Investors shrug off flat guidance and small cost fall as add-on sales soar

Ryanair has increasingly had the look of a passenger services company with a stripped-down airline attached. After a stellar net income beat in the second quarter, it’s a slightly less flippant view, with profits coming in 8% above consensus forecasts. The shares surged almost 9% at one point on Monday in the wake of another bumper quarter in ancillary service revenues – also known as ‘add-ons’ – at Europe’s biggest carrier. On a per-passenger basis, they grew 18% compared to a 14% run rate in the first quarter. The impression that Ryanair may be reaching some sort of endpoint after an air fare and seat volume war of attrition that’s lasted almost three years, also boosted the shares.

To be sure, with Brent crude down 4% during the quarter to the end of September, weighing on jet fuel prices, the group also had a tailwind on cost reduction. Still, Ryanair’s jet fuel costs are almost 90% hedged for the current full year ending in March. Given that hedges have been unchanged over the last two months, it looks like the market is discounting risks that prices could fall more. Furthermore, with the next fiscal year north of 60% hedged, RYA may be on the better side of potential OPEC+ moves that could set a floor for prices. Beyond good fortune, unit costs excluding fuel still fell slightly in Q1. That compares with a 4% rise in Q1. The 3% slide on the year in core fares also compared favourably with Ryanair’s guidance for a 6% fall.

Some ambivalence remains on the outlook. The airline narrowed full-year profit after tax guidance to €800m-€900m from €750m-€950m, leaving the mid-point unchanged. A positive takeaway is that management confidence has increased. More so, given Ryanair’s own signal that expected in-service dates for its 737 MAX orders, seen as key to growth at one point, have slipped again. RYA previously anticipated delivery in January-to-February, already later than an initial December date. There remains no objective confirmation from Europe’s EASA regulator of when the planes may fly again. Compensation will offset most of the dent to earnings though even visibility on that is unclear. Either way, the shares signal that investors believe delayed plane deliveries, as well as potential further strike disruption have been adequately priced - for the moment. Including Monday’s advance, RYA is up 60% since late August. Unchanged guidance is beginning to look conservative, pointing to further share price upside into year end.

Chart points

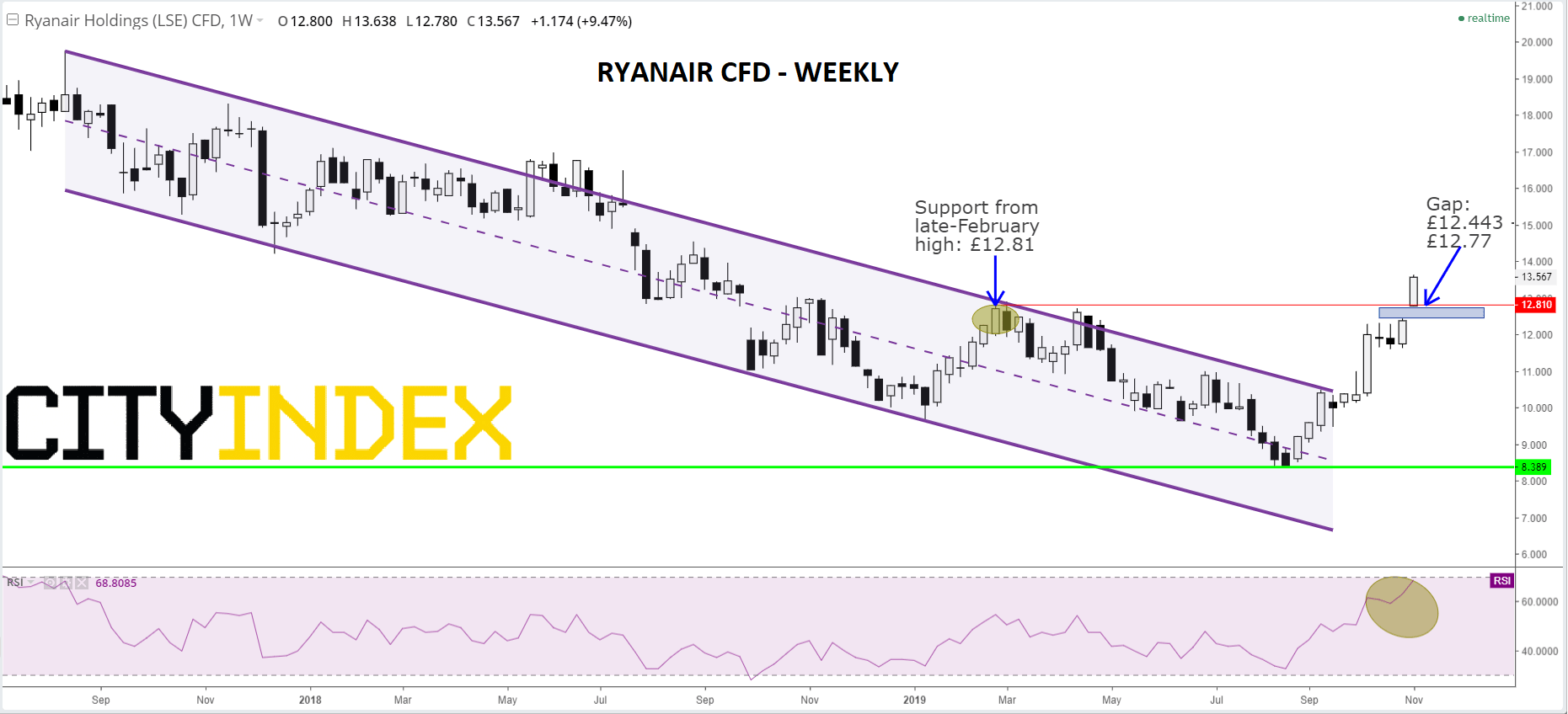

- RYA has successfully passed a critical juncture by establishing itself above £12.81, the former 2019 peak, notched in late-February

- Setting a new 2019 high, with good corroboration from price action and the Relative Strength index, confirms that RYA’s swing higher off August lows represented a trend change. At the very least, there’s now a floor under the down leg that began in August 2017

- The falling channel since then has clearly been broken, reducing the selling bias that overhung the stock whilst the structure was intact

- A price gap has opened between last week’s £12.443 high and Monday’s £12.78 low. It introduces the possibility that shares will revert into the shortfall for a spell, though such a move is not inevitable

- Only a sustained relapse below £12.81 would re-open the risk of renewed marked declines

Ryanair Holdings Plc. CFD (LSE) – Weekly

Source: City Index

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM