The deep sell off on Wall Street is spreading over into Europe, wiping out gains from the previous session. European bourses are a sea of red as risk off dominates amid rising concerns over resurging coronavirus infections and its potential to derail the fragile economic recovery.

Wall Street experienced a sharp decline after a series of warnings from the US Federal Reserve. Federal Chair Jerome Powell reiterated that the US economy still had a long way to go before recovery weighed on sentiment. His comments were supported by Fed Vice Chair Richard Clarida who considers the US economy to be in a “deep hole”.

The Fed sees a strong case for additional fiscal support. However, another rescue package before the November elections is starting to look very unlikely.

Evidence of the slowing economic recovery was evident in yesterday’s PMIs, particularly in Europe where the srtvice sector unexpectedly contracted. With covid cases rising and restrictions tightening the situation is only going to deteriorate over the coming months.

Rishi Sunak to the rescue?

UK Chancellor Rishi Sunak won’t be making a budget this year, instead, he will roll out a winter economic plan to see the UK through the coming month, which are set to be extremely challenging. With the furlough scheme set to end of 31st October, the markets have been concerned with what’s next? The centre piece to Rishi Sunak’s plan, to be announced today, is expected to be a wage support scheme similar to that in Germany. A scheme to subsidise wages of people in part time work, replacing the more expensive £39 billion furlough scheme. This should mean that the 4 million or so people that are neither in employment or out of employment on furlough, won’t necessarily face a cliff edge. This should at least soften the blow to the economy.

UK Chancellor Rishi Sunak won’t be making a budget this year, instead, he will roll out a winter economic plan to see the UK through the coming month, which are set to be extremely challenging. With the furlough scheme set to end of 31st October, the markets have been concerned with what’s next? The centre piece to Rishi Sunak’s plan, to be announced today, is expected to be a wage support scheme similar to that in Germany. A scheme to subsidise wages of people in part time work, replacing the more expensive £39 billion furlough scheme. This should mean that the 4 million or so people that are neither in employment or out of employment on furlough, won’t necessarily face a cliff edge. This should at least soften the blow to the economy.

Whilst the announcement late yesterday helped lift the Pound versus the Euro, sterling has failed to gain ground versus the mighty US Dollar all week, owing to increased safe haven flows into the greenback.

Looking ahead German IFO business sentiment data and US initial jobless claims will be in focus for further clues over the health of these economies

Oil extend losses

Oil process declined on Thursday and are extending losses weighed down today, despite inventories falling by 1.6 million. Concerns that the economic recovery in the US is stalling and concerns that Europe will soon be under tighter lockdown restrictions is dragging on the demand outlook.

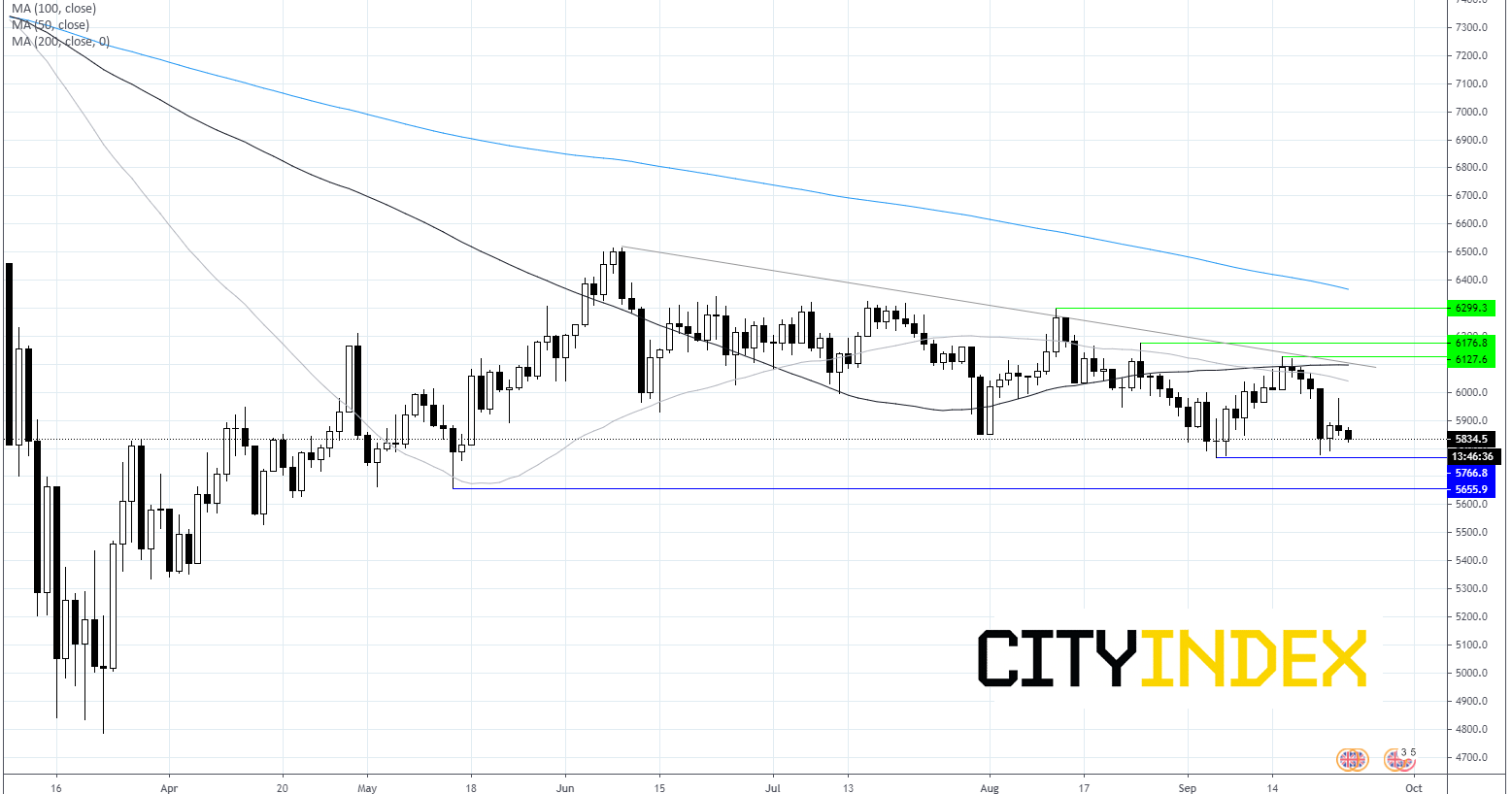

FTSE Chart

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM