RBS shares extend decline as FCA probe heats up

RBS made impressive progress towards its goal of becoming a “leaner, less volatile”, more boring bank, in the third quarter. But it also warned that […]

RBS made impressive progress towards its goal of becoming a “leaner, less volatile”, more boring bank, in the third quarter. But it also warned that […]

RBS made impressive progress towards its goal of becoming a “leaner, less volatile”, more boring bank, in the third quarter.

But it also warned that multi-billion pound compensation dramas were not yet a thing of the past.

The bank skimmed £10bn off Total Risk-Weighted Assets between the end of June and the end of September, leaving £316bn, well on course for its 2015 target of £300bn.

That looked even better compared with Barclays’ flat RWA outcome in Q3.

RBS also outperformed on Tier 1 Capital.

Regulatory reserves were beefed up to 12.7% from 12.3% in Q2, 1.5% higher since January.

Profit of £842m was adjusted to within an inch of credibility by RBS’s latest assortment of obfuscating exceptionals, absolvent impairments, and a one-off gain—£1.47bn—from ridding the balance sheet of Citizens.

It was a massive dip from Q3 2014’s £2.24bn, but just shy of £896m consensus.

‘Overlying’ this underlying income was an operating loss of £134m, down from £1.1bn income a year ago.

Blame restructuring costs.

It also emerged that RBS planned to make a final payment to the UK Treasury, formally ending an arrangement that gave the government priority over dividends.

RBS must pay the Treasury a further £1.2bn to terminate the ‘dividend access share’ that followed a £45.8bn bailout in the financial crisis.

“Given the full exit of Citizens, I think we’ve now got ourselves into a capital position where we can start to more actively think about repaying that,” RBS’s CFO Ewen Stevenson told reporters on Friday.

The bank announced a further offering of 110 million shares of Citizen Financial Group, equivalent to 20.9% of common stock.

Following completion of the second offer of Citizen shares within weeks, RBS will have fully divested its stake.

This and the end of the dividend arrangement would pave the way for for the government to sell its entire RBS holding, probably in 2016, having reduced it to about 73.2% in August.

If only things were that simple.

Experience shows it’s pretty much impossible for a Big 3 UK bank to get off scot free from mishaps during a quarter.

For RBS, fresh complication emerged on Friday that could hamper plans for a ‘new’ IPO.

It had to admit it may have underestimated costs for past misconduct—“substantially”.

Probes by US watchdogs after claims the bank misled investors in mortgage-backed securities, and an FCA investigation of its treatment of small businesses, have turned up costlier ‘nasties’ than thought.

RBS already set aside £4.5bn pounds for regulatory and legal actions.

There are no firm indications of how much more money the bank must set aside for fines and redress.

But its CEO Ross McEwan last month hurriedly convened an urgent briefing with senior executives after attending a meeting at the FCA about RBS’s Global Restructuring Unit.

The unit has since been wound up.

It’s alleged to have forced some small firms to default on loans so they could be charged higher fees.

Some former GRG clients have claimed they were made bankrupt, so their assets could be seized and sold.

“I think they’ve found something,” McEwan reportedly told his top managers.

A multi-billion pound compensation scheme was discussed at the bank in light of last month’s news.

