Sainsbury dividend cut seems inevitable

Supermarket hasn’t escaped bad times for the ‘Big 3′ grocers Sainsbury’s shares have been perky today and on the face of it, that’s a little surprising. […]

Supermarket hasn’t escaped bad times for the ‘Big 3′ grocers Sainsbury’s shares have been perky today and on the face of it, that’s a little surprising. […]

Sainsbury’s shares have been perky today and on the face of it, that’s a little surprising.

It will release its much-awaited second-quarter trading update tomorrow (Wednesday 1st October) and given the dark clouds hanging over the big, UK-listed grocers , it would have been less surprising if the shares had fallen.

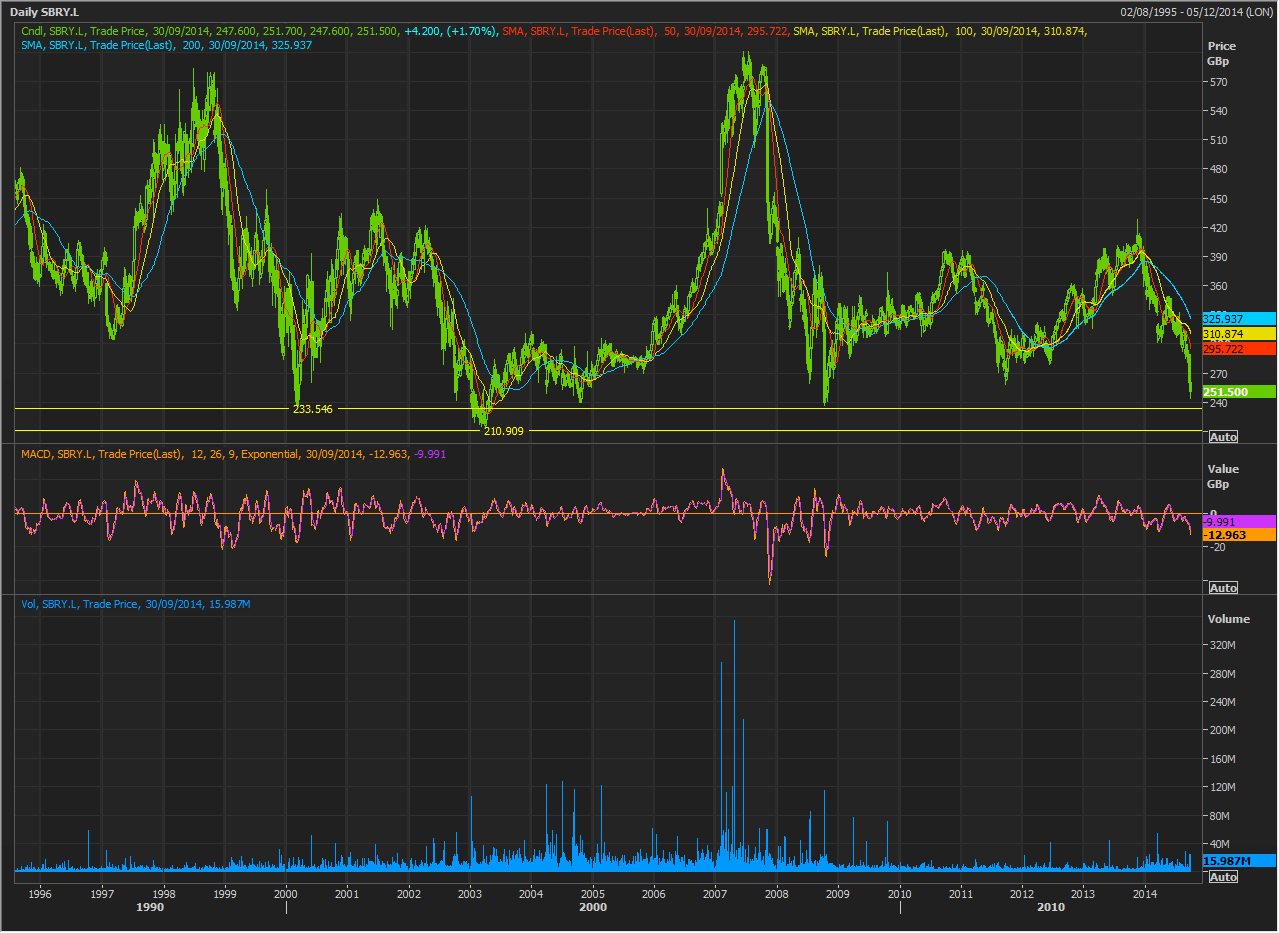

On closer inspection though, Sainsbury’s 1.7% share price rise today is little more than the natural pause any stock will show in the midst of a confirmed downtrend.

Sainsbury’s stock has gone from a peak of 428p reached in November last year, to nudging lows last plumbed in June 2008, below 250p.

That represents a share price fall of more than 41% in less than a year and is much more in keeping with investors’ pessimistic expectations for tomorrow’s results.

It’s clear tomorrow’s results are likely to show the third-largest supermarket chain in the UK (by consumer spending) has had as gruelling a year as widely expected, judging by the calamitous trend of its closest peer Tesco.

The havoc wreaked on Britain’s ‘Big 3’ grocers (or ‘Big 4’ if we include American-owned, but UK-based Asda) by upstart discounters like Aldi and Lidl is already infamous.

Suffice to say grocery market share grab by low-cost supermarkets shows no sign of slowing.

Data released a few days ago showed Aldi increased sales by 29.1% year-on-year and Lidl leaped by 17.7% in market share figures for the 12 weeks to 14 September.

Retail data provider Kantar Worldpanel also showed Waitrose sales rose 4.5% and placed Asda as the only major UK grocer increasing share, with a rise of 0.8% to 17.4% market share.

Tesco is well known to be reeling from a host of problems.

These were crowned by its sales falling 4.5%, leaving it with a market share of 28.8%.

Morrison’s sales fell by 1.3%.

That brings us back to Sainsbury.

Its sales fell by 1.8%, leaving its market share down at 16.2%.

In keeping with that, we’ve noticed stock market consensus forecasts of Sainsbury’s closely-watched same-store sales performance have been steadily falling for months.

(Same-store sales remove contributions from stores open less than a year. Most major UK supermarkets also exclude petrol sales from the figure.)

Whilst in June, the supermarket’s CFO, John Rogers, strongly suggested same-store sales would match their fall of 1.1% in the first quarter, our view is that the continued deterioration in grocery sales will mean Sainsbury’s store sales are bound to be worse than that in the second quarter.

We expect Sainsbury to report a 3.5%-to-5% fall in like-for-like sales tomorrow.

We see total sales flat quarter-on-quarter at 1%.

The other big watch point is of course the dividend.

With no respite in sight for the ‘Big 3’ we think something’s got to give at each of them.

More profit warnings are not out of the question.

Even a ‘cash call’, (AKA rights issue) under certain conditions, specifically for Tesco, might be possible.

(A rights issue will usually weaken a company’s share price.)

For Sainsbury, a rights issue seems unlikely.

But, Sainsbury’s management have given themselves lots of leeway to slash the pay-out for the sake of ‘investment in margin’ (to use the grim catch phrase many UK supermarkets have adopted lately as a euphemism for price cuts.)

Sainsbury has pledged to try to keep ordinary dividend cover at least 1.5 times its underlying earnings per share.

Its dividend for the last fiscal year was 17.3p with coverage of 1.9 times EPS.

But we already know consumer spending at Sainsbury in the most recent 12-week period fell by almost 2%.

To keep things simple (and to assume a best-case scenario) let’s say these falling sales equate to a fall of about 2% for the whole fiscal year.

Bearing in mind EPS was 33p last fiscal year, with an operating margin of 3.65%, even with coverage of 1.9 times (same as last year) the annual dividend would automatically fall 28 basis points this year to 17.02p.

In all probability, any quarterly pay-out would be cut too.

But such a dividend fall is still based on ‘lenient forecasts’ and the pay-out would remain within Sainsbury’s ‘at least 1.5 times’ coverage policy.

With Sainsbury stock now yielding about 6%, a dividend cut tomorrow versus market expectations suggests something closer to 50%.

The market is very likely to react to any dividend downgrade in way that makes today’s 4.2p share price gain look even more like the small change it is.

Note the shares are currently balanced on a support line that has stood the share price in good stead for more than a decade.

Below that is second-line defence close to 210p.