Remember the US Trade Deficit

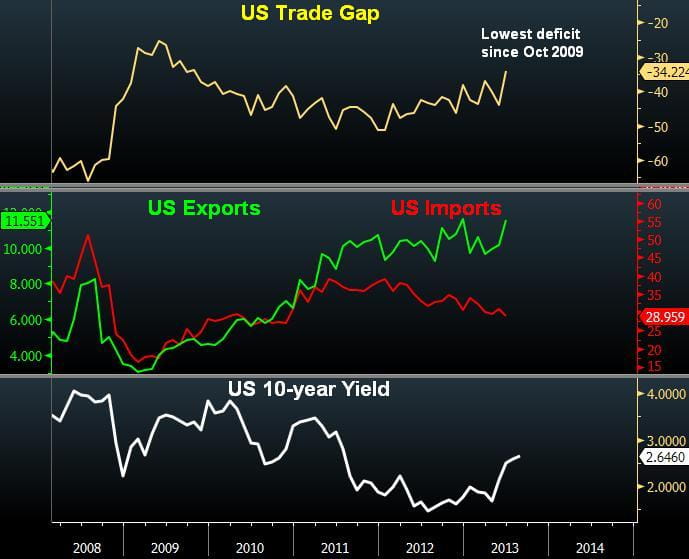

The US trade deficit fell by 22% to $34.2 bn in June, reaching its lowest level since October 2009. The 22% decline was the biggest […]

The US trade deficit fell by 22% to $34.2 bn in June, reaching its lowest level since October 2009. The 22% decline was the biggest […]

The US trade deficit fell by 22% to $34.2 bn in June, reaching its lowest level since October 2009. The 22% decline was the biggest in over 4 years. Currency traders haven’t focused on the US trade deficit since the mid 2000s, when it exceeded 6% of GDP. Today, it is half that level.

Today, the trade gap is down 34% from its 2012 highs. Over the same period, exports rose 62% and imports rose less than 2%.

Oil plays the biggest part the fall in the deficit. US petroleum imports have hit 3-year lows at $28.9 bn, while exports are near a fresh record high at $11.55 bn. US proven oil reserves are up 15%, posting second straight annual record increase. Rising shale developments in Texas and widening oil glut in North Dakota have contributed to the surge in reserves.

Due to US restrictions, all of US oil exports go to Canada. What happens to the trade gap if US oil is permitted to be exported to Europe and China? Would the US dollar rid of its external risk premium and regain its heights of early 2000s when the trade deficit stabilized near the $30 bn level?

Favourable Differentials

The difference between now and then is that the US trade gap rests on a falling trajectory for more than 6 months. And since June, interest rate expectations indicate the Federal Reserve is the central bank most likely to begin curtailing quantitative easing, preceding the BoE, BoJ and ECB. This is partly indicated by the fact that US 10-year yields stand at 2.64%, exceeding those in Canada, UK, Germany and Japan since March. This hadn’t happened since 2006. From a growth standpoint, Q2 GDP is likely to revised upwards to above 2.0% from the advanced release of 1.7%, following the latest trade figures.

Interest rate differentials, growth differentials and trade gap considerations; all point in the favour of the US dollar. But as the real world dictates, monetary policy considerations carry the most immediate weight on currencies –barring event risk such as credit downgrades or bailouts- Once the tapering ambiguity clears off, all that remains is that the Fed is the only major central bank positioned for a gradual scaling back. FX markets will have little choice but to adjust.