Sainsbury s Christmas sales better than feared but still poor

Sainsbury’s has eked out a small positive from a still-overall-negative trading update covering the all-important Christmas period, with a softer sales fall than expected. This gave […]

Sainsbury’s has eked out a small positive from a still-overall-negative trading update covering the all-important Christmas period, with a softer sales fall than expected. This gave […]

Sainsbury’s has eked out a small positive from a still-overall-negative trading update covering the all-important Christmas period, with a softer sales fall than expected.

This gave shares of the UK’s third-largest supermarket chain a lift in the morning, but it is well-worth bearing in mind that absolute rather than relative progress will be needed to put a sustainable floor under the shares since a 40% fall from late 2013 highs.

Investors seem to be well aware of this because after a pop of almost 5% at the market’s open, the shares slipped back to a more moderate gain of about 0.6%.

Sainsbury’s said sales at stores open over a year fell 1.7%, excluding fuel, in the 14 weeks to 3rd January, its third quarter.

Analysts were expecting a fall of between 2.5% and 4.4%, according to the average of forecasts by institutional analysts compiled by Thomson Reuters.

An additional plus is that the supermarket’s sales performance looks better than the 2.8% same-store sales slide it reported in the second quarter.

Gross third quarter sales (including established and new stores, but still leaving out fuel) fell 0.4%.

Investors might like to note that the supermarket is certainly not tardy of maintaining a sense of reality despite today’s not-too-bad showing in the winter holiday period.

Sainsbury’s essentially said the outlook for the remainder of its 2014-15 year (ending in March) will still be challenging, as ‘food price deflation’ (in large part driven by aggressive price cutting from relatively new discount grocers) is showing no signs of abating.

“Given the uncertainty in the trading environment, food price deflation and the price reductions we announced this week, we currently expect our fourth quarter like-for-like to be similar to that of our first half,” the supermarket said in a statement this morning.

Sainsbury’s announced a fight back strategy in November which basically involves cutting corporate costs, cutting dividends and slowing down its rate of store openings, which would help partly fund £150m of new ‘investment’ in lower product prices.

Similar trends are being seen at Sainsbury’s three big supermarket rivals, though there could be some merit in the notion that whilst Sainsbury’s has at least kicked off its price programme (arguably ahead of Tesco and Morrisons) Asda’s price cutting drive, might be more aggressive, with £300m of cost cuts pledged for the first quarter of 2015.

All in all, today’s trading update may qualify as a ‘swallow’ (just) but there’s certainly no sign of spring yet, for Sainsbury’s, or any of the other ‘Big Four’ supermarket chains.

Therefore, whilst a pop in the share price of the like seen earlier is not to be sniffed at, it’s difficult to think the shares have stabilized yet.

