Rio BHP shares got short lived boost from China cut

Mining and China. We know they’re inextricably linked. China is the biggest consumer of commodity metals in the world. So whilst China’s cut of benchmark […]

Mining and China. We know they’re inextricably linked. China is the biggest consumer of commodity metals in the world. So whilst China’s cut of benchmark […]

Mining and China.

We know they’re inextricably linked.

China is the biggest consumer of commodity metals in the world.

So whilst China’s cut of benchmark interest rates on Friday was a surprise, it was still very consistent with the ‘pain levels’ being seen across various commodity benchmarks, prices and stocks.

For instance, the fall of the most widely used grade of iron ore on Thursday to a five-year low was just one notable marker of the extent to which Chinese demand for the commodity used to make steel for industrial and construction purposes had weakened.

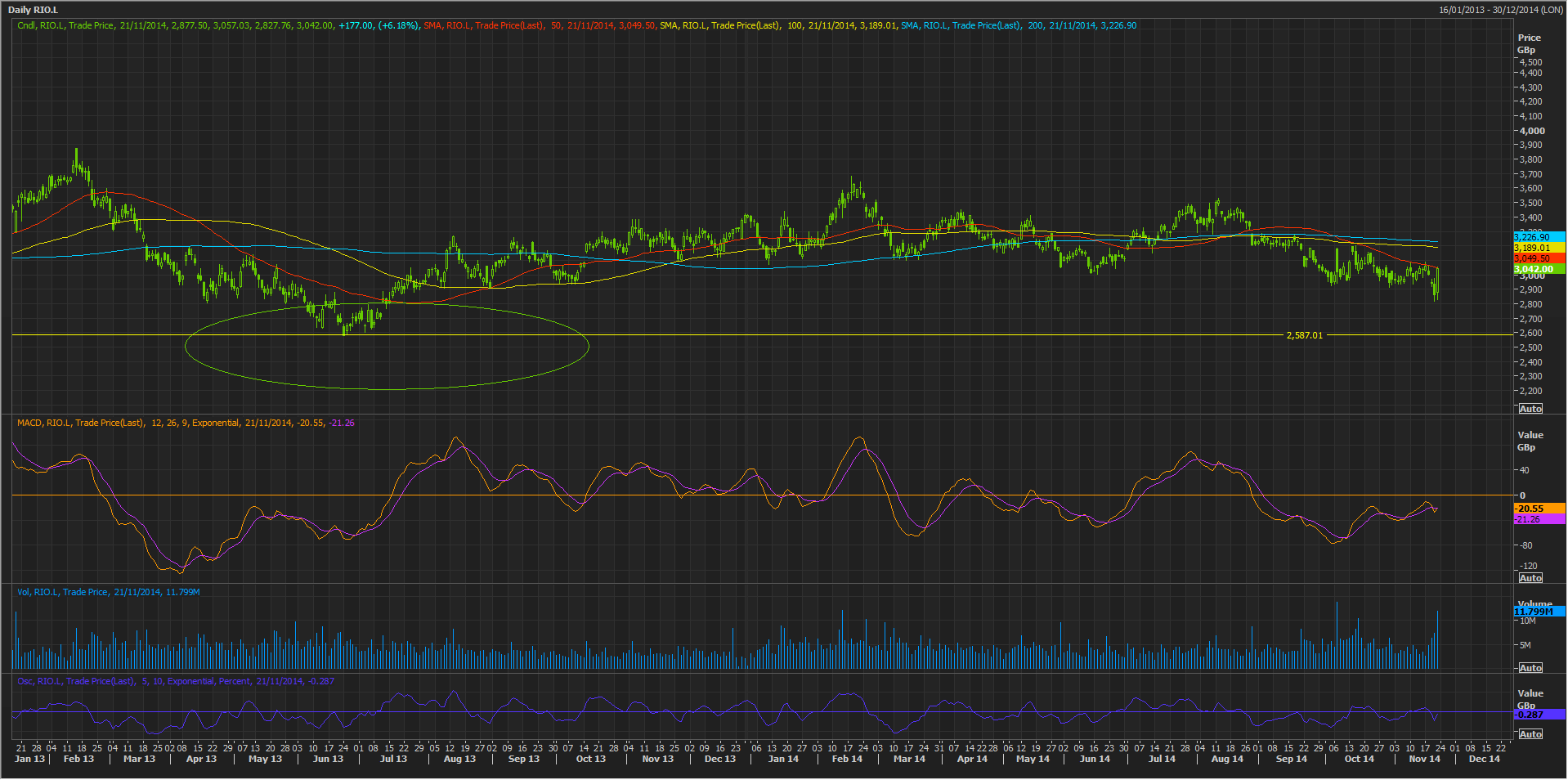

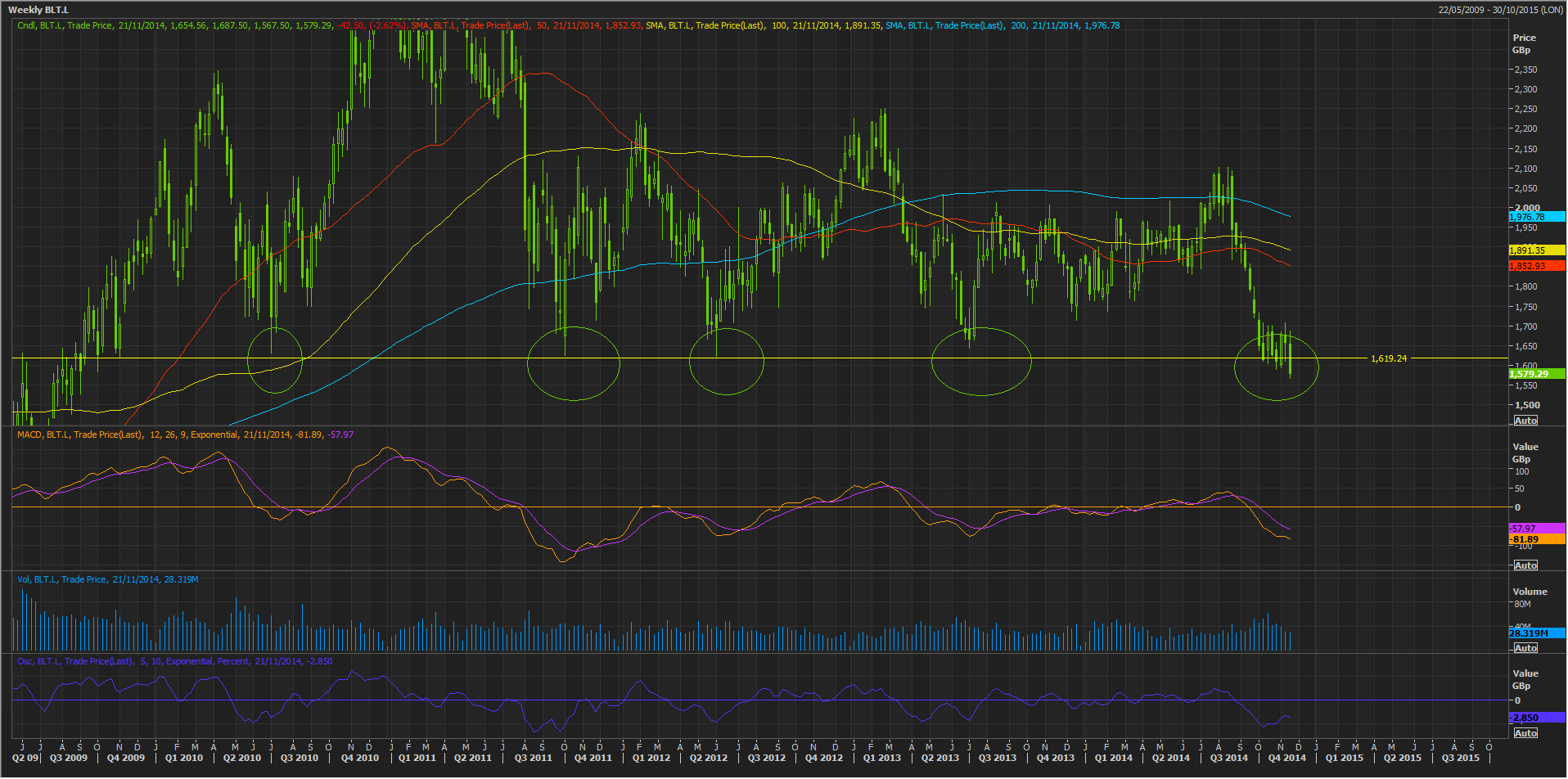

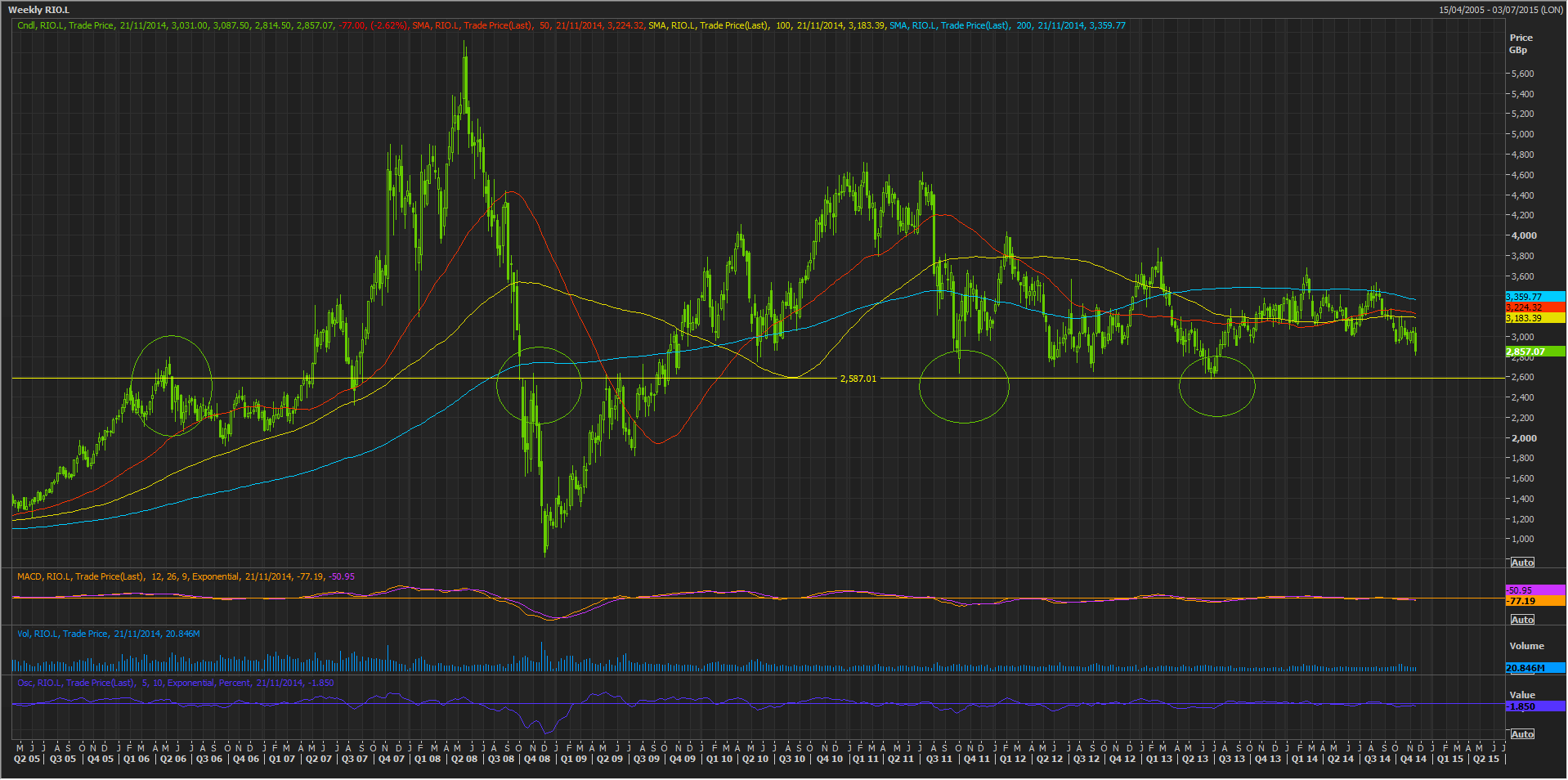

Shares of the UK’s biggest producers of the ore, BHP Billiton and Rio Tinto responded by slipping closer to important pivots.

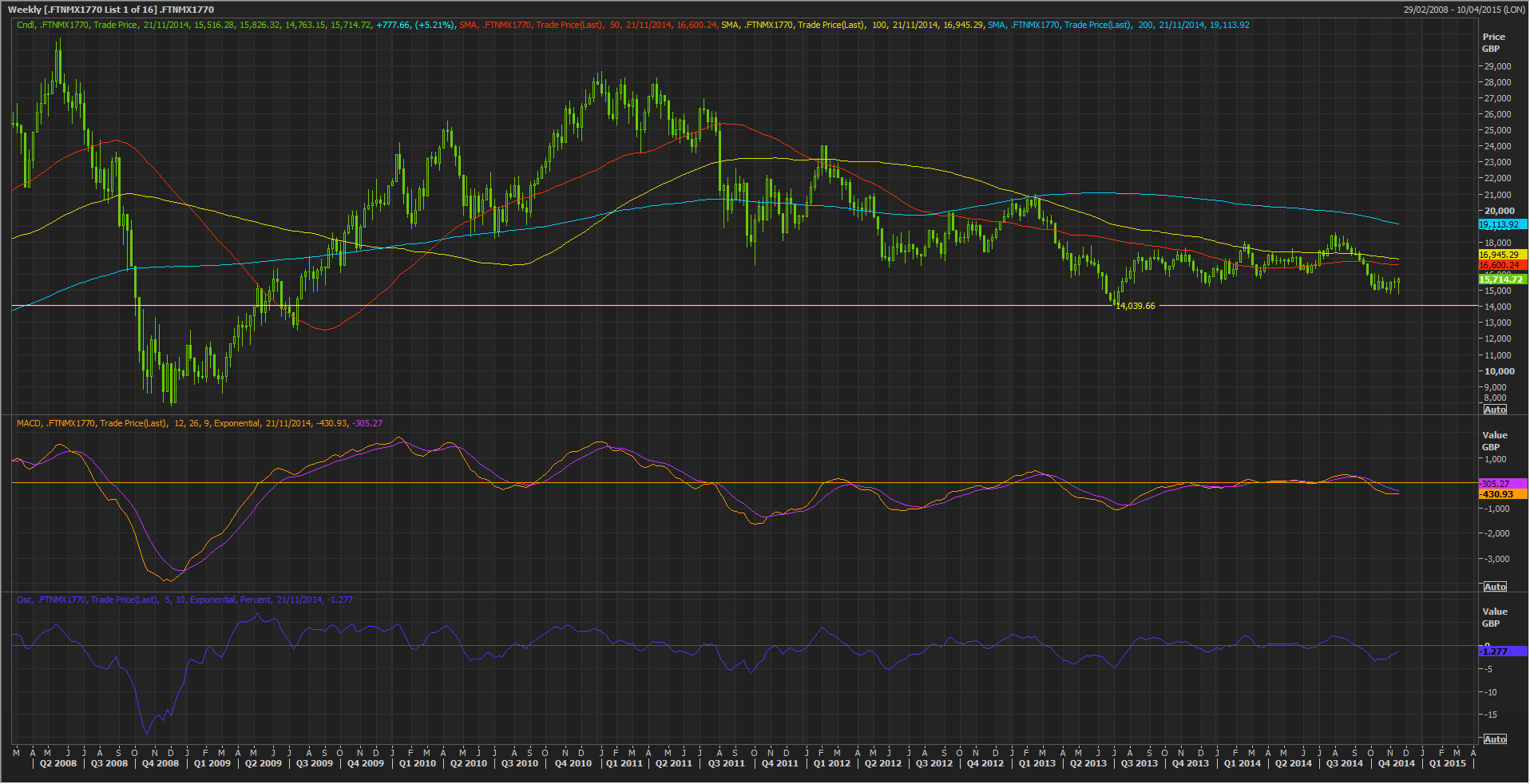

The two British mining giants would be sizeable constituent weights on the FTSE 350 Mining Index.

The weekly chart shows the index has been wandering back to an important pivot around 14039 that’s been traversed several times in the last six years or so.

The People’s Bank of China (PBoC) cut of its one-year lending rate by 40 basis points to 5.6%, and one-year deposit rate by 25 basis points, seemed to call a halt to this type of slippage.

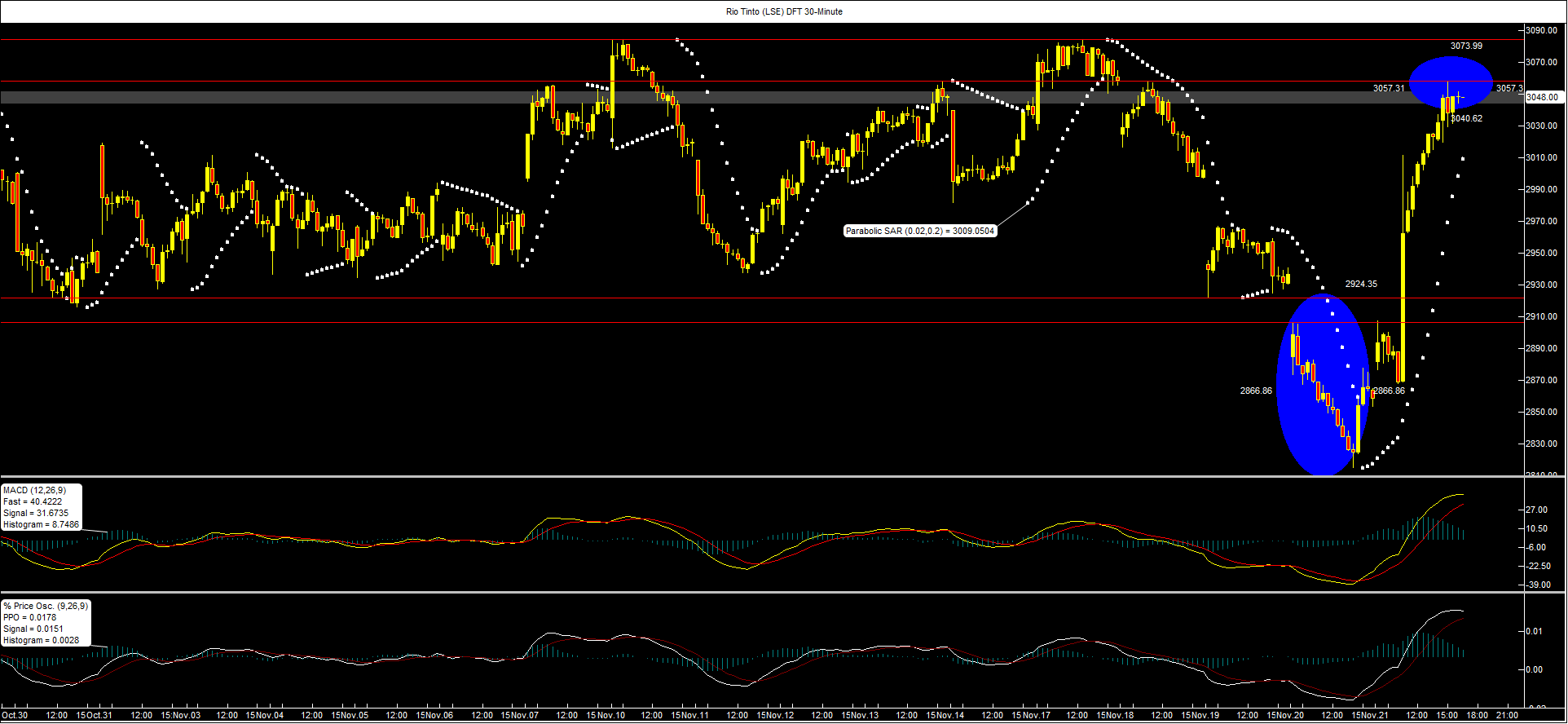

Even so, half-hourly intervals of Rio Tinto Daily Funded Trade suggest momentum provided by the central bank’s move may already have been exhausted.

The name, shown here in City Index’s Advantage Trader platform, bounced off a resistance close to 3058 in the last couple of hours of trade.

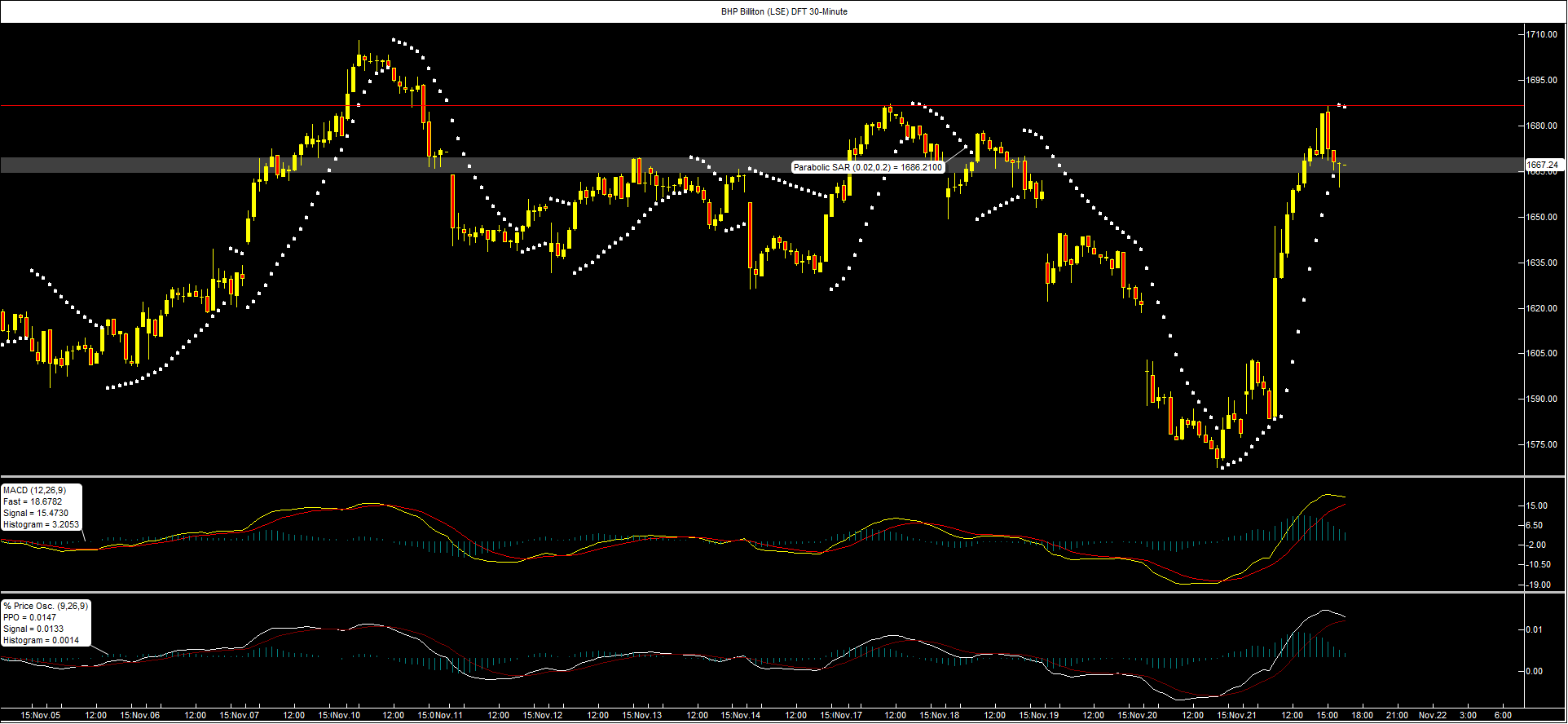

It’s a similar picture in the BHP Billiton DFT. It had already begun to rally before the PBoC’s announcement around 1030 AM, but the news gave the stock and City Index trade extra legs.

This puff seemed to run out around 1687. Even more so than the Rio chart, the give-back threatens to be just as aggressive as the ascent, though it’s worth cautioning that on a half-hourly basis, the bias of trade was still on the upside—albeit that was fading into the close. (Check the MACD and percentage oscillator).

It’s still too early to say whether these stocks have been effectively boosted out of range of the important (and quite magnetic) pivot lines I pointed out yesterday.

It’s worth noting the current record long dollar position (according to data from Thomson Reuters) may also argue for a structural net short position in mining assets that are exposed to dollar-denominated commodities, like iron ore.

The price of such materials tend to inversely correlate, to a varying degree, to periods of relative strength in the greenback.

{kind=link}

{kind=link}