S amp P 500 Q2 Earnings Season Kicking Up a Notch This Week

Much like this year’s Michigan summer, which got off to a slow start before this week’s projected sweltering temperatures, the Q2 earnings season is about […]

Much like this year’s Michigan summer, which got off to a slow start before this week’s projected sweltering temperatures, the Q2 earnings season is about […]

Much like this year’s Michigan summer, which got off to a slow start before this week’s projected sweltering temperatures, the Q2 earnings season is about to kick into full swing as well.

Only about 12% of the companies in the S&P 500 have reported earnings thus far, but the early results are promising, with 72% of those companies beating earnings expectations and 56% beating revenue expectations. The solid early performance thus far marks a stark contrast from the low expectations, where analysts were expecting aggregate earnings to decline by 4.5% on the back of the strong US dollar. That said, the earnings mavens at FactSet still expect overall S&P 500 earnings to decline by 3.7% when all is said and done, which would mark the largest decline in earnings since Q3 2009 (-15.5%) and the first decline since Q3 2012 (-1.0%). Given the still-depressed expectations, this week’s reports will be critical: roughly 130 companies (26%) in the S&P 500 will report earnings this week, including the largest company in the world by market cap, Apple.

As has been the case with the last few earnings seasons, the biggest theme in the US is the strength in the US dollar. Relative to Q2 last year, the greenback is roughly 20% stronger across the board; this means that foreign sales at many of the large, multinational firms that make up the index are worth “less” when translated back into US dollars. In fact, a number of top-tier companies including YUM! Brands, Johnson and Johnson, and PepsiCo have all cited the dollar as a major headwind. Of course, the precipitous drop in oil prices (down about 40% from last year) is helping some large manufacturing, consumer discretionary, and transportation companies (prominently including airlines) offset the negative impact of the rising dollar.

Beyond the obvious comparisons of earnings and revenues to expectations, traders will also focus on forward guidance this week. So far, the vast majority of companies that have provided guidance for next quarter have revised down their expectations, and forward-looking traders will be keeping a close eye on this metric as we move through this week.

Notable Earnings Reports to Watch This Week:

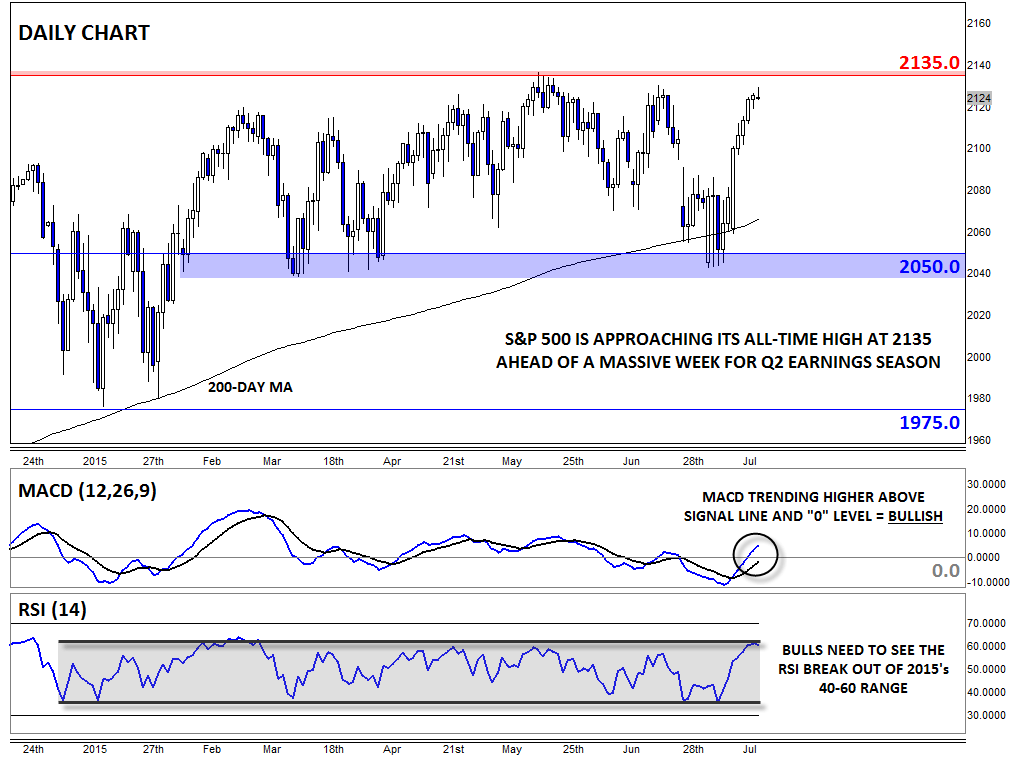

Technical View: S&P 500

From a technical perspective, last week’s furious rally off support at the 200-day MA has left the S&P 500 back within striking distance of its all-time high near 2135. Not surprisingly, the daily MACD has also turned higher, showing a return of bullish momentum, but the more important indicator to watch this week will be the RSI. Throughout the year to date, the RSI has been trapped in a 40-60 range, and in order to confirm a legitimate breakout in the S&P 500 itself (in contrast to the incremental, temporary new highs we’ve seen so far in 2015), traders would like to see the indicator break out of that range and ideally reach “overbought” territory at 70. Perhaps this week’s earnings reports will be the bullish catalyst that frustrated bulls have been waiting for all year.

Source: City Index

Source: City Index