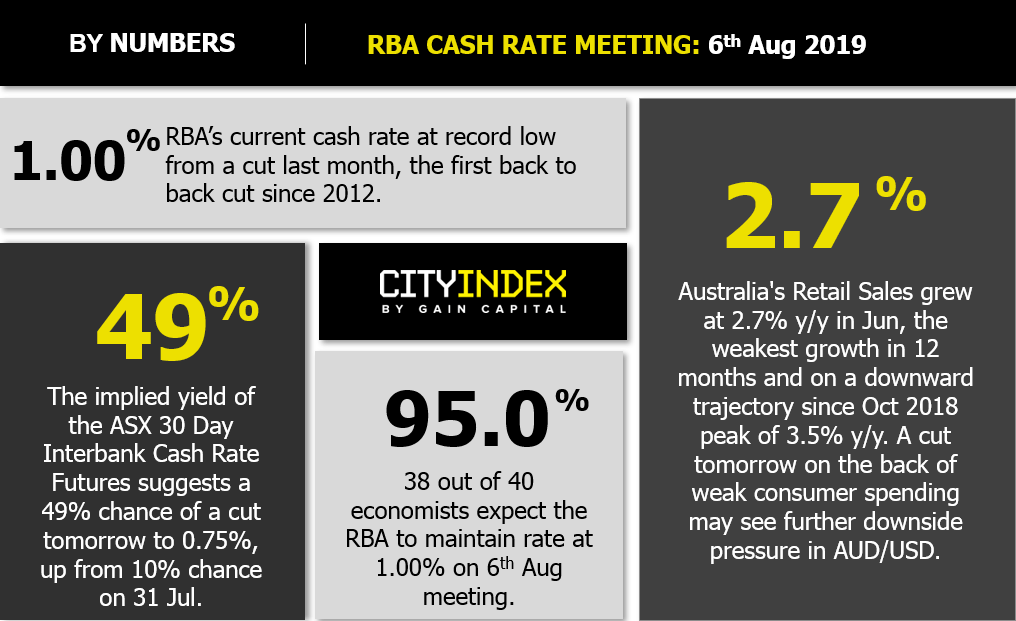

An overwhelming consensus (95%) from economists polled by Reuters expect no change in RBA key policy cash rate at 1.00% after tomorrow monetary policy meeting, a pause from the recent back to back interest rate cuts of 50 bps.

Interestingly, financial markets are not so complacent on a “stand pat” where the ASX interbank cash rate futures markets has indicated a 49% chance of another 25 bps cut tomorrow.

In his recent speech on 25th Jul, RBA governor Lowe has suggested a “what ever it takes” stance to grow the Australian economy even if that means slashing interest rates further. He also has cited that RBA will continue its best effort to get inflation to its long-term target range of 2%-3% where headline inflation has mostly been below 2% over the past four years.

Given such significant disparity of expectations between the interest rate futures market and economists’ consensus, an interest rate cut tomorrow, or a further dovish guidance may increase volatility and see further downside pressure in the AUD/USD.

There are several supporting factors to call for an interest rate cut tomorrow as follow;

- Australia’s retail sales for Jun came in at 2.7% y/y, its slowest pace in 12 months.

- Weak consumer spending has been accompanied by a deterioration in consumer confidence where the Melbourne Institute and Westpac Bank Consumer Sentiment Index has declined by 4.1% m/m to 96.5 in Jul 2019, the lowest reading since Aug 2017.

- Going forward, retail sales and consumer confidence are likely to see further headwinds due to an escalation of trade tensions between U.S. and China.

- China has “retaliated ” towards U.S. President Trump’s recent tariff hike of 10% on US$300 billion of Chinese imports by allowing the Chinese Yuan to shoot past the key 7.00 psychological level in today, 05 Aug Asian session where the USD/CNH (offshore yuan) has printed a current intraday high of 7.1122.

- A further weakening of the Chinese Yuan may trigger a “currency war” of among countries that are dependent on revenue from exports, thus exporting deflation globally which in turn weaken the demand of industrial commodities. Australia’s economic growth may see a double whammy of negative shocks from internal and external factors where her economic cycle is tied up closely with the demand for industrial commodities.

