S amp P futures higher on renewed Greece hopes

Yesterday saw the S&P 500 post its first quarterly drop in nearly three years. As well as the crisis in Greece and the stock market […]

Yesterday saw the S&P 500 post its first quarterly drop in nearly three years. As well as the crisis in Greece and the stock market […]

Yesterday saw the S&P 500 post its first quarterly drop in nearly three years. As well as the crisis in Greece and the stock market turmoil in China, investors are growing worried about the impact of the strong dollar on company earnings and US exports, and as the Federal Reserve looks set to be the first major central bank to hike rates later this year. Although interest rates are likely to rise only gradually to begin with, the tightening of policy will nonetheless make equities look less attractive on a relative basis. This is partly why we’ve seen an increase in the withdrawal of the so-called “smart money” from US equities lately. What’s more, every time the S&P has peaked at a fresh record high in recent times, there hasn’t been a corresponding increase in the buying momentum. The markets therefore do look fatigued and this could be the twilight of the bull trend.

Although, the possibility for a vicious sell-off is looking increasingly likely for US stock markets, we are yet to see a major technical or fundamental sign that would suggest a correction is imminent. In other words, we could still be in a prolonged consolidation period ahead of potentially another lurch higher in stock prices at some point down the line. And there is a good reason why this could happen, namely that the world’s other major central banks such as the BoJ and ECB are still dovish and that there is a potential for an acceleration in global economic growth, which should be good news for stocks across the board.

In terms of today’s session, Wall Street futures point to a higher open ahead of the ADP jobs report. Sentiment has been lifted by a report from the Financial Times this morning which said that the Greek PM Alexis Tsipras will accept all his bailout creditors’ conditions that were on the table this weekend. This has raised hopes that Greece may find a resolution which could see Sunday’s referendum being cancelled.

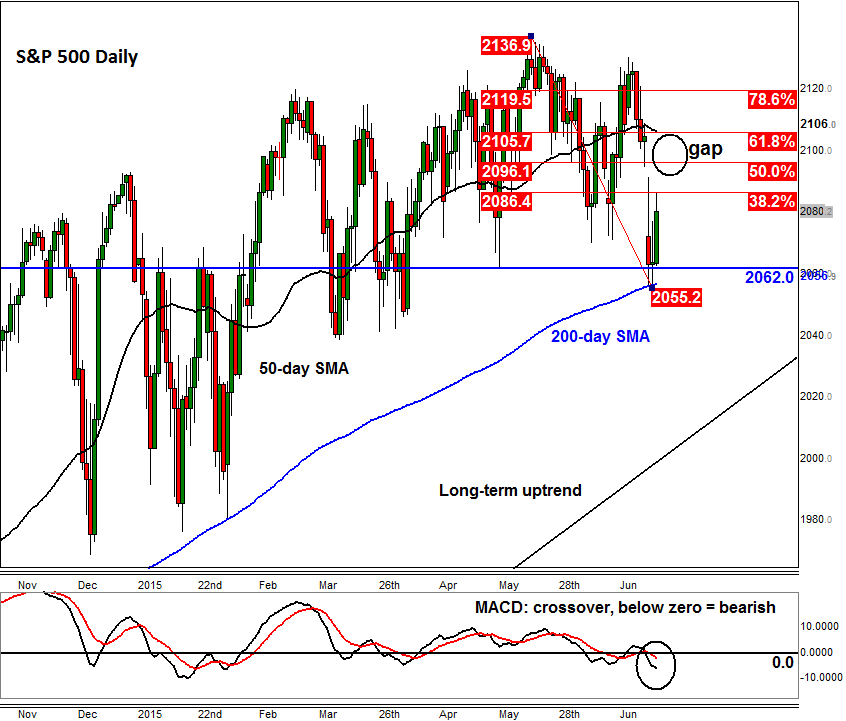

Meanwhile from a technical point of view, the S&P remains inside a long-term consolidation pattern. The recent retreat from near the all-time highs saw the index drop all the way to 2055, creating a huge gap in the process. This gap was partially filled on Monday when the S&P found some strong support from the 200-day moving average. But some of this void remains unfilled and there is the possibility of this happening in the next couple of days due, in part, to the sheer number of high-impact US economic data.

To fill the gap, the S&P will need to take out a couple of resistance levels that are now in sight. In fact, the first such level is being tested at the time of this writing: 2086, a level which corresponds with the 38.2% Fibonacci retracement of the move down from the all-time high of 2137. Above this level is Monday’s high at 2091, which, if broken, could see the index rally all the way through the void and reach the next key area around 2105. As can be seen on the chart, this level corresponds with the 61.8% Fibonacci retracement and the 50-day moving average.

Alternatively, if the 200-day moving average is broken down, then the S&P could be in for a correction. In this scenario, we wouldn’t be surprised if it went all the way down towards the long-term bullish trend around 2010/20, before making its next move.