Royal Mail shares climb on second class update

Royal Mail Group’s trading update looks disappointing in almost all respects, apart from a seasonal rise in parcel volumes that’s enabled the former state-owned monopoly […]

Royal Mail Group’s trading update looks disappointing in almost all respects, apart from a seasonal rise in parcel volumes that’s enabled the former state-owned monopoly […]

Royal Mail Group’s trading update looks disappointing in almost all respects, apart from a seasonal rise in parcel volumes that’s enabled the former state-owned monopoly to say it will hit full-year expectations.

Still, that was enough to set the shares on their best rally since November, with the stock rising as much as 5% on Thursday.

This is the market’s reaction to RMG painting a positive tone on its outlook, even if the news is only relatively promising rather than showing outright progress.

Here’s why:

On that more relative basis mentioned earlier, which is currently being well-received by the market, divisional parcel growth has risen back to flat following the 1% fall seen at the half-year stage.

This is expected to enable Royal Mail to report full-year results in line with expectations.

Consensus forecasts currently foresee full-year net income of about £159.44m.

On a more absolute, perhaps shorter-term perspective though, we continue to regard RMG as too hamstrung by legacy constrictions and the over-resourced practices of a formerly public-owned monopoly.

Smaller, nimbler rivals with tighter cost structures and flexible resources will continue to pick off aspects of RMG’s business due to their ability to survive on much thinner margins, in our view.

Are there compelling reasons to expect Royal Mail’s 50%-revenue earner, parcels, to recover back to its recent run-rate growth of 4%-5%?

We doubt it. 1%-2%, or even lower is likelier.

In a statement accompanying Royal Mail’s figures, CEO Moya Greene expressed confidence “that the outcome for the full year will be in line with expectations”.

However she later stressed during an interview with Reuters news agency that pressures were expected to continue.

“The conditions of overcapacity and too many players chasing traffic (are) going to continue to put pressure on prices for the next couple of years,” Greene said.

