Sainsbury s circled by short sellers but could squeeze higher

Updated Friday 27th February 1829 PM Sainsbury’s shareholders might be surprised to learn that at the moment, they own one of the most shorted stocks […]

Updated Friday 27th February 1829 PM Sainsbury’s shareholders might be surprised to learn that at the moment, they own one of the most shorted stocks […]

Updated Friday 27th February 1829 PM

Sainsbury’s shareholders might be surprised to learn that at the moment, they own one of the most shorted stocks on the London Stock Exchange.

Hedge funds and other big institutions have built up a bigger short position in Sainsbury’s stock than in that of any other major supermarket, according to recent FCA data.

10.5% of Sainsbury’s shares in the market were held as a short position, according to the watchdog’s data for the week ending 27th February.

This level was classified as ‘High’ by financial data firm Markit which grades short holdings in three basic categories with ‘Medium’ and ‘Low’ as the weaker.

Whilst there would be ample reasons on which to peg a build-up of selling pressure against Britain’s embattled supermarkets as a whole, why shorters have targeted the UK’s No.3 grocer isn’t entirely clear.

Broadly speaking, Sainsbury’s has performed no better or worse than its rivals in the most recent round of sales figures—its interim figures were just as mediocre as Tesco’s and Morrisons’.

All three reported that sales fell in their prior quarters, albeit not as sharply as expected, and less than in previous periods.

Tesco was the only ‘Big 3’ grocery chain to scrape out growth during a 12-week period ending on 1st February, according to figures released by market research firm Kantar World Panel, but naturally, it was an anaemic rise of just 0.3%.

Sainsbury’s itself said its third-quarter same-store sales fell ‘only’ 1.7% whilst the market had expected a fall of as much as 4.4%.

In fact, it was Morrisons that reported the worst sales for the all-important Christmas retailing season, with a 3.1% fall in the six weeks to 4th January.

But even that was still better than the average analyst forecast compiled by Thomson Reuters.

Obviously, on an absolute basis none of these were stellar performances.

Combined with an escalating price war and corporate soul-searching amongst all the big grocers, there were and are ample weaknesses for traders to exploit in the sector.

But that still leaves the question of why Sainsbury’s stock was apparently rated as the most likely of the big grocers to take a tumble that for shorters, could be potentially profitable.

The trio doesn’t differ much in terms of the amount of cash they plan to pay out to shareholders.

More to the point, none are expected to substantially increase their dividends this year, if they increase pay-outs at all.

Tesco and Sainsbury’s have warned shareholders not to expect increased pay-outs and Morrisons is not seen as likely to increase its own.

Dividend yields among the Big 3 range between 6.2% for Tesco, to 6.8% from Morrisons.

So to find clear reasons to single out the weakest for the short treatment, we may need to resort to a simple assessment of their individual relative prospects for the year ahead.

On that basis some (very) relative fundamental points against Sainsbury’s include:

But those negatives against Sainsbury’s still seem fairly moderate to me.

I can see no clear equity valuation lag between Sainsbury’s and its two biggest listed rivals, at present.

And, because all three major supermarkets are moving targets with assets and liabilities in states of fast-moving flux at the moment, teasing out credible net asset values under this scenario is problematic to say the least.

In the end, it was not entirely surprising that we had to take a peek into technical and quantitative stock analysis to catch a glimpse of the thought processes of the secretive, algorithm-backed funds that typically hold the bulk of short positions in blue-chip stocks.

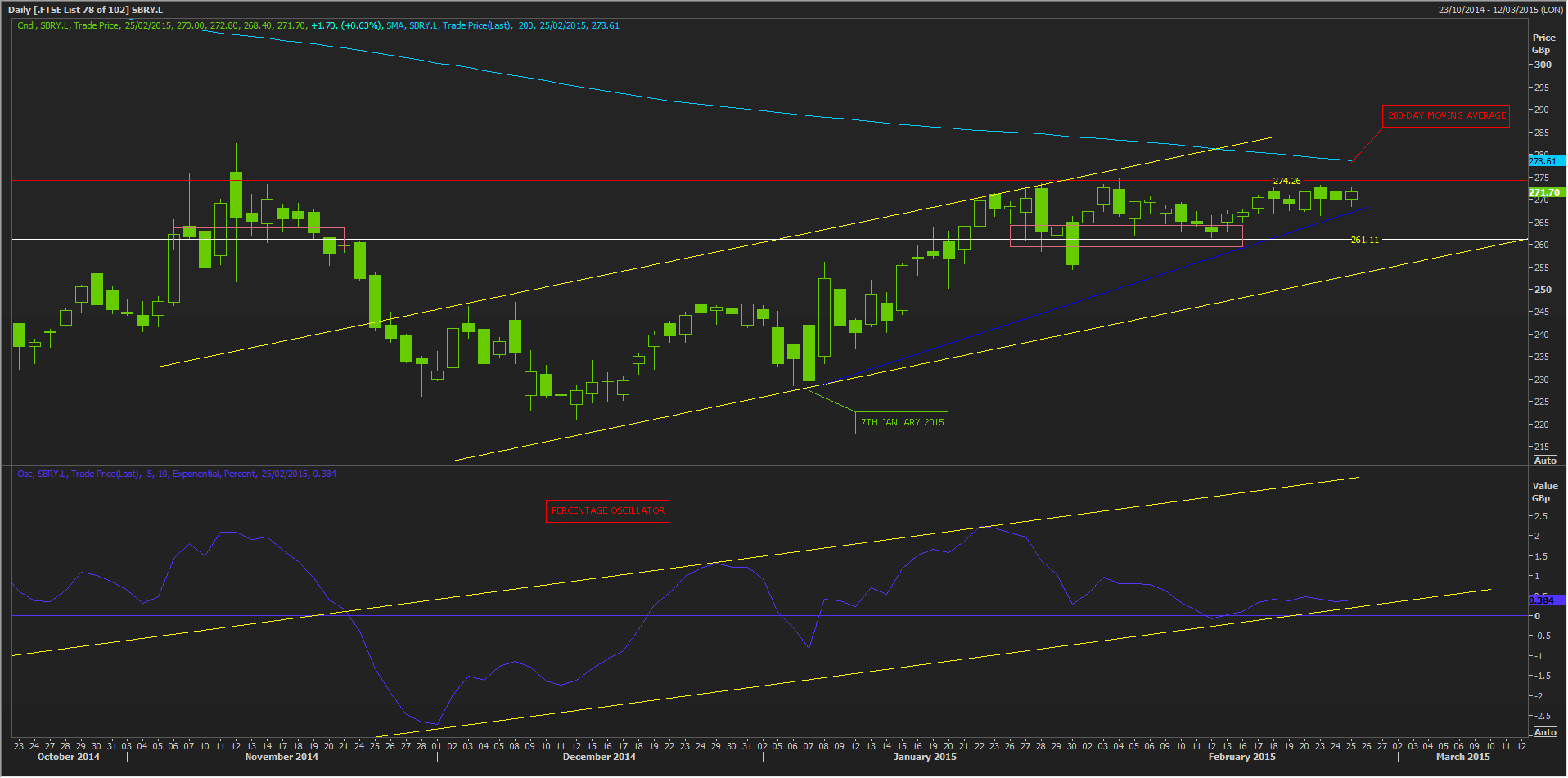

We found that whilst stocks of all three major supermarket chains took a severe thrashing last year, as discount chains bit into their grocery market share, Sainsbury’s stock is the only one still trading below its 200-day moving average, a key boundary in technical analysis.

Morrisons’ shares fluctuated close to their 200-day average five times since November 2014 and currently trade above it.

Tesco tested the level late last month and broke above it a couple of weeks ago.

But Sainsbury’s shares have not touched the 200-day gradient since December 2013.

On the quantitative side, we found Sainsbury’s and Tesco stocks recently had the highest annualized volatility of any FTSE 100 stock in the consumer sector, according to a ‘screen’ using Thomson Reuters data and analytics.

Volatility was gauged by calculating the annualized standard deviation of daily share price moves over 90 days.

This type of methodology tends to smooth-out short-term ‘noise’ and is similar to the empirical techniques deployed by quantitative analysis-based investors, many of which are hedge funds.

In our screen, Tesco’s volatility came out as the highest at 39.66%, suggesting it showed the biggest risk of an unpredictable price move.

But Sainsbury’s was second in the list of 11. Morrisons was third, spirits maker Diageo was 8th and Dettol maker Reckitt Benckiser was last.

This suggested a higher risk of unforeseen stock price moves by Tesco and Sainsbury’s when compared with volatilities of perceived ‘safer’ bets among top consumer shares.

Whilst volatility can strictly speaking be bi-directional, markets tend to regard the risk inherent in volatile assets as negative.

These results combined with the perceived ‘kitchen-sinking’ Tesco arguably underwent when it reported its strategic review, might, just, be sufficient justification to choose Sainsbury’s as the best supermarket stock to go short on right now.

Even so, we conclude the odds that Sainsbury’s stock will fall within a month are more balanced than the sizeable short position in the shares would suggest.

Additionally, Sainsbury’s short sellers face the typical risk of a ‘short squeeze’.

This happens when several try to close (or ‘cover’) their positions almost simultaneously, leading the stock to rise quickly and often significantly.

Given that the significant short position in the stock has failed to weigh on the share price over several weeks, I see the likelihood of an eventual painful unwinding of the shorts as having increased.

So whilst it’s difficult to be outright bullish on any supermarket stock at present, we disagree with the extent of bearishness required to trade Sainsbury’s stock short.

On the other hand, whilst the broader market is showing Sainsbury’s a degree of support, there do not appear to be many catalysts which could push its stock substantially higher in the immediate term.

Sainsbury’s delivery time

Up until the fourth quarter of Sainsbury’s 2013-14 year, it had been outperforming rivals, reporting nine unbroken years of sales growth with a strategy focused on own-brand products, on the quality of its food and on expanding its fast-growing convenience and online businesses.

But it followed that by posting several straight quarters of falling sales as discounters Aldi and Lidl won market share from the established grocers, consumers shopped around to save money and price war escalated.

Sainsbury’s, whose shares fell about 40% last year, said in November it would cut costs, dividends and new store openings to fund an additional investment of £150m in lower prices.

It also cautioned that it expected supermarket like-for-like sales to keep falling for the next few years.

Investors will get a chance to gauge Sainsbury’s recent progress on 17th March, when it will release a trading statement.

If it produces like-for-like sales which have fallen no faster than the 1.7% decline the supermarket reported in January, it’s likely the shares could advance.

Note, Morrisons will be the first of the Big 3 to release its spring trading update, on 12th March.

Tesco will publish preliminary results for its 2014 full-year on 22nd April.