S amp P 500 Global stocks sell off again

The harder the drop, the higher the bounce. That’s exactly what happened at the end of last week and start of this in the global […]

The harder the drop, the higher the bounce. That’s exactly what happened at the end of last week and start of this in the global […]

The harder the drop, the higher the bounce. That’s exactly what happened at the end of last week and start of this in the global equity markets. But Monday’s kick-back rally has quickly ran out of steam and the markets were selling off sharply once again at the time of this writing. No one seems to be able to point the finger at one particular factor behind the equity market sell-off. I think it is a combination of things, including withdrawal of bids after the US indices tried for several weeks to break to new all-time highs when there just wasn’t enough fuel left in the tank. Obviously fears over a premature US interest rate rise could be a reason for the panic, similar to last year. Then, the market went into a free fall which lasted until the second half of January. But the US markets were able to regain their poise as expectations about another rate increase receded amid weakening data and before long they achieved new all-time highs. You could add the ECB in the mix, too, after it decided against easing its policy further last week and according to Mario Draghi, policymakers at the central bank did not even discuss the prospects of extending the bond purchasing programme beyond March 2017. In addition, there are fears that the Bank of Japan may be considering a so-called reverse operation twist and engineer a way to steepen the yield curve. Obviously the US election is another factor creating uncertainty.

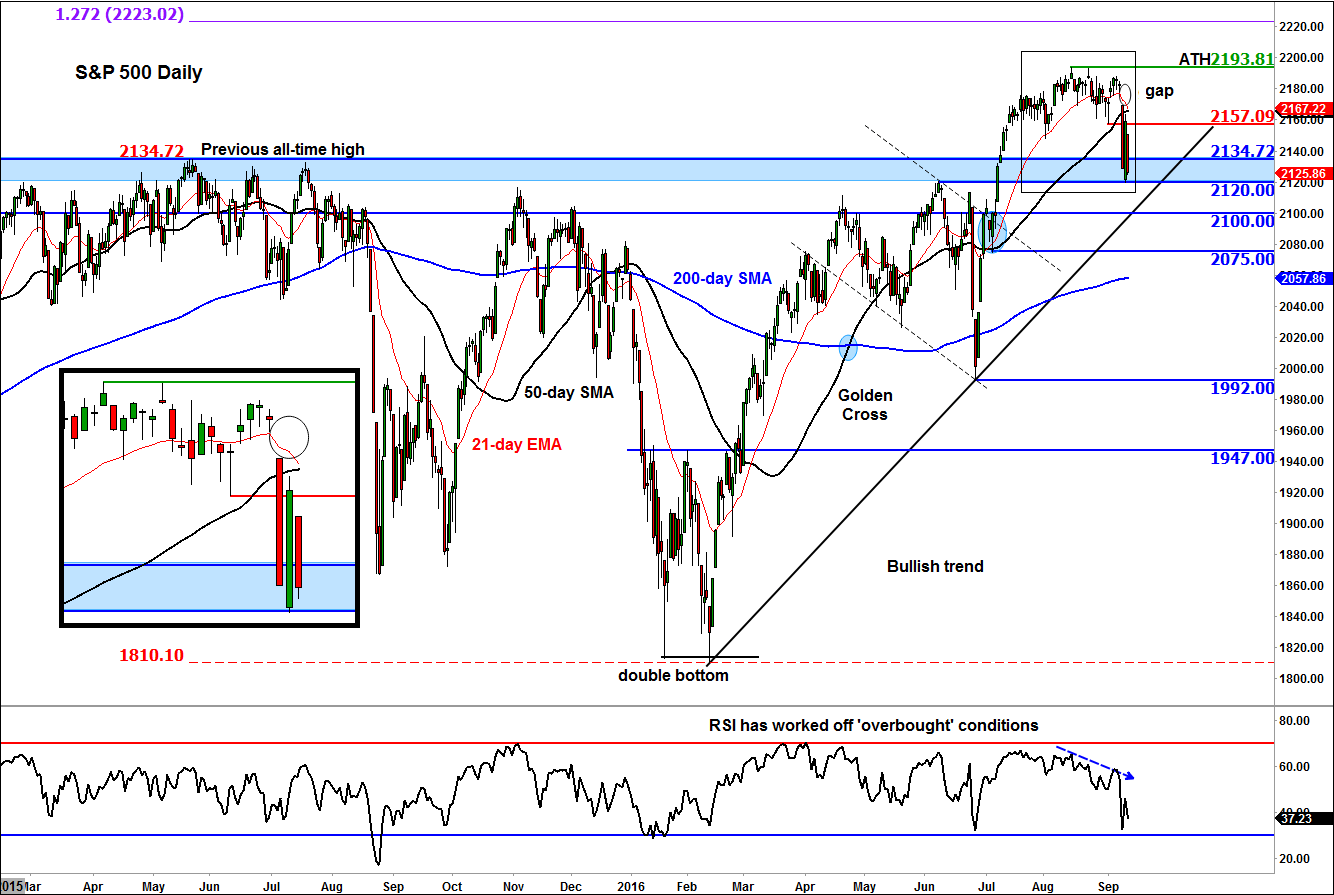

Whatever the cause of the sell-off, clearly there is risk for some further follow-through in the downward pressure in the days and weeks to come. However, I maintain my long-term bullish outlook on the markets as I still believe that there are not many alternatives for yield-seeking investors to choose from, with government bond yields still being near historically low levels. Thus the weakness in equities could be faded once again, especially as the US indices retreat to some significant support levels.

In fact, the S&P 500 is still clinging on to a key support area around 2120-2135, which marks the convergence of the previous all-time high with a prior resistance level. If this level breaks then the next bearish target to watch is at 2100, which corresponds with the rising trend line. So there are plenty of levels which could offer support, leading to a possible bounce. At this stage, we would only turn bearish upon a break below the bullish trend line. If that were to happen then a drop to significantly lower levels would not come as a surprise to us.