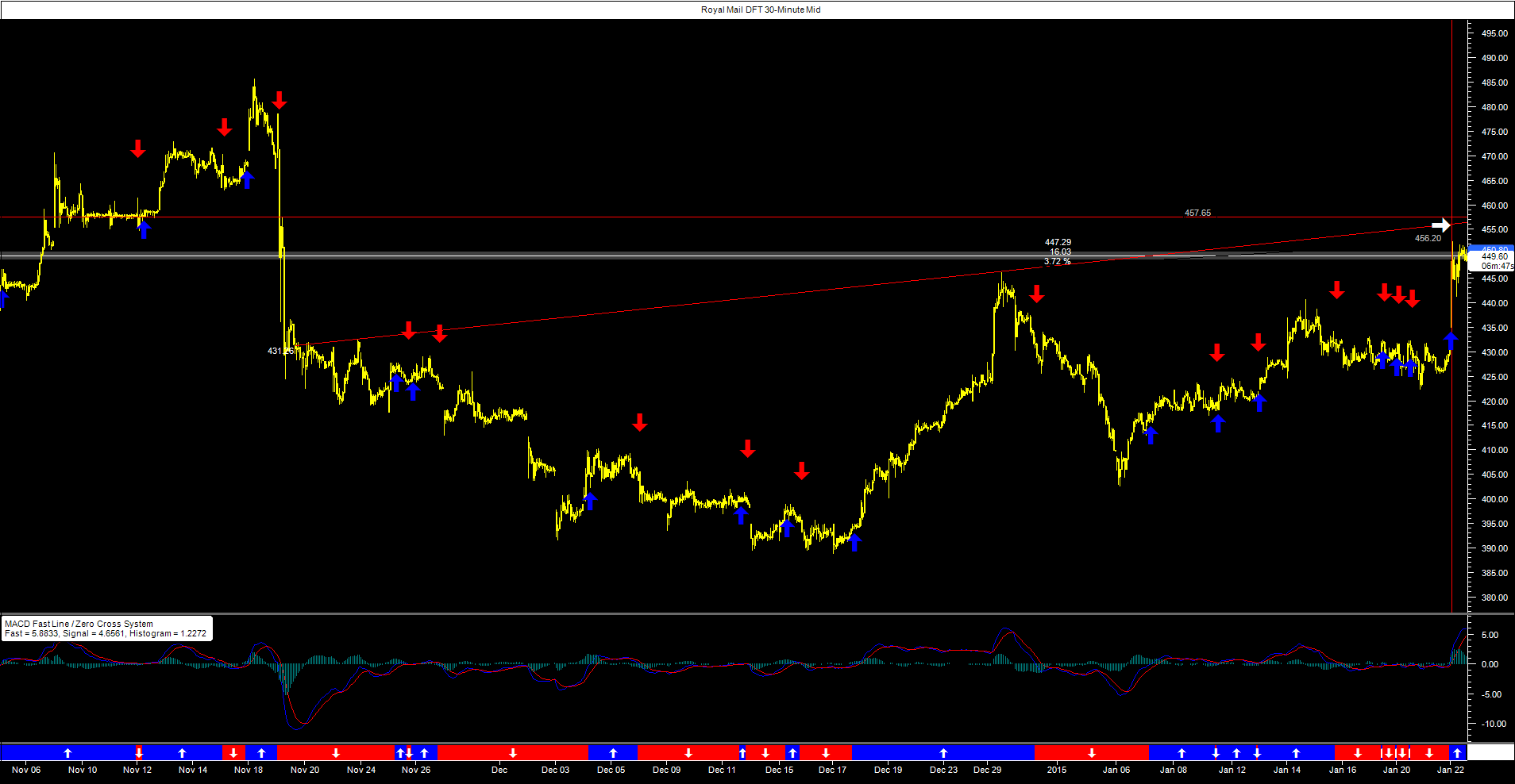

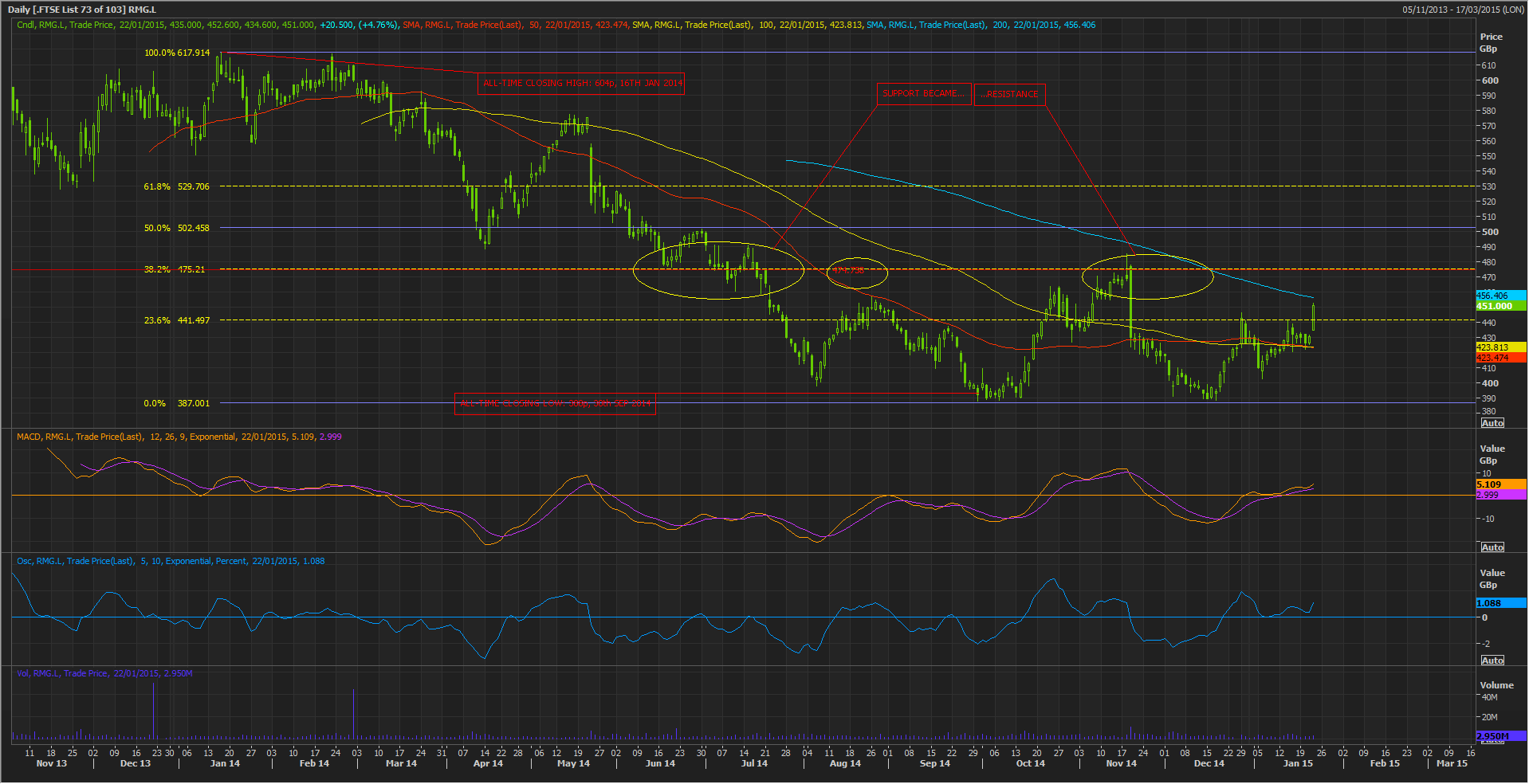

It seems plausible to me these factors will continue to dampen sentiment on the stock, keeping it below important Fibonacci levels, confirmed resistance and even perhaps the 200-day moving average, for the medium term at least.

There’s little doubt the current bullish tilt of the stock is strongly present on shorter-term time frames too.

Traders of City Index’s Daily Funded Trade are bidding up the contract in the same way as the market stock.

Our MACD Zero Cross trading system last signalled a long entry on Wednesday morning, which has in this case been corroborated.

In a similar way to the underlying stock, I do expect the DFT to be challenged on the upside at the points marked. I also note momentum currently looks stretched on the upside.