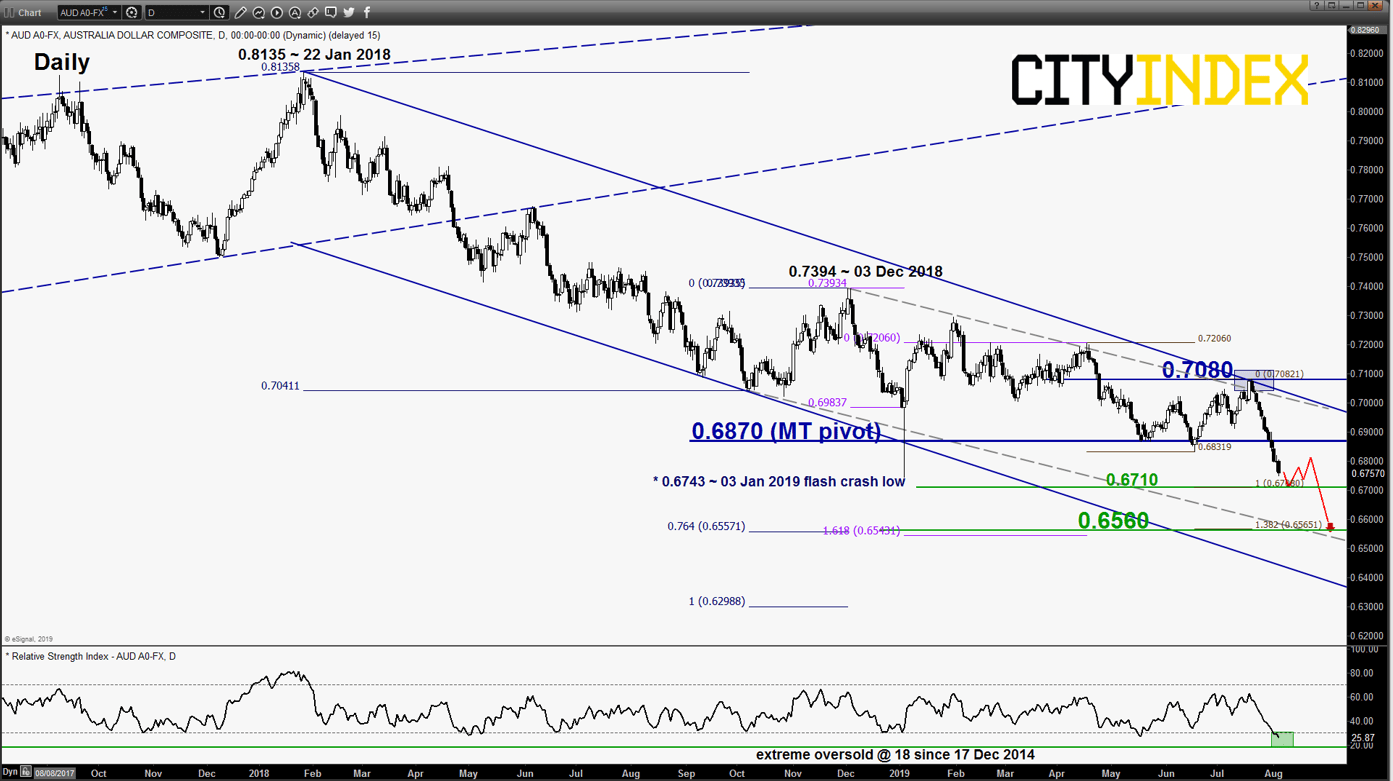

Medium-term technical analysis outlook on AUD/USD

click to enlarge chart

Key Levels (1 – 3 weeks)

Pivot (key resistance): 0.6870

Supports: 0.6710 & 0.6560

Next resistance: 0.7080

Directional View

Bearish bias in any bounces below 0.6870 key medium-term pivotal resistance for another round of potential impulsive downleg to target next support at 0.6560. On the other hand, a clearance with a daily close above 0.6870 negates the bearish tone for an extended corrective rebound towards 0.7080 (also the 18/19 Jul 2019 swing high).

Key elements

- Evolving within primary descending channel since 22 Jan 2018 high of 0.8135.

- The daily RSI oscillator is now coming close to an extreme oversold level of 18 where the Index may see a risk of a minor corrective rebound at the 0.6710 support due to an “overstretched” downside momentum in price action.

- The next significant medium-term support rests at 0.6560 which is defined by the lower boundary of a medium-term descending channel from 03 Dec 2018 high (depicted in dotted grey) and a Fibonacci expansion cluster.

Charts are from eSignal

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM