After a strong close on Wall Street, European stocks are looking to play catch up, although grim coronavirus statistics and growing fears over a second wave will keep risk sentiment in check.

Fears of lockdown restrictions being re-imposed or economies being reopened at a slower pace have weighed on sentiment across the week resulting in choppy trading and a constant struggle between the bulls and the bears. Whilst the FTSE closed the previous session in positive territory and aims for another jump higher on the open, the index is on track for a 2% loss across the week. Meanwhile the S&P is on track for a flat weekly move despite being up as much as 1.8% and down by as much as 2.4% at different points across the week.

In the US several states posted the highest one day increase in daily coronavirus infections whilst Texas has slammed on the brakes on its reopening plan, reversing course after just one month of reopening, as new cases hit a record 5996. Texas has been operating a more aggressive reopening plan, easing restrictions at as a faster rate that New York, which is still seeing improving stats.

US recorded its highest number of daily cases, with an increase of 42,000 infections. Concerns are rising that the fragile economic recovery could be knocked off track, however hope that stimulus could offset this is keeping the markets range bound.

US data in the previous session showed just how fragile the economic recovery is. Whilst durable goods soared, jobless claims showed that the improvement in the labour market is slowing.

With little on the European economic calendar to grab traders’ attention, a relatively quiet session is expected. In the afternoon, US Personal consumption expenditure and consumer confidence data could provide fresh impetus.

Oil extends gains, but remains cautious

After steep falls mid-week, oil continued its recovery, extending gains amid hopes of continued fuel demand recovery. Satellite traffic data from China, US and Europe is showing growing levels, boosting optimism surrounding fuel demand. Gains will remain capped as concerns surrounding oversupply linger following EIA inventory data showing a much bigger than expected inventory build, supporting a similar find from API data earlier in the week.

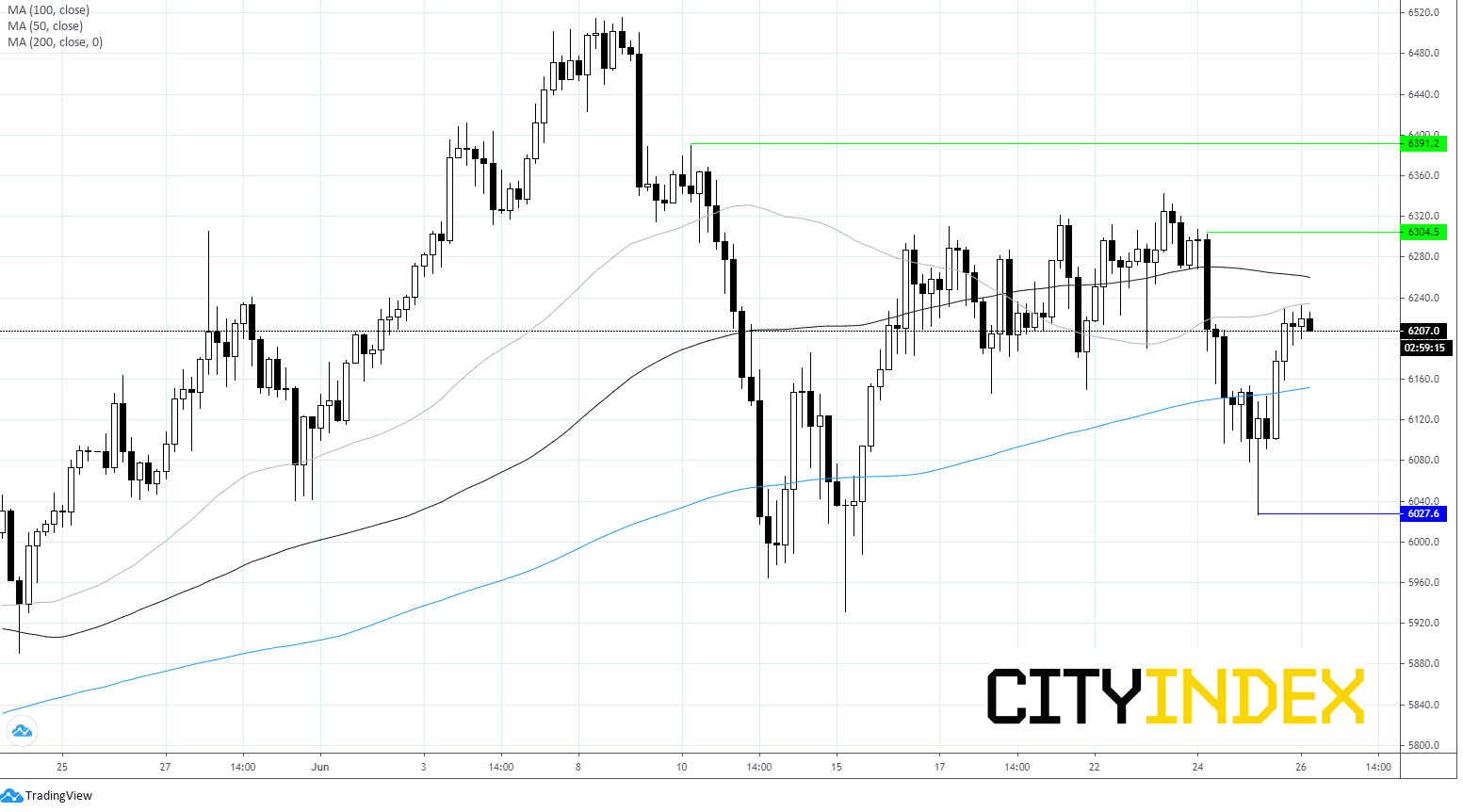

FTSE Chart

Latest market news

Today 08:33 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM