Royal Mail shares may soon return gains

Royal Mail Group’s recent clutch of good news continued on Thursday, as it announced trading in its new financial year had started according to plan, […]

Royal Mail Group’s recent clutch of good news continued on Thursday, as it announced trading in its new financial year had started according to plan, […]

Royal Mail Group’s recent clutch of good news continued on Thursday, as it announced trading in its new financial year had started according to plan, after cost savings enabled it to boost annual profits.

Shares of the former state monopoly that will mark a second anniversary as a privatised business in October were until Wednesday’s close still advancing off fortuitous news flow from the last three weeks, during which time the stock added more than 16%.

RMG said operating profit “before transformation” costs for the year to 29th March rose 6% to £740m, better than the £712m consensus forecast compiled by Thomson Reuters.

Pensions and other exceptional items still pushed the actual net outcome 8.7% lower than the year before though, to £611m.

Group revenue rose 1%.

Progress in Royal Mail’s closely watched parcels business (50% of sales) was also modest, with a 1% rise, as relentless pricing competition and modernisation drives pressured margins.

Parcel volumes rose 3%; letter sales continued what in all probability will be a chronic decline with a 1% fall.

An interesting positive development was RMG’s incursions against its European rivals.

It saw a 7% advance in revenues from the region—welcome news whilst a spate of European-backed start-ups pose a potential threat to Royal Mail’s UK business.

That brings us neatly to what remains the most important news for the group over the last month—that one of the most significant threats to Royal Mail’s UK business to date had been neutralised, at least for now.

On 30th April, Royal Mail stock posted its biggest rise since February, with a near 5% surge after Netherlands-based postal company PostNL announced it ended talks with a private equity backer to expand its Whistl subsidiary in Britain.

LDC, which is the private equity arm of UK-based Lloyds Banking Group, was to have taken a 40% stake in a joint venture encompassing Whistl’s current activities.

PostNL said the company was still considering plans for the unit, including looking for other investors to pursue an expansion.

Less than two weeks later, Whistl announced the suspension of door-to-door letterbox deliveries, ending a service that delivered mail in larger UK cities like Manchester and London, putting the jobs of around 2000 employees at risk of redundancy.

Despite this promising news for RMG, albeit not from its own initiative but apparently from ‘luck’, these events are unlikely to mark the end of PostNL attempts to establish itself in the UK market.

The slippage of as much as 2.6% in Royal Mail stock this morning may suggest that suspicion is beginning to be shared more widely.

My base case that argues against the rise of the stock much further is that RMG still faces potential competition from new strong UK delivery market entrants like Deutsche Post (owner of DHL) and indeed even PostNL, should the Dutch firm manage to sort out how to fund its expansion.

This is the main reason why I think the balance of probabilities currently favours the end of RMG stock’s 30% advance from lows in December.

