It’s not a great assessment of Europe’s airline sector when add-ons save the outlook

But with Ryanair’s shares down 43% over two years of low-cost operator hell, investors will take it. The stock lifted as much as 4% in Dublin before slipping 2% into the red. No one’s getting carried away. These numbers are promising, not stellar.

- Q1 profit after tax down 21% on the year to €243m

- Revenues up 11% to €2.3bn

- Average fare down 6%

- Ancillary revenues – from sales of food, extra bag space, faster boarding, etc. – up 14%

- Passenger traffic up 11% to 42 million

- Costs up 19%; including fuel costs up 24%

One of the industry’s key challenges remains a years-long face-off during which fare rises have been aggressively curtailed. There’s little sign Ryanair is ready to blink. It notes the 6% average drop in the first quarter “stimulated 11% traffic growth”. And though it still has the lowest unit costs, it hasn’t been immune to rising overall expenses. Its fuel bill leapt 24%, despite hedging that’s widely thought to be favourable relative to peers.

Delayed delivery of Boeing’s 737 MAX adds another dimension. The embattled plane maker is now unlikely to receive a renewed safety certification by September, as mooted. In turn, Ryanair’s in-service date, initially December at the latest, has slipped to January or February. In fact, there’s little true visibility on Boeing’s chances of meeting those dates either. Compensation should offset most of the dent to earnings, but that too lacks clarity for now. Pilot pay rises and hiring to increase the ratio of staff to passengers will reduce leeway further. Little wonder Ryanair sees expected growth for summer 2020 peak of just 3%.

All told, the group has afforded investors some relief by keeping annual profit guidance between €750m-€950m when the fear was a dip towards the lower end. Yet leg room remains tight and could squeeze further. Chiefly, Lufthansa’s Eurowings appears to be on an increasingly do or die course to retain Air Berlin share, selling excess seats below cost. UK and Ireland pilot ballot results are due next week. Ryanair’s premium valuation reflects its industry-leading cash flow generation and balance sheet, but growth worries are less defined. In other words, there’s room for market forecasts to fall, if not plunge. The shares, down 6% so far this year, could level off, though won’t soar.

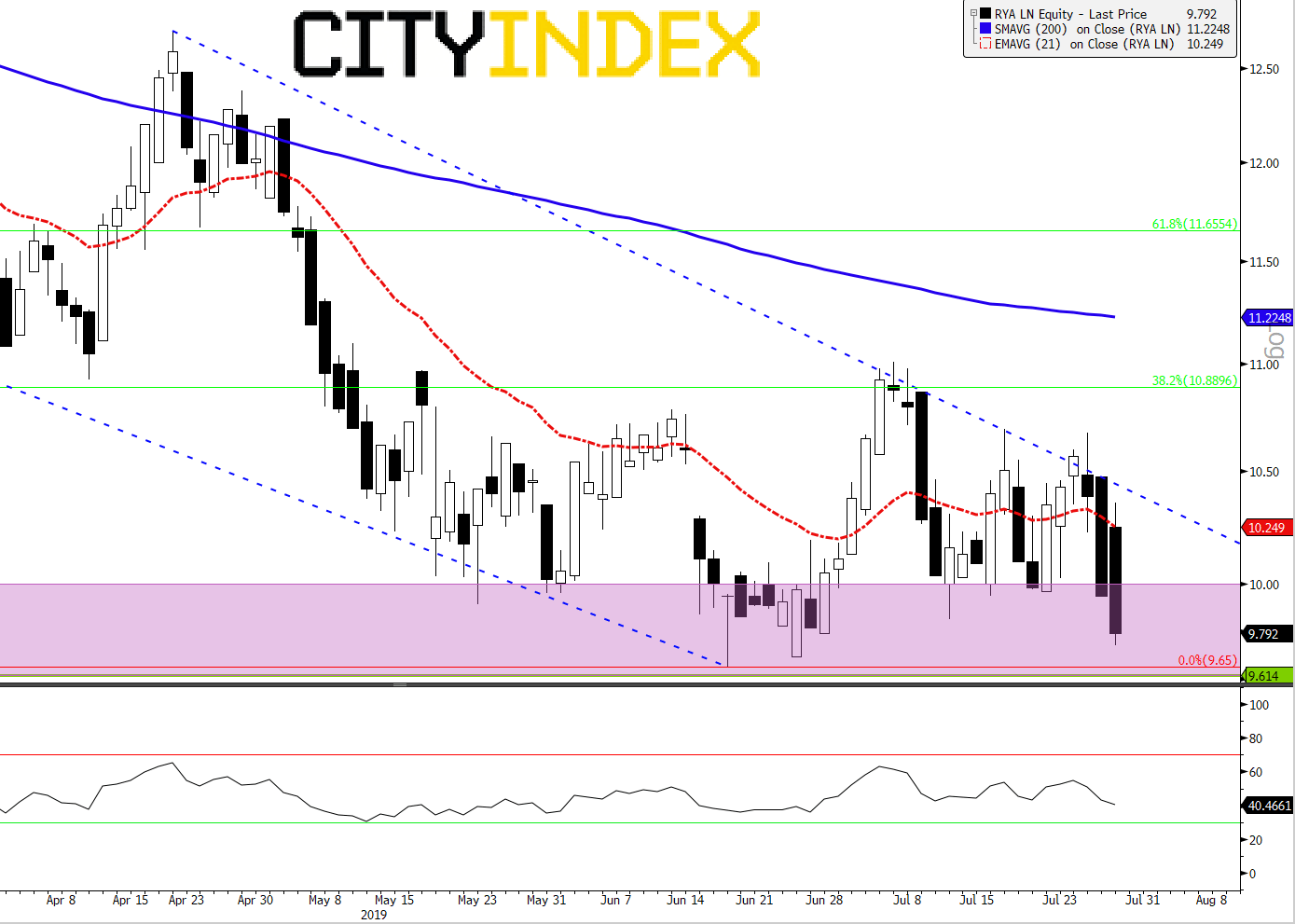

Chart thoughts

A relatively shallow retracement of the resigned reversal to the downside from April’s highs should warn buyers to keep their sights set low. The bounce up from June's four year lows, the second visit in six months, stalled just above €10.88, which equates to 38.2% of the year’s prior advance. The attempt to climb didn’t definitely breach the upper wall of a channel in place since mid-April, indicating the market remains wary even at these subdued prices. What RYA has going for it here is proven support. Assume the backstop is more of a band over which emphatic rejection of prices below €9.61 was observed in December, January and June. With price currently toying with the upper end of the range (call it €10) equilibrium looks near. A potential break out in a few weeks at the apex of the structure should clarify whether bulls of bears are in control. To be sure though, with price tracking below the 21-day exponential average and a sickly-looking RSI, enthusiasm over a possible upside break, isn’t apparent.

Ryanair Holdings Plc. – daily [29/07/2019 14:43:45]

Source: Bloomberg/City Index

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Yesterday 08:18 AM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM