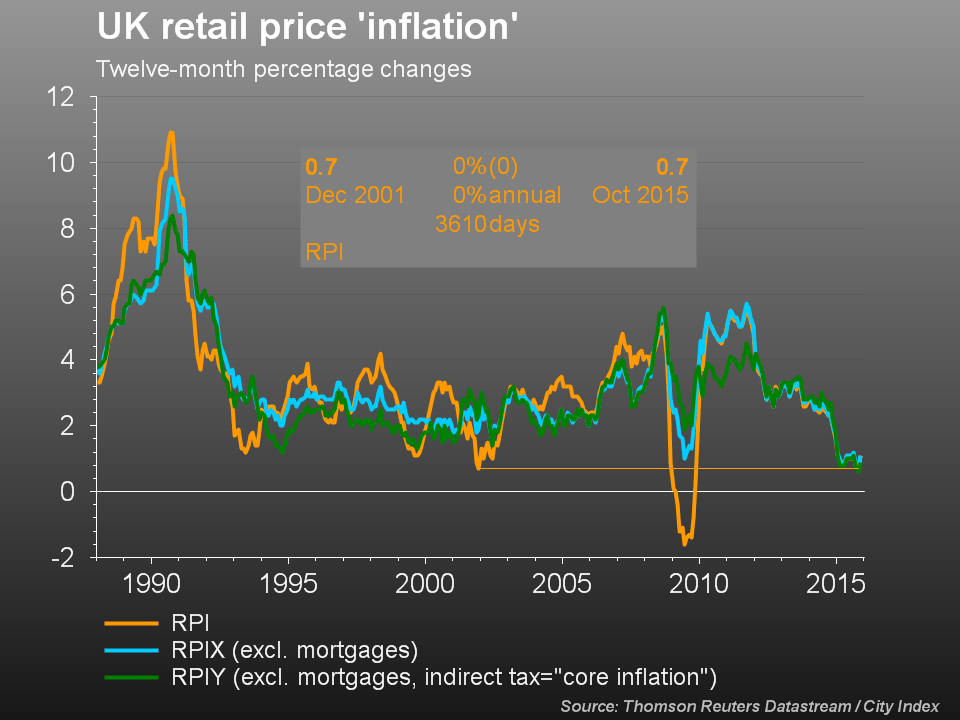

Many retailers are still widely expected to confirm that real deflation in UK food prices over the last year has seeped into the broader consumer industry.

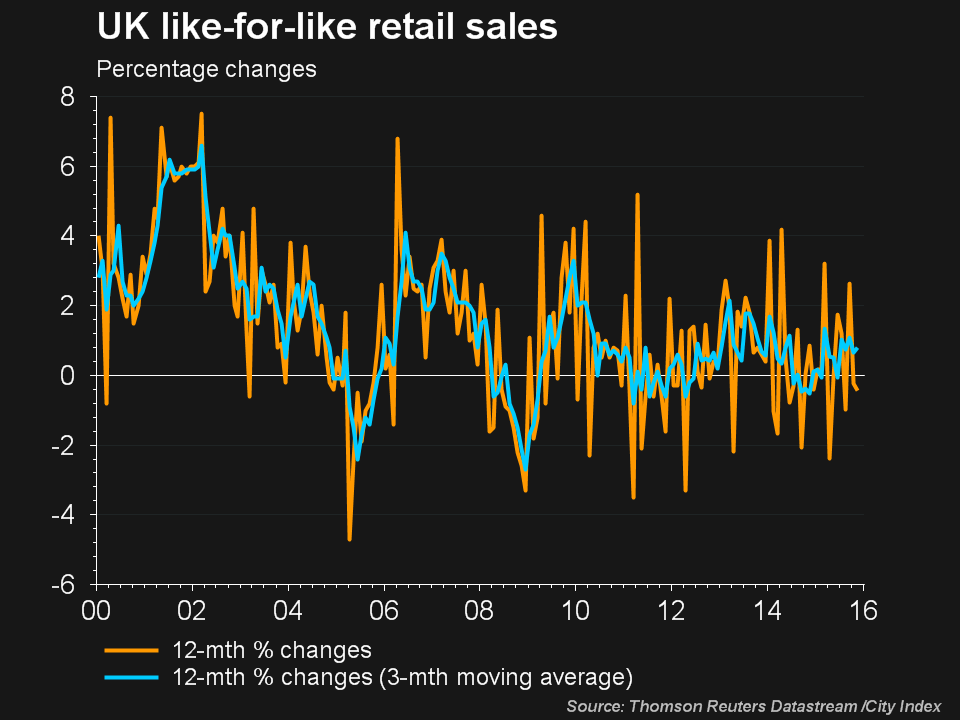

Using three-month averages of the change in like-for-like retail sales to smooth-out typical retail seasonal volatility, we see same-store sales growth recently hit similar levels to those in the second half of 2012.

A highly sensitive and somewhat China-battered UK stock market will remain becalmed this week if few further relative retail winners emerge.

On the other hand, as per Tuesday, marginal-to-moderate surprise ‘wins’ will be rewarded, somewhat disproportionately.

No. 2 supermarket’s eye-catching play for sprawling and struggling Home Retail Group, may not distract investors from close scrutiny of its Q3 update, coming on Wednesday.

The hunt for further clues as to if (or more probably when) Sainsbury’s will return with a better offer than the one HRG rejected will be on.

But with UK takeover rules mandating the supermarket ‘put up or shut up’ by 2nd February, more than a fortnight away, perhaps investors shouldn’t expect more details on top of those already offered, so soon as Wednesday.

We therefore expect investors to react more to Sainsbury’s trading than its intended M&A.

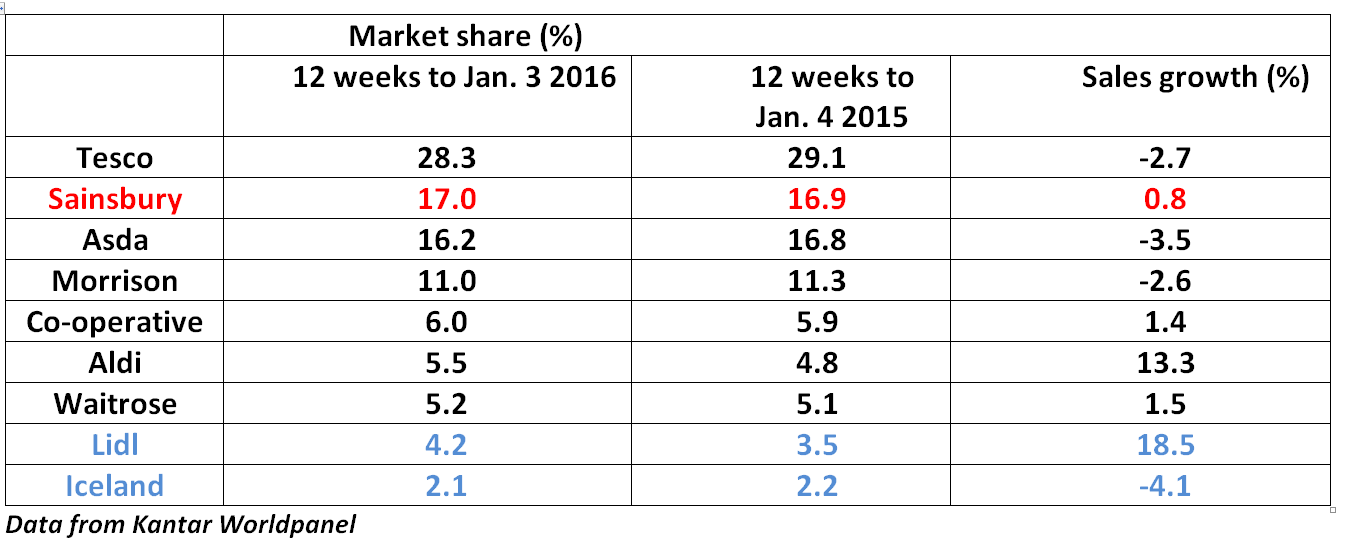

On the former, so long as its official sales match independent data, it should still be winning—at least among the ‘Big 4’.

12-weekly data from Kantar Worldpanel out on Tuesday gave Sainsbury’s its fourth-straight rise, this time by 0.8%.

Not much, but better than its closest rivals.

Kantar’s data doesn’t gel with the average market forecast of like-for-like, which sees a fall of 0.7%.

If the consensus turns out to be wrong, the stock will react accordingly.

Please click image to enlarge