Rising price pressures to help GBP recovery

CPI data out later this morning is worth watching for a couple of reasons, it is expected to rise to 1.1%, which would be the […]

CPI data out later this morning is worth watching for a couple of reasons, it is expected to rise to 1.1%, which would be the […]

CPI data out later this morning is worth watching for a couple of reasons, it is expected to rise to 1.1%, which would be the fastest pace of price growth for 2 years, this comes at an interesting time for sterling as the market ponders another leg higher in its recovery.

Prices are expected to resume their upward trend after a 0.1% decline in October. Fuel price increases and a reduction in food price deflation is likely to drive CPI higher in November. The one-off factors that weighed on October prices, such as the large drop in clothing sales, are unlikely to be repeated in November.

Could an inflation overshoot be on the cards for November?

There is a small risk of a higher reading than 1.1%, but if CPI does come in line with expectations, this is likely to be the tip of the iceberg. The decline in sterling is likely to feed through to higher prices with a vengeance next year, and we are likely to see a breach of the BOE’s 2% target rate at some point in the next 6 months. Today’s price data may not warrant mention from the BOE at its meeting this Thursday, but it is likely to focus minds on upward risks to inflation and how the BOE plans to deal with it.

The UK consumer and rising prices

Rising prices could also raise questions about the future for UK consumption, a key pillar of GDP growth. Retail sales have held up well in the last few months as consumers brush off Brexit-uncertainty. A higher than expected inflation reading later this morning though, could trigger some concerns about how consumers can keep up their rate of spending without running their savings down to record low levels (the record low was 4.8% in 2008).

Interest rates may need to play catch up

Interest rates will also be in focus, the market does not expect UK interest rates to rise until the end of 2018, if inflation runs above target and consumption manages to hold up, then a delay of nearly 2 years before raising rates could seem excessive. Thus, a higher than expected CPI reading today could lead to a readjustment in the UK rate markets.

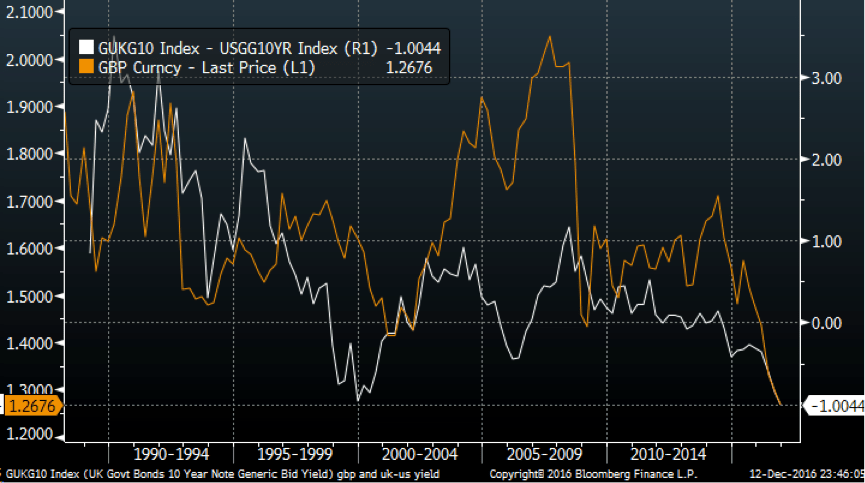

The chart attached is also worth watching. It shows GBPUSD (orange line) and the UK-US yield spread (white yield), which has diverged recently: as the yield spread continues to decline (US yields outpace gains in UK yields), the pound continues its recovery against the US dollar. In the short term, a rise in inflation in the UK could see a mini recovery in the yield spread, which would support another leg higher in the pound, GBPUSD could see back to 1.2770 – the 100-day sma and key resistance.

However, any recovery in the UK-US yield spread could be cut short if Janet Yellen and the Fed strike a hawkish note at their meeting on Wednesday. This yield spread is currently -1%, the record low from 1999 was -1.26%, so a hawkish Fed could see the market test this record low, which may hurt GBP in the medium term and cut short its rally. In GBPUSD 1.2420 is key short-term support, the low from 30th November.

Overall, inflation in the UK is likely to rise in November, and we could see expectations for a rate rise from the BOE shift forward from the end of 2018. While this could support sterling in the short term, the focus will shift to the Fed on Wednesday, and a hawkish slant from Janet Yellen could weigh heavily on the pound, as it may trigger a return to the record low in the UK-US yield spread

Figure 1: GBPUSD and UK-US yield spread, long-term chart

Source: Bloomberg and City Index