Fears of a second wave of coronavirus persisted overnight dragging on risk sentiment, pulling Asian markets lower and setting European bourses up for a lower start on the open.

The number of cases in some US states are rising to record levels, which is unnerving investors. Texas, saw its largest daily increase in infections since the start of the coronavirus pandemic. However, it is worth keeping in mind that this is timing. Whilst states such as New York have passed the peak and are now reopening, some US states are experiencing the first wave of daily rises, just later. However, the chances of this spreading are still very real.Authorities in China have ordered the partial lock down of part of Beijing in an attempt to get a grip on the covid-19 spread in the capital city. The markets had been under the impression that China had stamped out coronavirus and was on track to reigniting the economy. The second wave of infections highlights the dangers of easing lockdown measures and reopening the economy. The latest developments in Beijing are dampening hopes of any quick economic rebound, feeding risk aversion.

BoE to increase asset purchases £100 billion

The BoE Is not expected to cut interest rates from the current 0.1% when it meets today. It is broadly expected to increase its Asset Purchase Programme by £100 billion. There is a good chance that some policy makers will be more dovish and push for a bigger increase.

Since the pandemic started the central bank has slashed rates from 0.75% to the 300 year low of 0.1%. It has also added £200 billion to its quantitative easing programme, taking the total to £645 billion.

The BoE Is not expected to cut interest rates from the current 0.1% when it meets today. It is broadly expected to increase its Asset Purchase Programme by £100 billion. There is a good chance that some policy makers will be more dovish and push for a bigger increase.

Since the pandemic started the central bank has slashed rates from 0.75% to the 300 year low of 0.1%. It has also added £200 billion to its quantitative easing programme, taking the total to £645 billion.

With inflation at a fresh 4 year low of 0.5% yoy and the UK economy having contracted by a quarter in just two months, March and April, the BoE will be under pressure to act meaningfully, boosting the prospects of a bigger than forecast £100 billion increase. With £100 billion priced in, any increase short of this amount will be viewed as disappointing and insufficient for dealing with the UK’s economic woes, a sell off in the Pound could be triggered, with risk aversion also dragging on the UK index. Similarly, a plus £100 billion increase could give the Pound a leg higher, whilst also boosting the FTSE.

Any comments surrounding negative rates will be closely watched. The negative rates idea gained some momentum at one point, with several BoE policy makers warming to the idea. However, BoE Governor Bailey has lowered expectations in recent public appearances, negative rates are not expected to be imminent if they happen at all. Too much discussion on the topic though could send the Pound tumbling.

US initial jobless claims a frustrating slow come down

Jobless claims are expected to increase by 1.3 million, down from the previous week’s 1.5 million. Whilst this will be the lowest increase in 3 months, it is still 6 x the pre-coronavirus February figure. Continuing claims are also expected to show a drop to 19.8 million, down from 20.9 million as starts slowly reopening and Americans are gradually rehired. The pace is frustratingly slow and suggests that another knockout month of retail sales is looking unlikely. A weak reading could feed risk aversion boosting USD and weighing on equities.

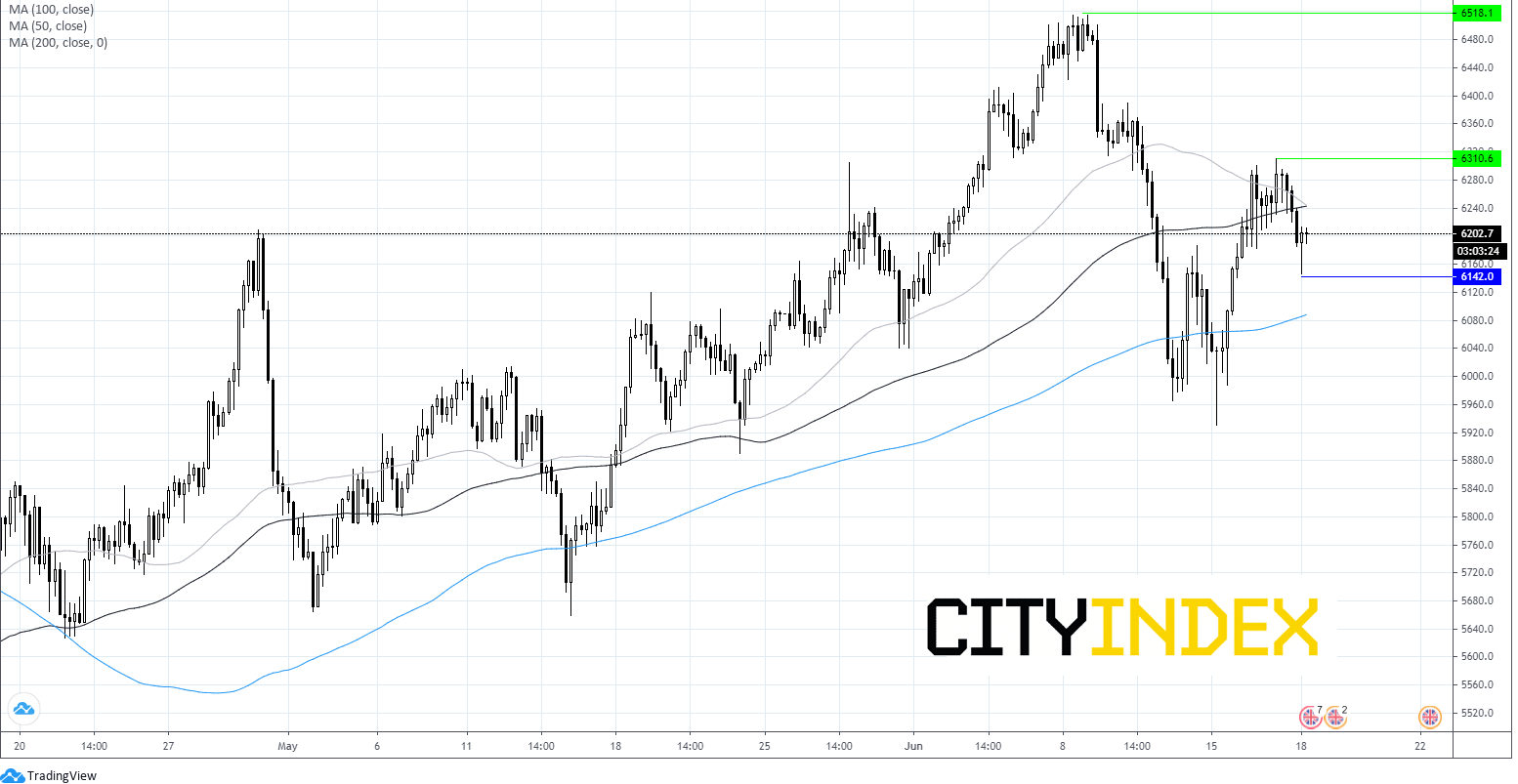

FTSE Chart

Latest market news

Today 01:15 PM

Today 07:49 AM

Today 04:24 AM

Yesterday 10:48 PM

Latest Central Bank articles

February 18, 2024 08:00 PM

January 31, 2024 01:31 AM

January 29, 2024 07:57 PM

December 26, 2023 09:27 PM