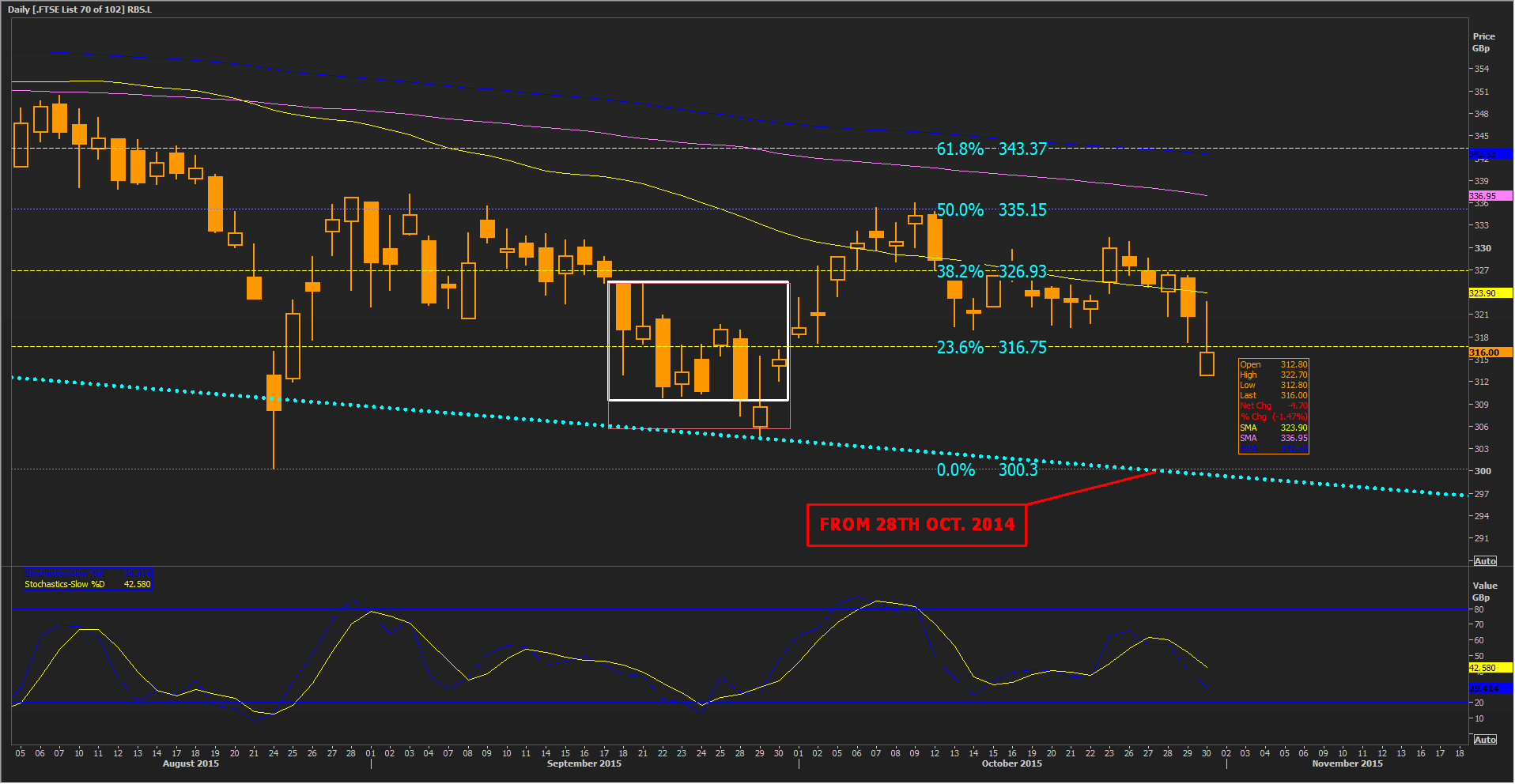

In lieu of clarification about this latest ‘black box’ issue for RBS, its stock will probably stay in the downtrend its UK sector has been in this year.

Thomson Reuters United Kingdom Banks Index is 12.5% lower year-to-date.

RBS itself has lost 24% since February.

In the near term, having crossed into a consolidation zone from September with a base at 307p, the shares risk a test of their 24th August low at 300p.

The stock bounced hard at an intraday low of 308p in July 2014.

That was the upper bound of a thoroughly tested zone beginning at 296p.

It supported prices between March and May of that year.

A severe compensation-related shock might be enough to burn the small barrier remaining to the psychological 300p price, bringing support mentioned above into view.

Please click image to enlarge