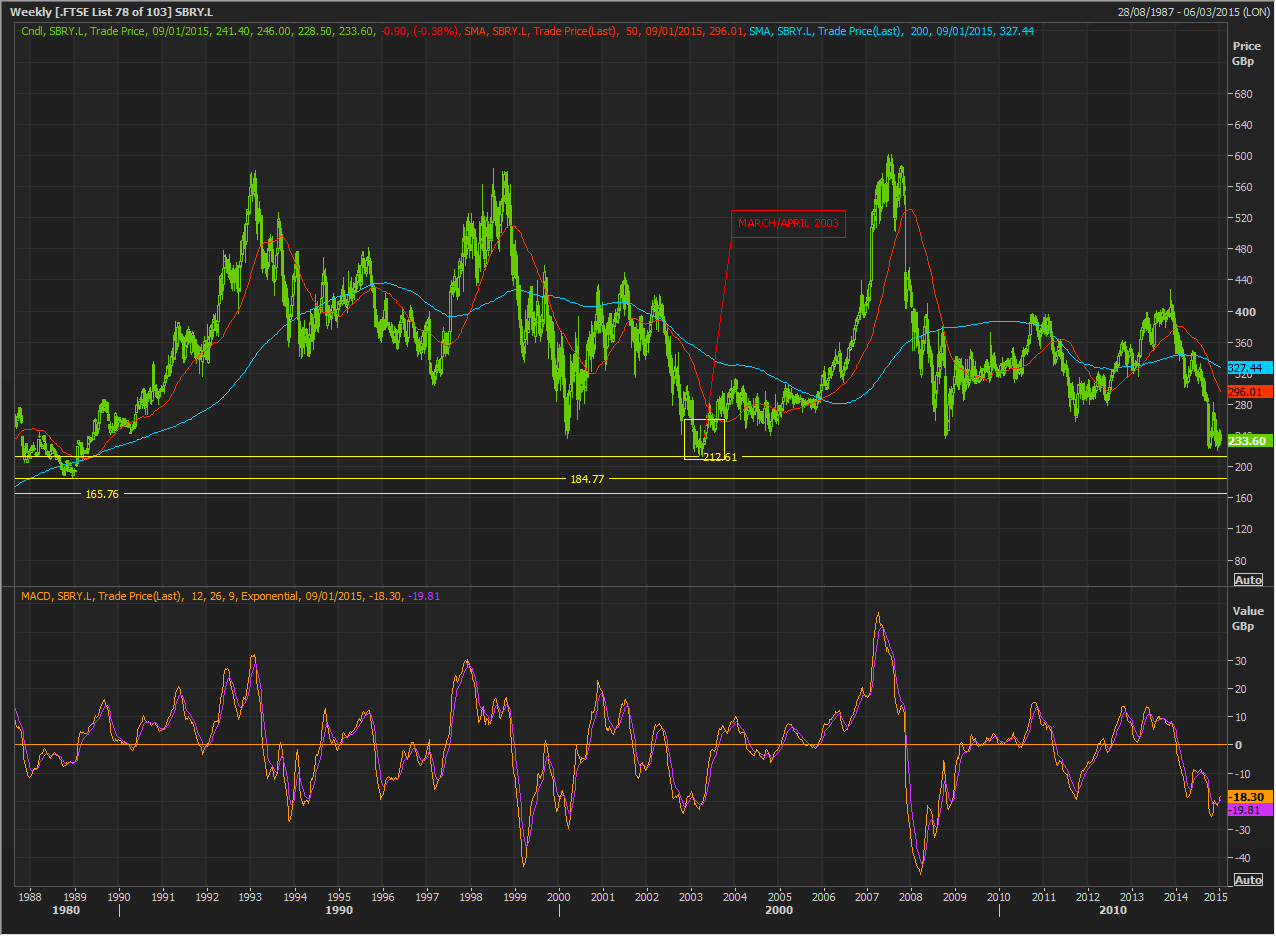

On a conservative view, there appears to be fair reason to expect the ‘magnetism’ of the pivot lows seen in spring 2003 to continue to attract sellers.

This suggests a visit by the shares to prices close to 212p remains a fair possibility.

Obvious near-term catalysts will be an update from arch rival Tesco, due tomorrow and similar statement from Morrisons on Tuesday next week.

Any suggestion from these statements that Sainsbury’s rivals have fared better during their Christmas holiday selling periods will very likely be taken by the market as a signal of slippage on Sainsbury’s part.

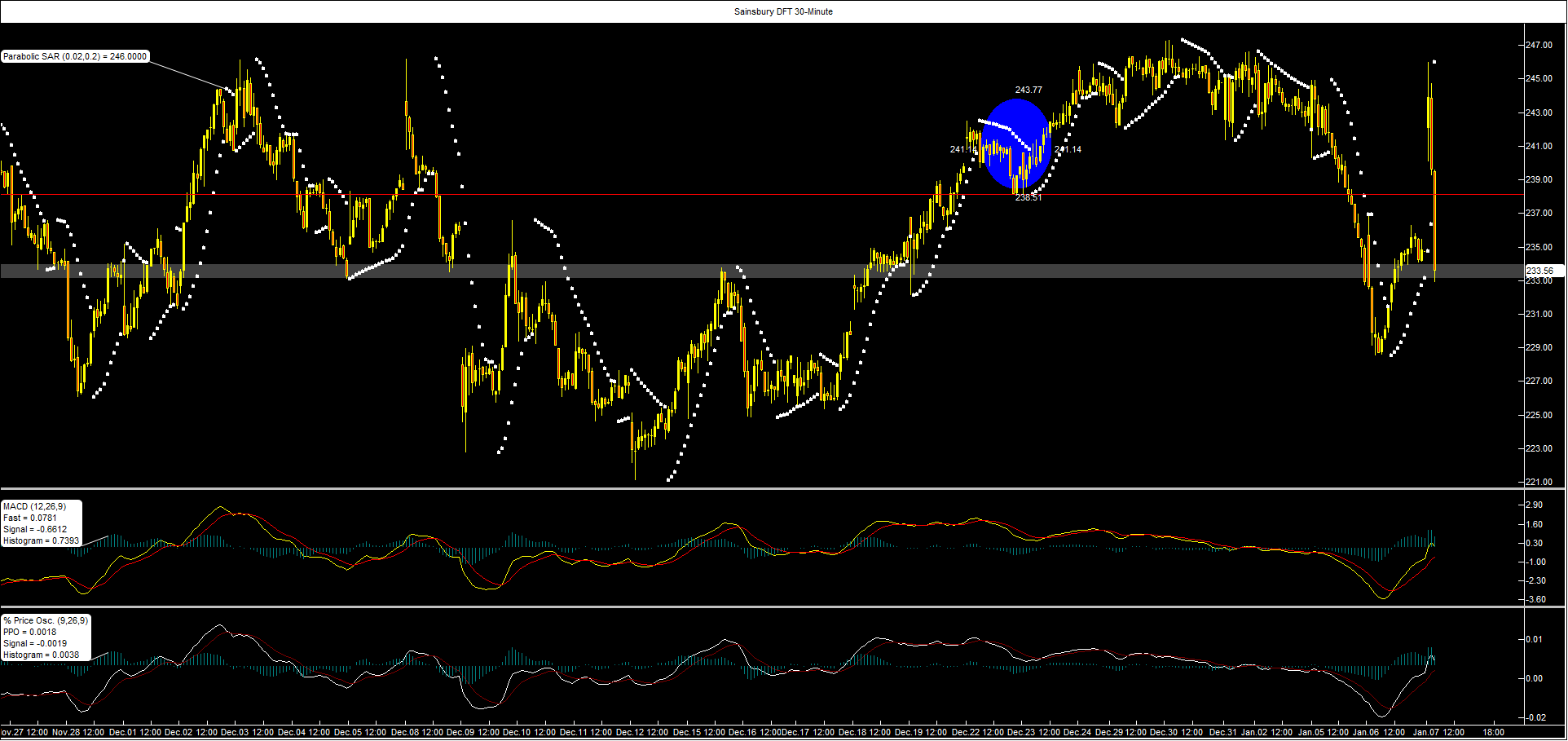

Half-hourly trading of City Index’s Sainsbury Daily Funded Trade shows some eagerness amongst clients to sell this morning’s rally into recent support.

However, such efforts may not go as smoothly as sellers wish in the near-term given that the various oscillators I have included using City Index’s Advantage Trader application suggest momentum moderately favours buying.