RBS reassures underpins shares

The two basic things RBS needed to get right during this quarter were: RBS makes hay 1. Keep a lid on the loan loss […]

The two basic things RBS needed to get right during this quarter were: RBS makes hay 1. Keep a lid on the loan loss […]

The two basic things RBS needed to get right during this quarter were:

1. Keep a lid on the loan loss situation—check. The economic upturn in the UK during the quarter has given British banks a window to skim some extra benefits out of net interest income and RBS has ‘released’ (to use banking terms) £801m this quarter, worth of funds that would have been set aside to cover bad loans, compared to the £590m the market was expecting.

2. Less control over this one—but the regulatory/legal side, including PPI insurance back-claims and currency manipulation provisions: RBS said it’s setting aside £400m for the currency fines, and adding a further £100m to provisions for compensating people miss-sold loan insurance.

These figures look to be in-line.

On pre-tax side, there will be no complaints that Q3 profit is £1.27bn compared to £1.1bn expected and a large rebound from a loss of about £634m brought about by various impairments in Q3 last year.

RBS later in the morning outlined conditions under which it would consider paying a dividend.

This will be moderately surprising to many investors.

A dividend was seen as a distance prospect, with the 80% government-owned bank widely expected to concentrate on clearing up a number outstanding regulatory issues in order that it could be as ship-shape as possible in preparation for the UK state to return the bank to the market by disposing of its stake.

(The government earlier this year cancelled a planned sale of a quarter of the shares it owns, on the basis that the stock was trading too weakly.)

RBS chief executive Ross McEwan confirmed this morning that the bank wanted to strengthen its capital position and get more clarity on misconduct charges, before considering a dividend. “There’s no way we will be paying a dividend until we get ourselves well in advance of that 12% target,” McEwan told reporters in response to questions on dividends.

The bank, had a core Tier 1 capital ratio of 10.8% at the end of the third quarter, strong enough to pass recent stress tests set by European regulators.

It has set a target of holding core capital of more than 12% by the end of 2016.

“I don’t think we should be thinking about dividends until we’ve got a really good capital build and seen some of the bumps in the road out of the way,” McEwan added.

Further out, RBS like all banks operating in the UK, faces the potential dilemma that will be triggered by interest rate rises. In the UK, this will be when the Bank of England increases its base rate from 0.5%, a level it’s been at for about 5 years.

This historic low has enabled banks to maintain relatively cheap lending rates, especially for mortgages. When it ends, with a likely 25-basis point rate increase, RBS’s current consumer loan mix and a leverage ratio that is up to 3.9% is widely expected to stand it in good stead.

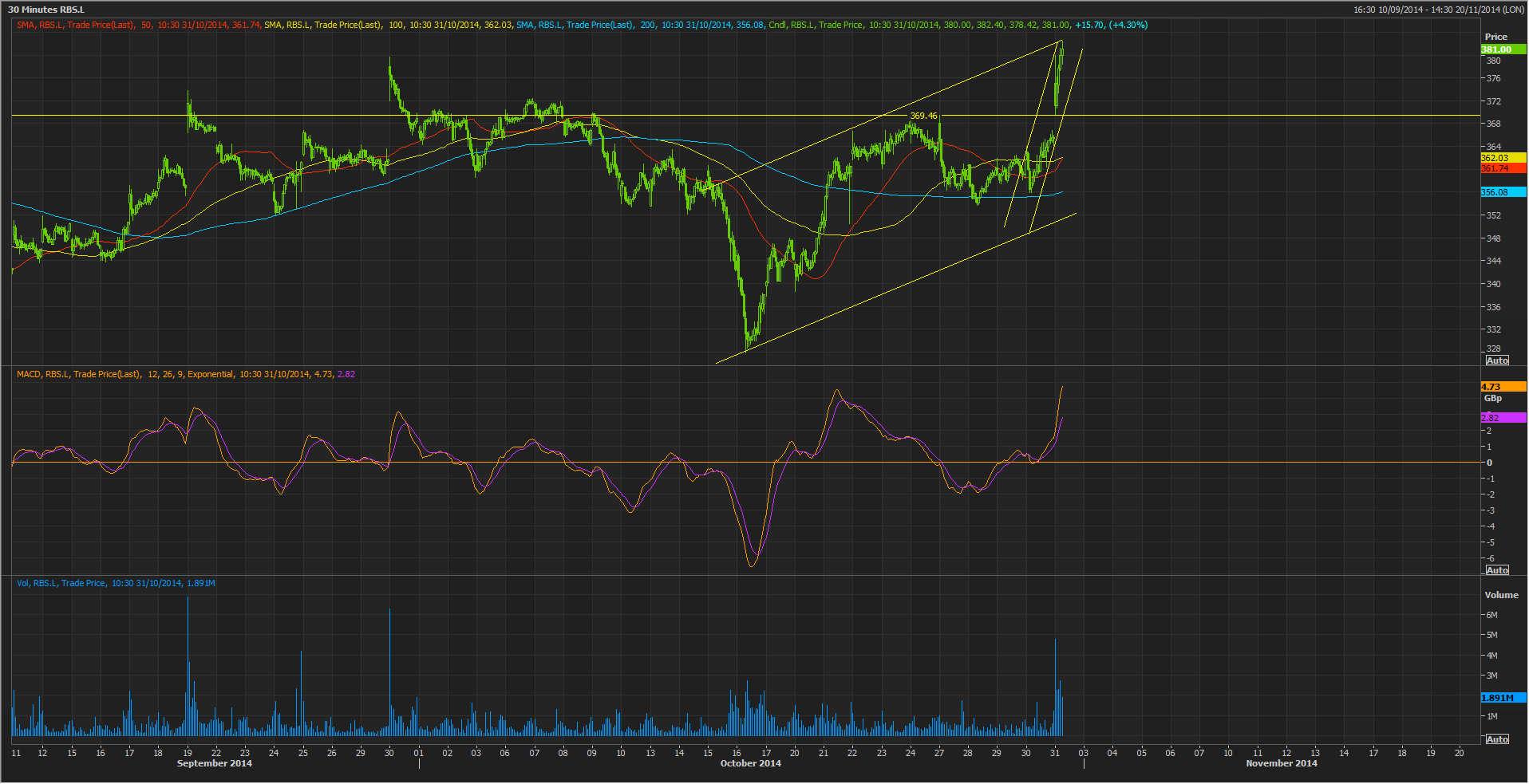

Taking this in combination with the dividend comments, we can see why the market has reacted well to the CEO spotlighting the conditions for a pay-out—adding an additional 1.5 percentage points or so to the stock’s already respectable rise of about 2.5% with the shares now trading more than 4% higher at 380p.

Investors seem to be concluding that the existence of any plan to eventually pay dividends is a positive, whilst at the same time no doubt aware that removing the ‘risk’ of dividend from outgoings will play well to the metrics outlined above.

The already promising broad trend of gains in the stock has been given an extra fillip this morning, with the probability of strong support beneath 369p from now on.