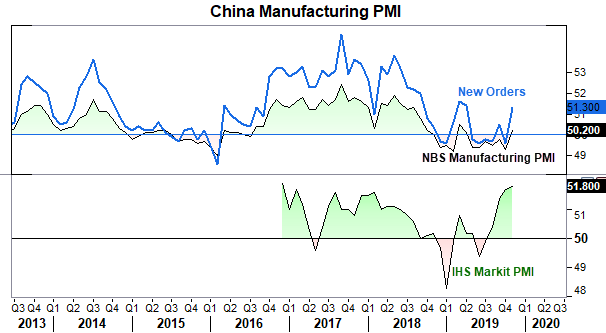

The week began with an element of risk on thanks for positive Chinese data over the weekend. China’s manufacturing PMI expanded in November to break a 7-months stretch of contraction according to China’s National Bureau of Statistics (NBS). At 50.2, it’s the highest read since March and backed up by new orders expanding to 51.3.

Whilst the government back figured are treated with a little caution, it’s encouraging to see that the privately-run PMI data from IHS Markit also expanded at 51.8, beating expectations of 51.4 and above 51.7 prior. With the sector expanding at its fastest pace in early 3-years, it ticks another box for the potential of a global rebound as we head into 2020.

- S&P500 E-mini futures are up +0.28% and just off record highs

- Gold is -0.21% lower

- US10Y has risen to 1.8%, up 1.77% from Friday’s close

- NZD and AUD are the strongest majors, JPY is the weakest

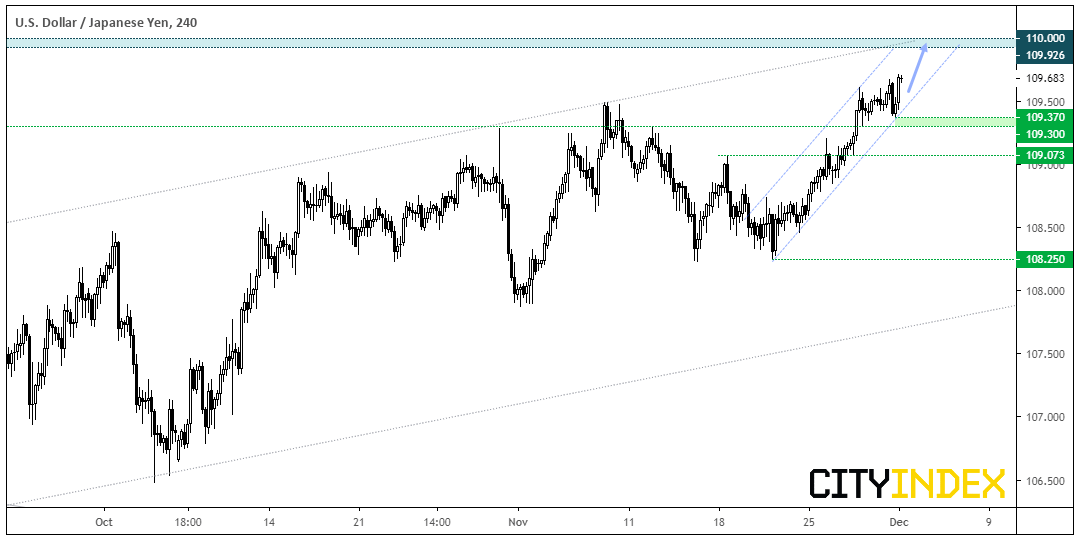

USD/JPY remains within a bullish channel, with last week’s break above 109.50 invalidating the longer-term bearish wedge pattern we were monitoring. Bullish momentum since the 108.24 low is forming a steady trend on the four-hour chart and prices appear set to retest 110 for the first time since May. Given the strength of the last four-hour bar, the swing low appears to be in at 109.37 so the near-term bias remains bullish whilst this level holds as support.

- Bulls could seek dips within the tight bullish channel.

- A break beneath 109.30 assumes a bearish reversal from the highs.

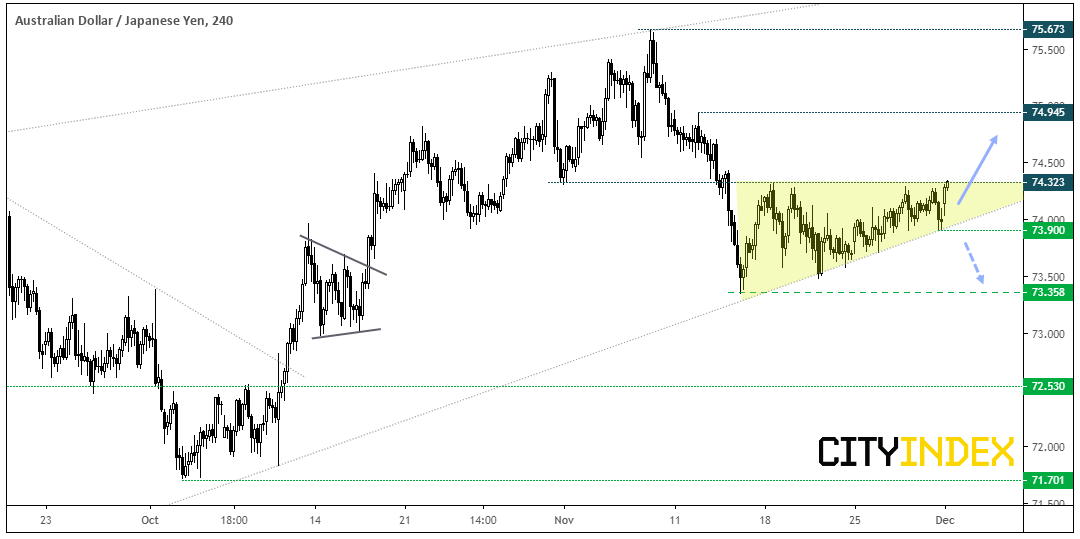

AUD/JPY is one to watch for a potential break higher, although keep in mind RBA hold their final meeting of the year tomorrow. By Friday’s close, RBA’s rate indicator suggested just an 11% chance of a -25 bps cut, although given that Westpac have now revised for them to cut two times and launch QE by June 2020, we could see some bearish follow-through on AUD pairs if RBA’s statement is perceived to be more dovish than November’s. Conversely, if they maintain their ‘steady as she goes approach’, we could just as easily see these pairs bounce higher.

Technically, prices action is supported by the bullish trendline projected from the flash-crash low. Today’s positive PMI reads has seen it rally into 74.33 resistance, although it appears to break it just yet.

- Ultimately, the near-term bias is bullish above 73.90 so traders could seek a break above 74.40 to assume bullish continuation.

- Whereas a break below 73.90 invalidates the bullish trendline and assumes further downside.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM