SABMiller shares creep lower ahead of deadline

Updated 21st October 2015 – 0933 BST SABMiller succumbed to Anheuser-Busch InBev last week after a whirlwind courtship, but tying the knot will take much […]

Updated 21st October 2015 – 0933 BST SABMiller succumbed to Anheuser-Busch InBev last week after a whirlwind courtship, but tying the knot will take much […]

Updated 21st October 2015 – 0933 BST

SABMiller succumbed to Anheuser-Busch InBev last week after a whirlwind courtship, but tying the knot will take much longer.

Try leafing through the pile of antitrust approvals required.

Regulators are wary of the lake-like beer volumes the combined company could control.

In the States, 70% of market share would fall at ‘Megabrew’s feet without a forced disposal of SAB’s interest in the Molson Coors JV with Miller.

ABI knows from experience that US competition officials will probably demand that pound of flesh.

They forced the brewer to drastically curb its $20bn Grupo Modelo acquisition about two years ago.

Late last week Australia’s takeover watchdog showed its teeth.

The Competition and Consumer Commission didn’t comment directly, but a former commissioner did.

“This deal will not have an easy ride through the ACCC” he told reporters.

Aussie antitrust has latterly frowned on deals that would remove the last but two dominant market players.

The ABI-SAB combo could control 46% of Australasian beer.

And, if regulators in saturated markets say ‘nope’, risks rise that overseers of SAB’s 21% share in China will as well.

The worst-case scenario is that the deal is stifled globally, but the second-worst is almost as undesirable.

In the US alone, MegaBrew could forego $1.9bn annual Ebitda, based on multiples likely buyer Miller would pay for 58% in Miller Coors.

In Australia, SAB made 12% of its total revenues, or £2.7bn, in 2015 financial year.

Anheuser typically embeds Aussie sales in its Asia Pacific figure.

LatAm was latterly 11% of ABI’s total sales or about $5bn.

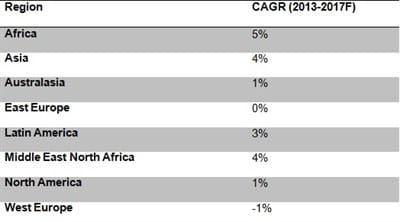

ABI is banking on the fast-growing African market, which SAB dominates, to buttress the takeover rationale regardless of disposals elsewhere.

Source: canadean.com

Will shareholders be as patient?

Anheuser’s financial room to manoeuvre in the deal is already looking limited.

We hear it is busy arranging up to $60bn in new loans to help cover the 50% cash premium to SAB’s mid-September worth (c. $68bn).

Moody’s already placed the firm on review for a downgrade.

We believe shareholders should also note that dwindling first-world beer volumes have pressured free cash flow rates at both SAB and ABI.

Our analysis suggests their free cash flow yields—derived from cash balances after ‘ordinary’ spending and costs—are close to five-year lows.

Please click image to enlarge

Free cash flow yields tell us how well companies are growing cash in the bank as a factor of market or enterprise value.

To be sure, ABI and SAB are certainly in excellent financial health.

Anheuser-Busch’s EV-based cash flow yield is forecast around the same as other global brewers’, on a one-year view.

However that represents slippage after best-in-class cash generation a couple of years ago.

Put another way, ABI is expected to generate cash worth 5.2% of its market cap in the next twelve months, compared to 8.6% in August 2013.

Even though ABI’s market cap has risen more than one 30% since then, that still equates to a cash yield attributable to equity holders (nominally at least) that’s around 13% lower.

What could have triggered this fall?

It would be rash to link the reversal of robust cash creation with failure to secure Modelo-operated ‘Corona’, which had 7% US market share in 2013.

But it’s tempting.

The start of ABI’s cash-yield downtrend coincides with completion of its Modelo buy—sin Corona.

Recall that the DoJ’s case hinged less on the 7% share, than the potential for ABI to raise prices on all brands, including Corona.

A 3% rise in 2013 across all of Anheuser’s US brands, plus Corona, could have added $1bn profit per annum, at the time.

Proving this beyond speculation is beyond our scope here, unfortunately.

Club Pilsener, Uganda 2010

What we know is that Anheuser-Busch has commenced one of the priciest takeovers of all time.

This comes after its free cash flashed concerns; perhaps related to prolific acquisitiveness of years past.

It’s also undeniable that the DoJ hasn’t forgotten its 2013 view.

And that ABI is well aware it once again faces exiting a strategic US asset.

That puts even more emphasis on synergies and African growth.

The takeover’s merits after all are its long-term grab of African market share, but costs for nearer-term benefits look inflated.

The backstop would be the estimated 29% global share–albeit slow-growth-to-no-growth–left after disposals.

AB InBev may address the above concerns robustly when (or if?) it hits the new formal takeover deadline, on 28th October.

Meanwhile, after SAB’s 45% advance since late August, note the stock’s first real pause since SABMiller’s agreement last week.

Huge implied support from ABI’s bid suggests any retracement will be slight.

But if uncertainty, misgivings and even incredulity take hold—remember SAB shares have still not reached ABI’s £45 offer—a correction is a risk.

The 12th-13th October gap would quickly become a target: 12th Oct. high: 3800p—13th Oct. low: 3920p.

Support backed by 38.2% of the rise from 24th August would also be on watch.

Continued failure could accelerate the shares past the 18.6% one-day surge in mid-September.

A consolidation zone lies around 2900p-3540p.