S amp P 500 approaching all time high as bulls shrug off mixed earnings season

The sun rises on a new trading week, and traders are seemingly a bit slow to roll out of bed this morning. Most major markets […]

The sun rises on a new trading week, and traders are seemingly a bit slow to roll out of bed this morning. Most major markets […]

The sun rises on a new trading week, and traders are seemingly a bit slow to roll out of bed this morning. Most major markets are merely consolidating in quiet trade, with European equities edging lower, the US dollar ticking down after last week’s surge, and major commodities simply holding their established ranges.

With nothing particularly pressing on the economic calendar today, it’s worth checking in on US earnings season, which is roughly one-third complete. As of this weekend, 173 of the companies on the S&P 500 had reported earnings, and a solid 77% of them have beat analyst expectations. This number sounds incredibly encouraging, but it’s worth noting that the 1-year and 5-year averages for this figure are 74% and 72% respectively, so it’s only slightly better than the recent historical figures.

In what’s become a clear theme over the last few years, far fewer companies are beating estimates on top-line sales. To wit, only 43% of the companies that have reported thus far have beat revenue estimates, well below both the 1-year (53%) and 5-year (57%) averages. This divergence suggests that US companies continue to cut costs aggressively and exploit accounting gimmicks in order to overcome weak overall global growth.

Not surprisingly, the major themes thus far are the strength in the greenback, slow global economic activity, and subdued oil prices. The US dollar index was roughly 17% higher in Q3 compared to last year, and fully two-thirds of the companies that have report thus far highlighted the strong dollar or other currency concerns in their conference calls. Meanwhile, oil prices were roughly 50% lower than the previous year last quarter, hurting energy stocks and helping heavy consumers of gasoline, including airlines, manufacturers, and most consumer-oriented companies. A whopping 167 companies in the S&P 500 report earnings this week, so along with the FOMC and BOJ, US stock market performance will be a major theme to watch.

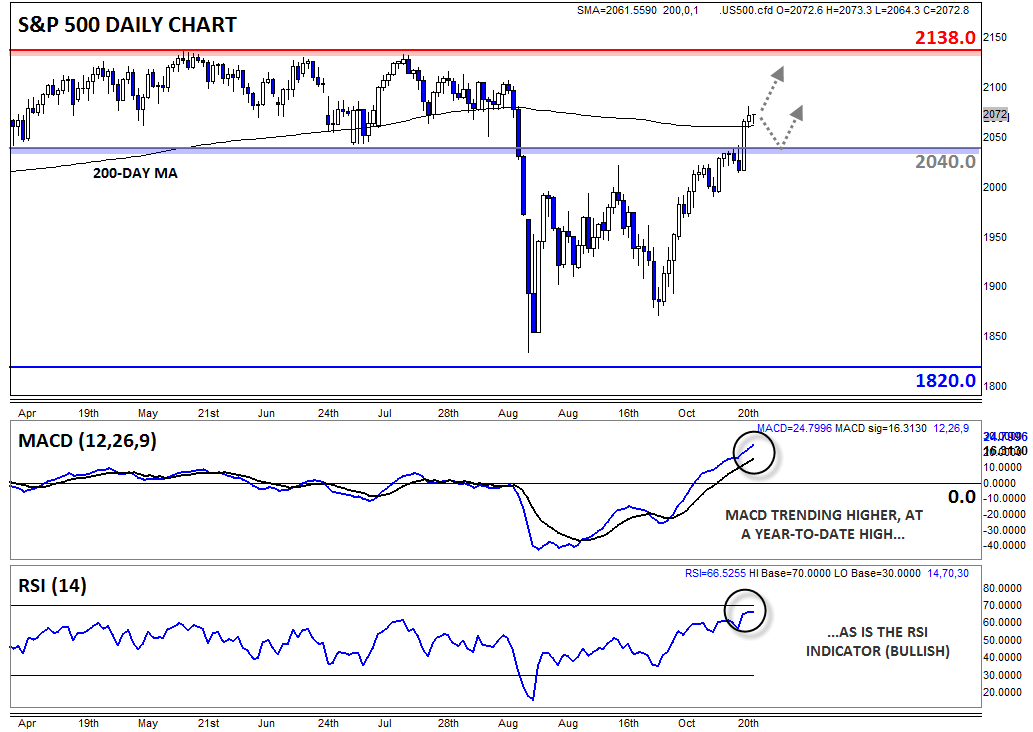

Technical View: S&P 500

Turning our attention to the chart, it’s clear that traders have been encouraged by the so-far mixed earnings season (not to mention the easy monetary policy on both sides of the Atlantic). The S&P 500 has tacked on over 200 points, or over 12%, from its late August low, and stocks are once again within striking distance of the all-time high at 2140. Last week’s surge through previous-support-turned-resistance at 2040 was a particularly promising sign for bulls. Both the MACD and RSI are trending higher at multi-month highs as we go to press, suggesting the near-term uptrend remains healthy.

With prices edging back above the 200-day MA at 2060 on Friday, the S&P 500 could rise further this week, especially if earnings reports improve and the Fed remains dovish. In that case, the index could approach the all-time highs heading into next week. On the other hand, even a shallow pullback this week would not be fatal for bulls, as long as the index remains above the 2040 level.