Rio Tinto 8217 s iron burden

Rio Tinto got more things right in the first half than mining rivals, including continuing to pay dividends, unlike fellow iron ore gargantuan BHP Billiton.

Rio Tinto got more things right in the first half than mining rivals, including continuing to pay dividends, unlike fellow iron ore gargantuan BHP Billiton.

Rio Tinto got more things right in the first half than mining rivals, including continuing to pay dividends, unlike fellow iron ore gargantuan BHP Billiton.

Debt reduction was also on track.

On Wednesday headlines have fixated on its interim profit falling to a 12-year low.

Yet there was no surprise in the result—in fact world iron producer No.2 beat most sensible forecasts and, including exceptional items, officially, the group made a profit.

Either way, it was able to book net cash from operating activities which was concerning, but at $3.2bn and 27% lower year-to-year, no disaster.

So why did its London stock slip on Wednesday? (Not to mention why Rio shares trade at a 35% discount to closely-matched BHP, and one which is not a great deal smaller against global miners of similar size.)

There’s no mystery; the answer is in its 44% revenue earner, iron ore. Even after rising 55% from the lowest prices in decades marked in December 2015, prices remain four times lower than their early 2013 peak.

Chinese, demand and consumption and even production (at the costlier end) looms large in this sphere.

Steel capacity reduction that began in the region this year provided a boost, though even top management of iron ore producers have been unwilling to spin it in a positive light.

“Ultimately, that excess of supply will drive prices lower than where they are currently”, said BHP Billiton CEO, Andrew Mackenzie, in March, downplaying the effect of restocking as seasonal, particularly whilst port inventory remained elevated. Anglo American’s chief expected things to remain “tough on the supply side for some time” for producers of the metal, which Anglo would remain, but less so as it gradually disposed of its iron mining businesses.

Rio is sticking with it. That exposes the £54bn group to the full force of continuing ‘backwardation’—that ominous market environment in which futures prices signal that it will be cheaper to deliver a commodity in future than buy it today. That’s great for consumers in theory, less so for producers.

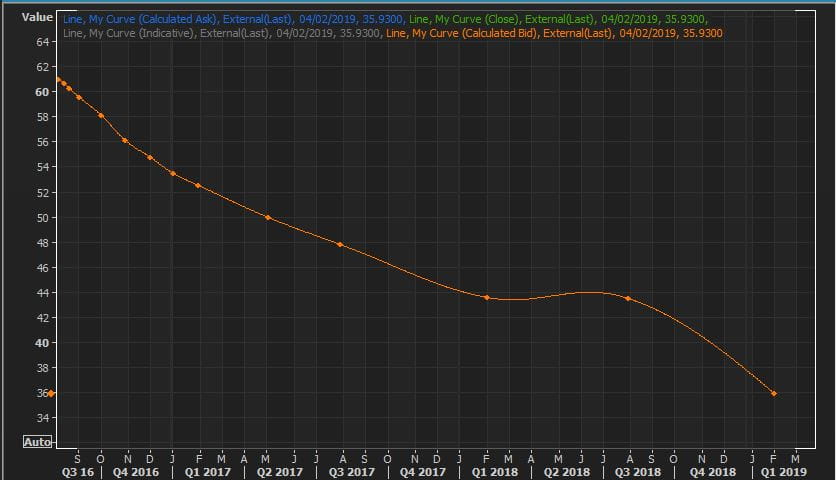

In Iron ore’s case, think as much as three years into the future, according to data from Thomson Reuters which I have charted below.

Source: Thomson Reuters / please click image to enlarge

Whether these projections turn out to be correct or not, the impact on the shares of the most exposed companies to iron prices is real enough.

And the tectonic nature of global influences on those prices means that whilst the outlook for prices is uncertain, the downside is compelling.

On that basis, Rio’s strategy of reducing costs and debt to protect its cash position—$3.25bn at end of its last fiscal year—makes sense.

It aims to keep shareholders on board by, almost uniquely among its class, continuing to pay dividends.

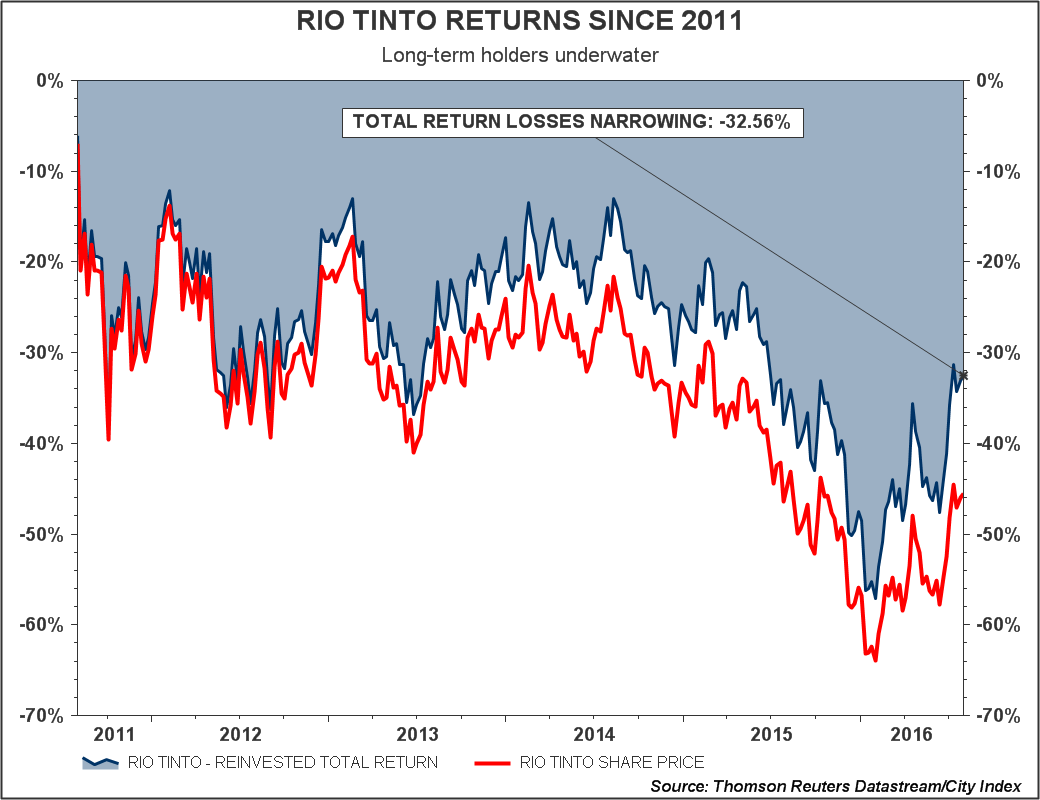

Unfortunately, for the strategy to make sense shares need to recover from a 40% loss over five years, which have meant dividends are merely bailing out already submerged returns to shareholders.

Please click image to enlarge

Perhaps mooted acquisitions in other commodities, particularly copper, might be answer, although Rio CEO Sébastien Jacques was keener to stress the group’s disciplined stance toward asset buys on Wednesday.

From a technical perspective shorter term traders will focus on testing the strength of the line on which the price has climbed since 20th July.

A short-term (and therefore likely weak) potential triangle breakout formation is visible in the hourly view, with a useful 38.2% interval at the equivalent of 2435p on City Index’s Daily Funded Trade (DFT).

A bullish outcome could offer the DFT a further attempt at the late July 2520p high. Failure should undo all the work since 20th July. That is unless the 61.8% Fibonacci at 2838p holds.

Please click image to enlarge