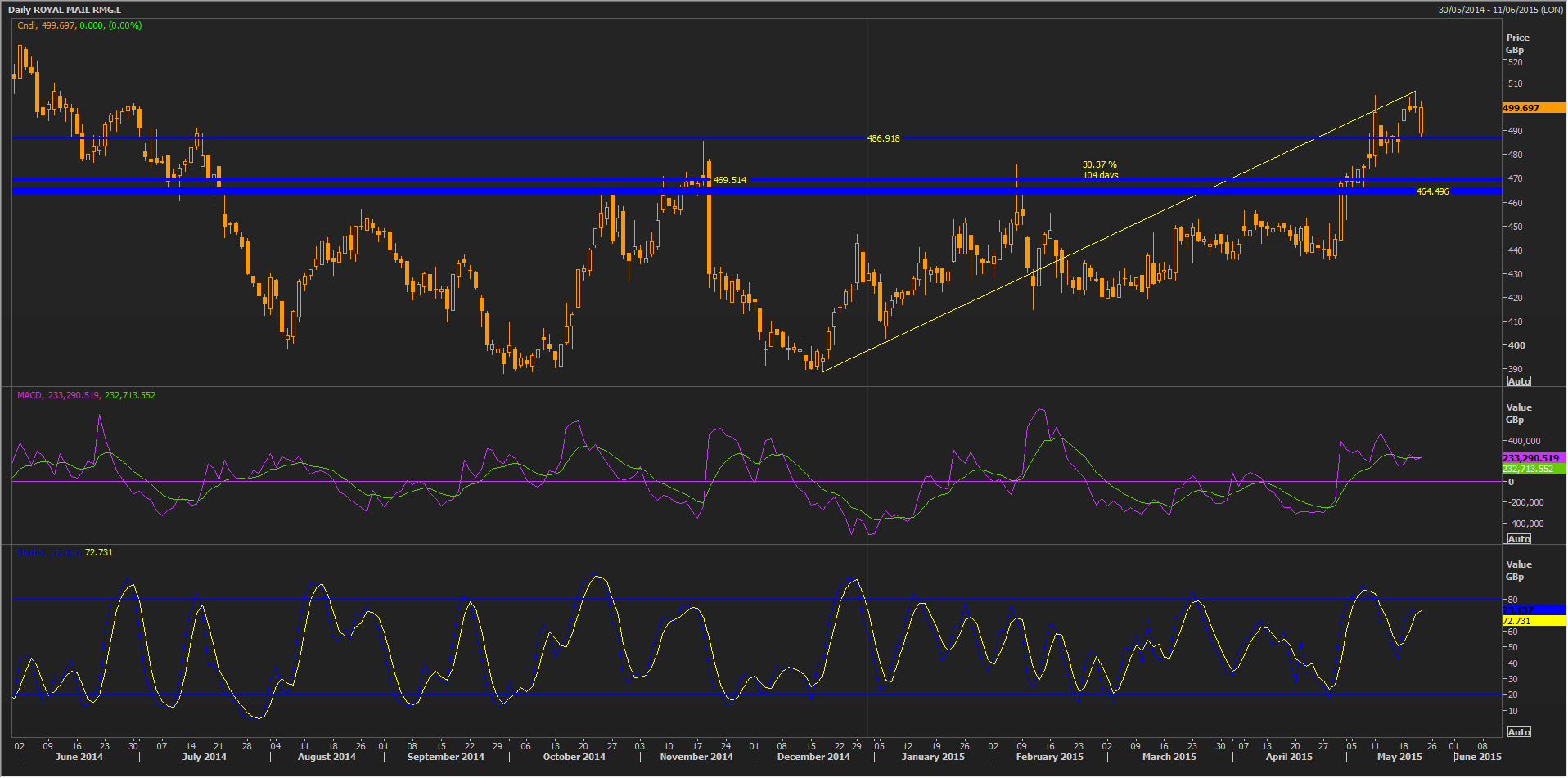

Additionally I note RMG stock is on Thursday testing a support formed from the top of a price spike that followed news the firm would sell property in Nine Elms, near central London.

This leads me to think more solid support lies lower. At the very least the stock should return to support spanning from 470p to 464p.

Fundamental reasons to conclude that Royal Mail’s rally since December might have overshot are below.

It would be unfair to say Royal Mail stock has no attractions, of course.

The stock’s strongest valuation point seems to derive from RMG’s legacy establishment in the United Kingdom enabling a remarkably solid balance sheet and excellent yields.

For one thing, RMG’s surplus property has been estimated in the City to be worth between £450m-£600m, although the firm has not been clear about its intentions regarding these assets.

In free cash flow yield terms, I estimate Royal Mail Group has latterly been close to the top of its European peer group and forecasts suggest it will reach 8% by the end of its current year. That compares with an average of 3.8%, and 5% for Deutsche Post, 6.7% seen for PostNL and slightly negative FCFY expected from TNT Express.

But I conclude the competitive outlook combined with uncertainty, costs and the government ‘overhang’ outweigh these strengths for the medium term at least.