Ryanair shares peak after latest forecast raise

Ryanair shares steepened their ascent off mid-October lows with a rise of as much as 10% today, after its second forecast upgrade in a month. […]

Ryanair shares steepened their ascent off mid-October lows with a rise of as much as 10% today, after its second forecast upgrade in a month. […]

Ryanair shares steepened their ascent off mid-October lows with a rise of as much as 10% today, after its second forecast upgrade in a month.

The Dublin-based airline’s London and European listings are continuing a rebound from slumps in the autumn that were to be based on tightening market conditions and signs that competition, namely from arch rival easyJet, was notching up.

However, a number of tailwinds have come to the sector’s aid in recent months, chiefly the plummeting price of fuel, and Ryanair has been the biggest beneficiary among European airlines.

It’s notable that Ryanair stressed it doesn’t expect significant upside in profitability from the oil price fall, as it has hedged against price increases in 90% of the fuel it requires to March 2016.

But its shares have got an uplift from cheaper oil nonetheless.

Ryanair’s recent share price gains may partly be down to easyJet’s recovery story now being perceived by the market as more advanced than Ryanair’s, therefore casting easyJet as having diminished room for further improvement, and probably at a slower pace.

On the other hand, the Ireland-based carrier hit a nadir in terms of poor publicity and earnings in 2013 with a number of profit warnings and negative customer surveys.

This forced it to publicly commit to better customer service, improve the coherence of its sprawling European footprint and strike a better balance on costs and margins—i.e., put a stop to its apparent ‘low-cost-at-all-costs’ strategy, and “unnecessarily pissing people off,” to quote Ryanair’s CEO Michael O’Leary.

These measures included a better-structured forward booking strategy, a website revamp, tripled marketing budget and providing a business class fare category for the first time.

All this helped Ryanair to upgrade its profit forecasts for the second time in a month on Thursday, after reporting that passenger numbers climbed 22% in November.

(This compares with a passenger rise of 3% at easyJet during that month).

Having only last month raised its forecast of profit after tax for the year ending March 2015 by almost 20% to €750m-to-€770m, Ryanair said it now expects to make between €810m and €830m.

This latest improvement of guidance puts the top end of Ryanair guidance almost €100m above market forecasts with consensus looking for a 40% rise in net profits to €732m.

Ryanair also said it managed to raise load factor—a measure of seats sold as a percentage of capacity— to 88% from 81%, despite ramping up the number of seats by 13% in November.

The airline’s success in balancing efficiencies with selective ‘investments in margin’ (this year’s buzz phrase that means price cuts) has enabled it to maintain its operating lead in the air travel sector.

Its operating margin is assessed as 16.4% over the last 12 months compared to a 4% industry average, according to data from Thomson Reuters.

This serves to underline Ryanair’s prevalence in the sector and also the edge that it has largely maintained above its closest peer and fiercest rival easyJet.

EasyJet only managed a 7.7% operating margin over the last 12 months.

Making a definitive case for one being a better investment case than the other is problematic though, aside from the fact that easyJet recently increased the amount of earnings it pays as dividends, whilst Ryanair as yet has no formal policy.

Still, it’s clear the pair has managed to increase the pressure on higher-cost “full-service” airlines like Air France-KLM and Lufthansa, especially with pilots employed by the latter today staging their tenth strike this year.

Whilst the entire European airline sector is on what could be regarded as a ‘growth rating’ after hitting dire straits early in the decade, Ryanair and easyJet’s operating metrics are firmer than the sector.

For instance their load factors in a troubled year for the sector to March 2014 were still 83% and 90.6% respectively, compared to Lufthansa’s last published European load factor of 74.7% (in the year to March 2013.)

Ryanair and easyJet’s prospective price-to-earnings ratios of 14.3 times and 12.6 times may therefore have some justifiable basis (the sector average is 13).

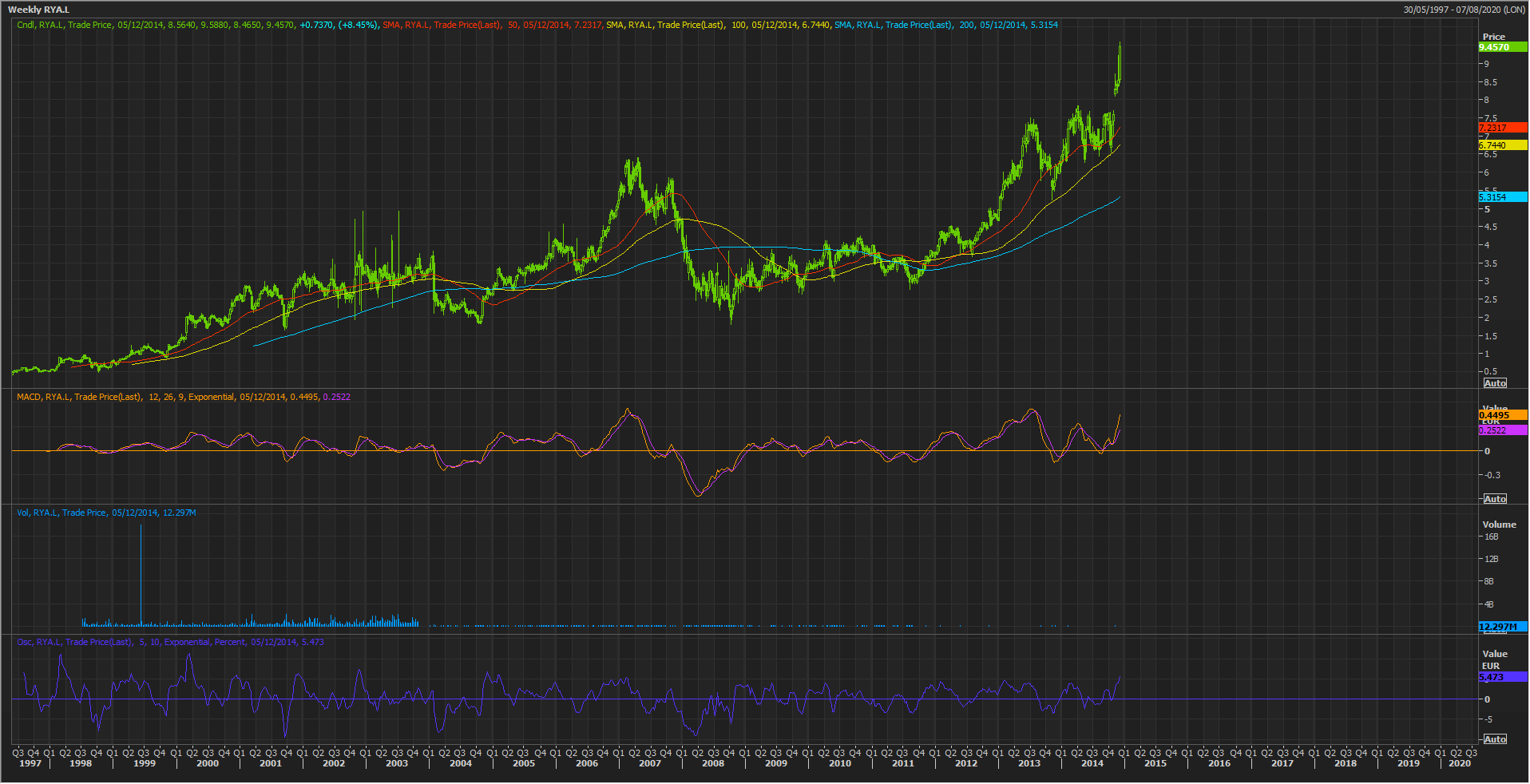

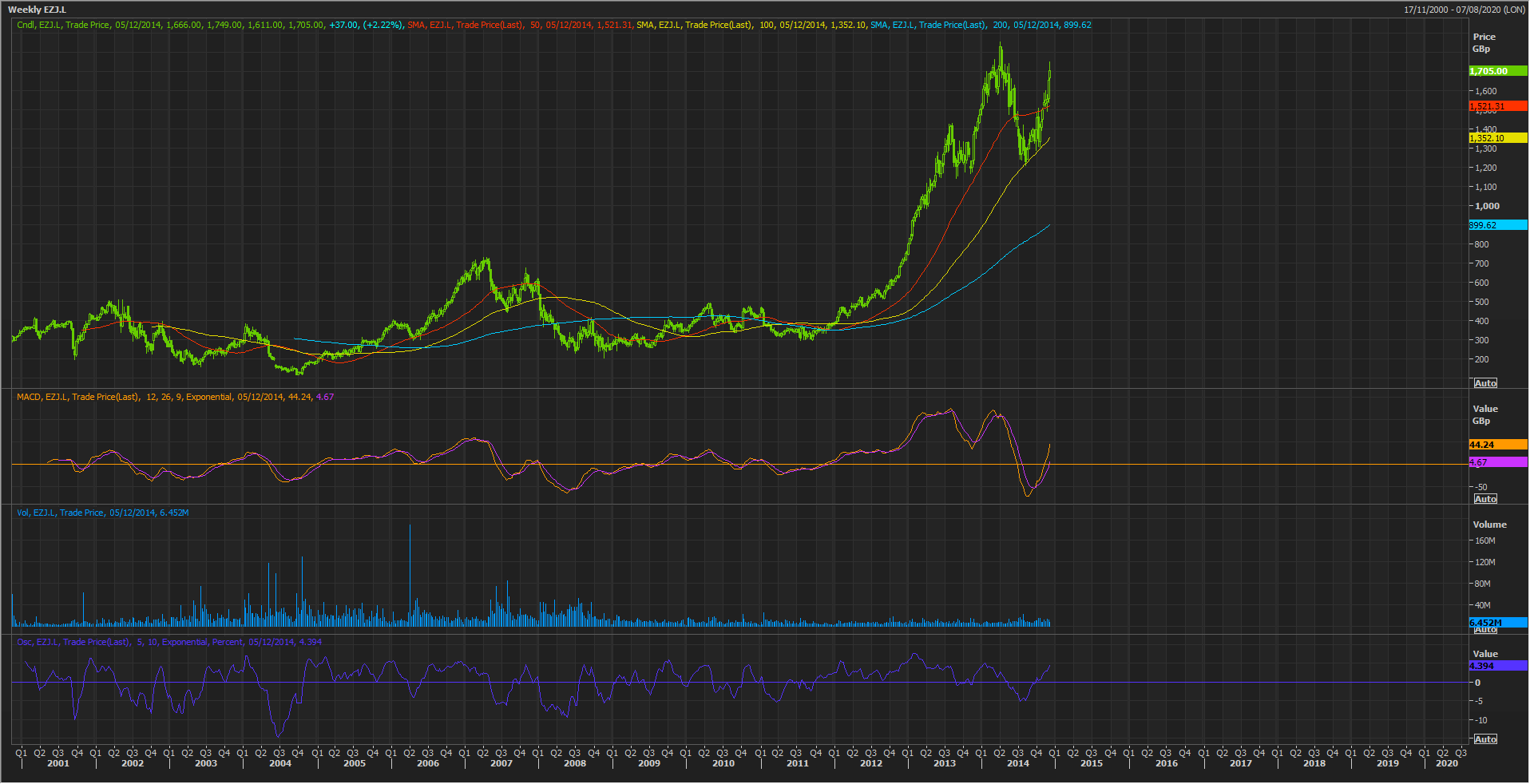

Even so, Ryanair’s upward trajectory into the end of the year has potentially placed its euro-denominated London-listed stock on a moderately more precarious basis than that of its rival, if we zoom right out to the ‘dawn of time’, in terms of the British low-cost airlines.

Ryanair’s weekly stock performance has recently regained all time peaks, whilst easyJet has eased off these.

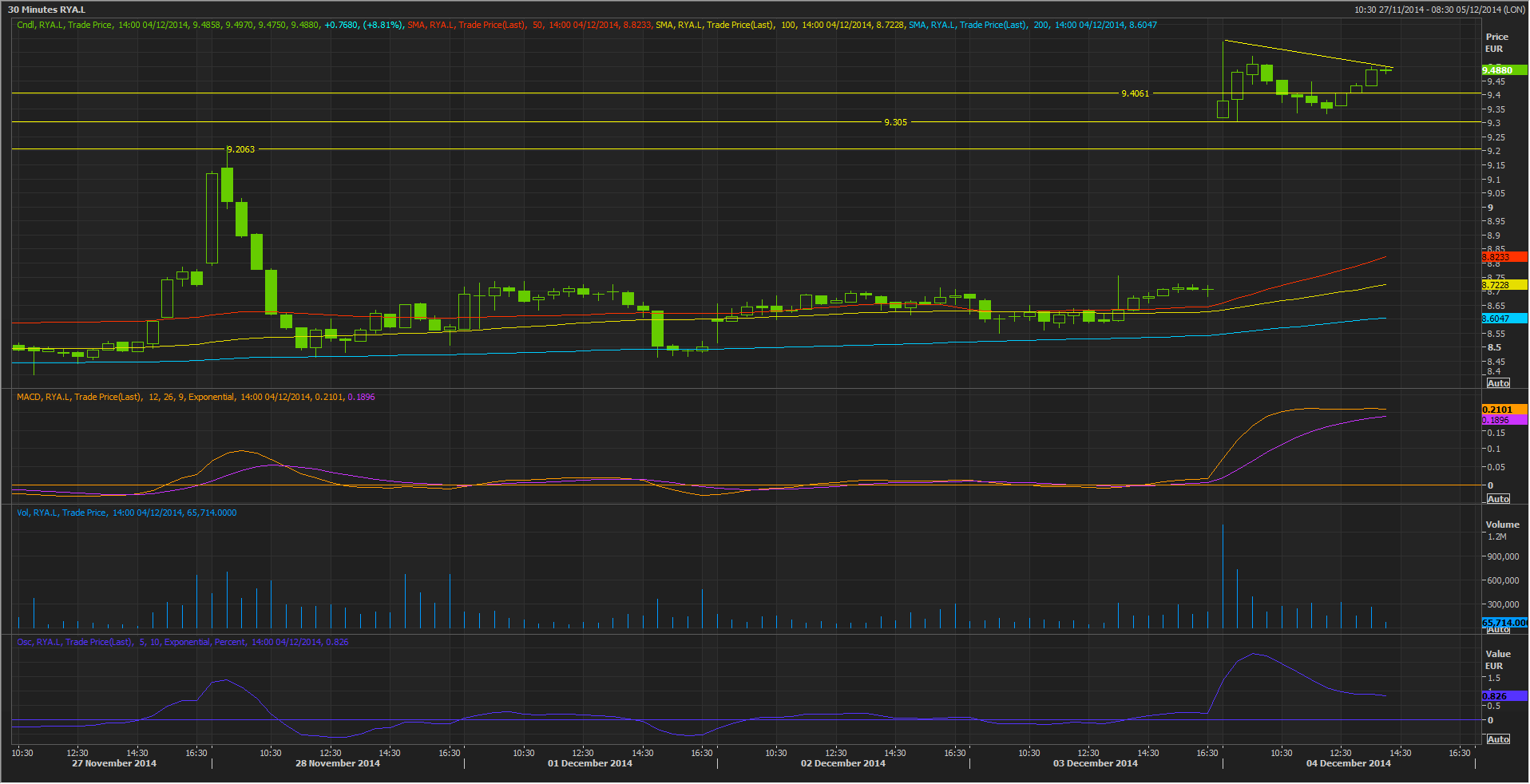

Half hourly trading in today’s sector leader shows marginally softening conviction as the day has progressed, whilst momentum (MACD) is flattening in ‘buy’ territory, and the percentage of buyers reverts back to the balance (see blue percentage oscillator line).

Lots of potential supports nearby.