US tech stocks were in the firing line once again overnight with the Nasdaq weathering a 4% drop whilst Tesla tanked over 20%. The selloff in the tech heavy Nasdaq took the Nasdaq into correction territory for the second time this year.

Not only did Tesla miss out on S&P inclusion but GM buying up a $2 billion stake in Nikola is unnerving investors. Up until now Tesla has been without serious competition. However, Nikola is starting to look as if it could be in the running.

News AstraZeneca will halt all its vaccine trials as a participant in the trials appeared to experience adverse side effects initial sent the market southwards. It is standard procedure to halt vaccine trials in such circumstances for independent review and the market accepted the expanation without too much damage. The markets are particularly sensitive to vaccine news given that it is the surest and quickest route to return to pre-covid levels of economic growth.

The vaccine news comes as the British government bans the meeting of over 6 people in an attempt to stem the rise of covid cases, in a one two punch to sentiment. Yet despite the stacking up of bad news European market performed a serious U-turn on the open and are trading firmly higher across the board.

Brexit Hits Pound

The UK today will release its internal markets bill which has caused some controversy. Whilst the British government is painting this to be a tweaking round the edges of the Brexit withdrawal agreement and a clarifying of trade between the UK and Ireland, the EU is seeing this through a very different set of eyes. The EU is viewing this as an overriding of an international treaty and breaking international law, making the UK government appear very untrustworthy.

This latest development in the Brexit story is having a huge a big impact on GBP which has plunged over 1.3% yesterday and is off further today. GBP/USD trades over 2.3% lower this week so far, unwinding gains across the past month. A

There is a good chance that the Pound could extend losses now as we head towards the October 15th deadline as the reality of a no trade deal Brexit starts to hit home. Up until now there had been an assumption that the EU and the UK would pull the cat out of the bag and agree a deal at the last minute. Any tampering with the Brexit divorce bill would means the chances of a trade deal are significantly lower.

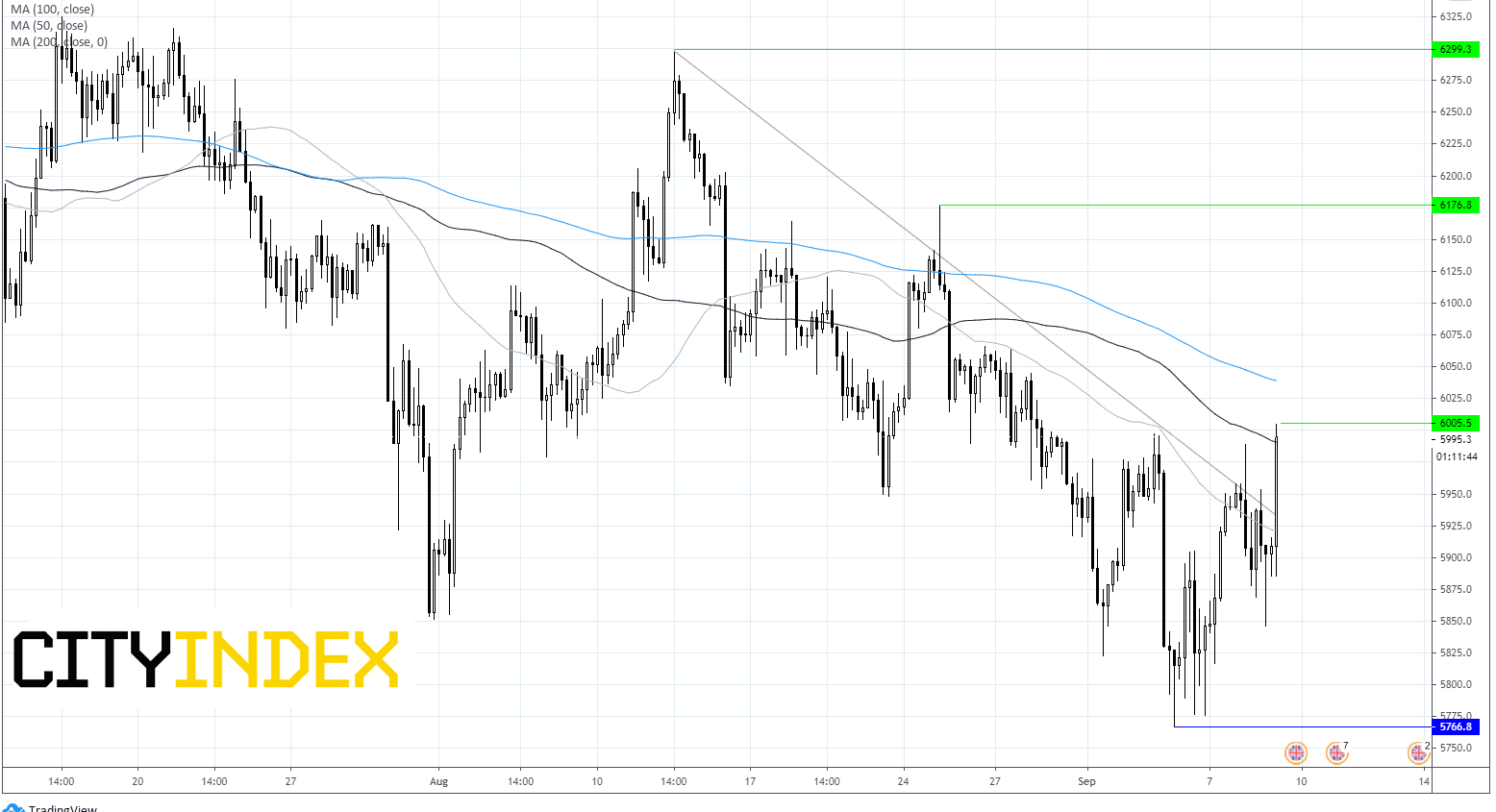

FTSE Chart

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM