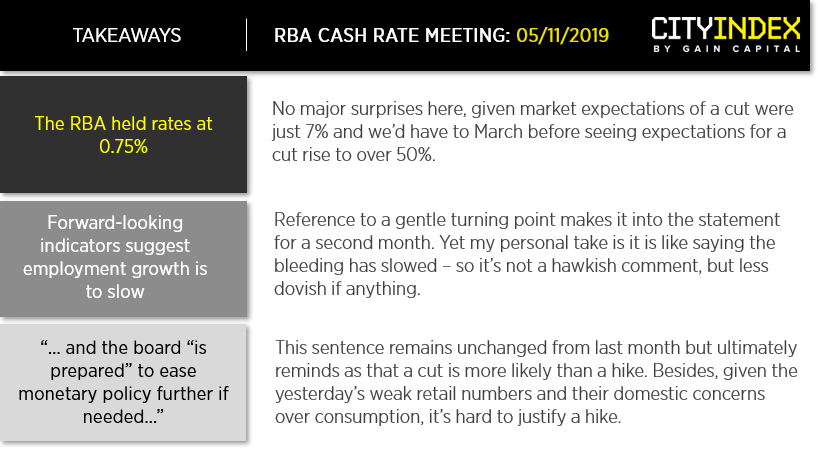

RBA held rates as expected, yet the easing bias remains despite talk of a ‘gentle turning point’.

Going into today’s meeting, expectations for a cut were low at just 7% according to the RBA Rate Indicator. But then they had cut rates three times over four meetings, and policy changes can take many months before their impact is felt by the broader economy. This may well explain why we have to go all the way into March 2020 before the expectation of a cut is above 50%, so there’s certainly been a change in sentiment in recent weeks. And as they’d discussed ‘keeping rate cuts on hold for a rainy day’ further suggests easing could indeed be on the back burner.

Still, whilst RBA are less dovish than they were, they still don’t appear hawkish. And its also possible the talk of QE may ramp up if data misses the mark over the coming months which could weigh on AUD, even if the prospect of further cuts don’t.

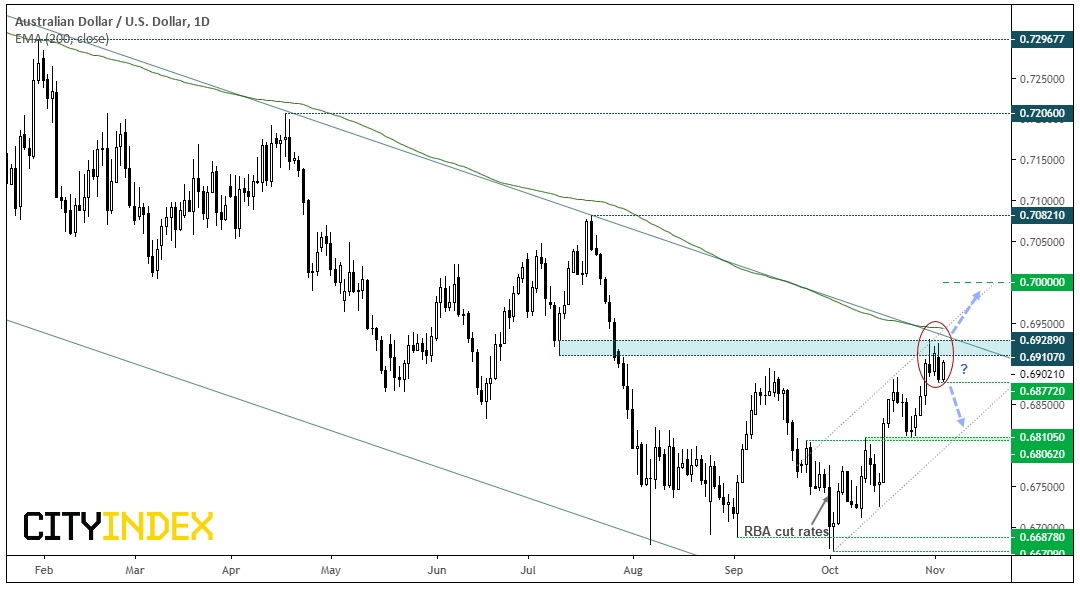

AUD/USD: We can see that RBA’s October cut provided its final drive lower before reversing course. A thaw in trade tensions and Fed cut have helped the Aussie rebound 3.9% from its low, yet prices have paused around a technical juncture. A bearish pinbar and bearish outside day shows traders struggling to push it above the July 10th lows, and of course we also have the upper bounds of the bearish channel and the 200-day eMA to provide further resistance as necessary.

- Prices are consolidating within a 50-pip range, although the four-hour trend is bullish.

- The bearish trendline and 200-day eMA make bullish setups on the daily timeframe less appealing, from a reward/risk perspective

- A break above 0.6950 brings 0.7000 into focus

- Whilst DXY holds above 97, AUD/USD has the potential to top out – although we’d want to see a break below 0.6877 before assuming downside

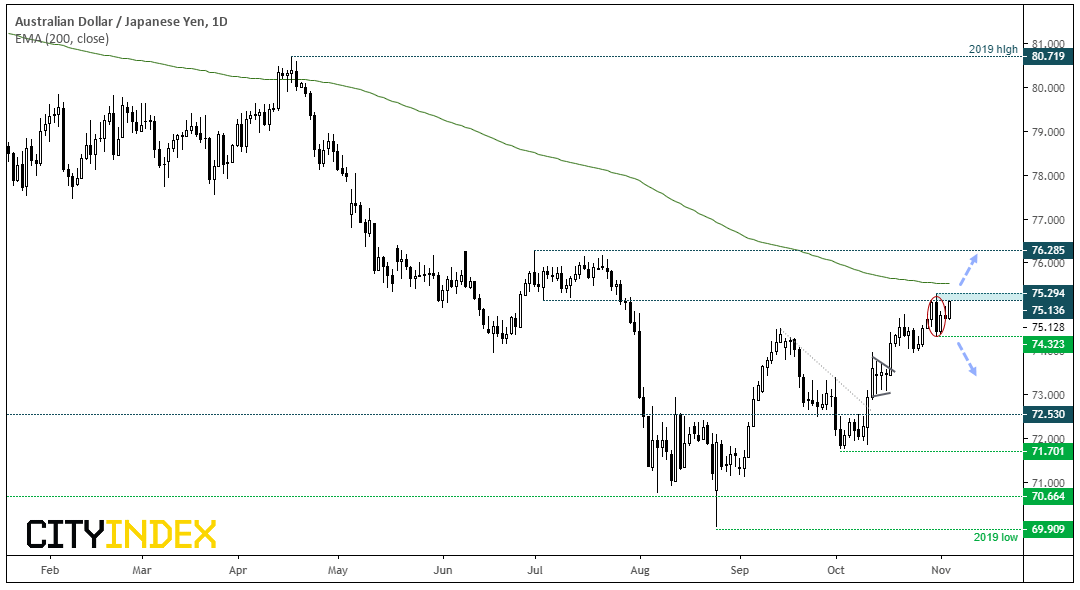

AUD/JPY: Its rally has paused after hitting its highest level since August and, like AUD/USD< trades below its 200-day eMA which can act as a level of resistance and erode away at risk/reward potential.

- A bearish engulfing candle marks a potential swing high just below 75.30, and bears could consider a break beneath its low of 74.32 to signal a bearish leg is underway.

- However, we’d suggest keeping an eye on indices and bond yields before becoming bearish on AUD/JPY; With US markets at record highs and yields perking up, it could throw a cushion of support under AUD/JPY and raise the prospects of a bullish breakout.

- Yet it could also be argued that yesterday’s pinbar reversal (and gap) on the S&P500 leaves potential for some mean reversion, which could help force AUD/JPY lower.

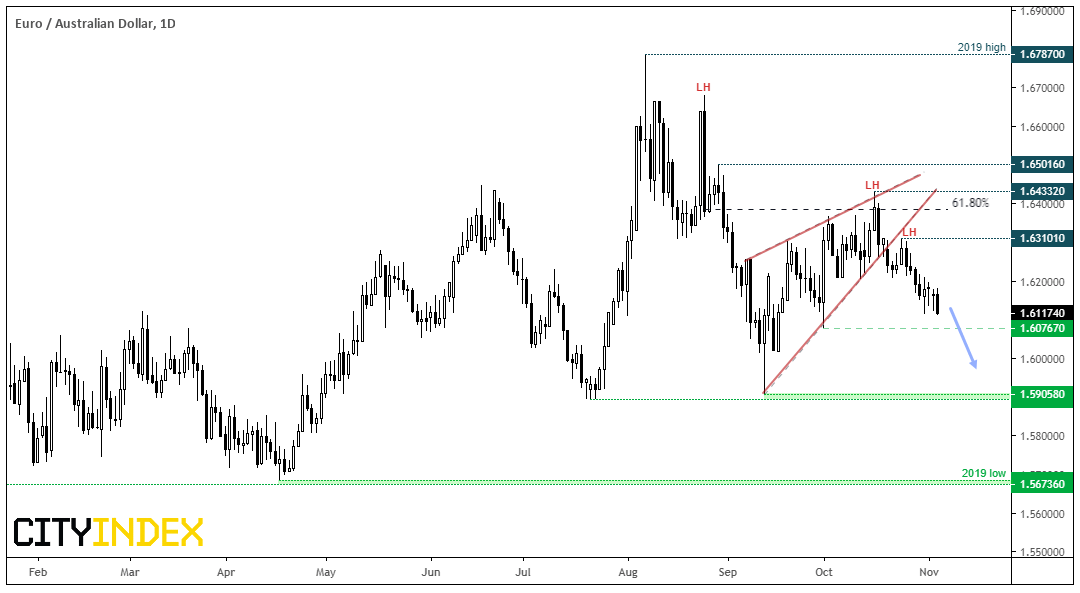

EUR/AUD: The bearish wedge remains in play which targets the lows near 1.5900. With support nearby at 1.6076, there’s potential for a bounce before its next leg lower resume. So bears could either wait for a retracement to fade into, or simply wait for a break beneath 1.6076.

Related analysis:

Weekly and Monthly Bearish Engulfing Candles Appear On DXY - But Just How Grizzly Are They?

AUD/USD Could Target 0.7000 if the RBA Strikes an Optimistic Tone

USD Could Be Approaching A Make Or ‘Break’ Scenario Leading Into NFP | DXY, EUR, AUD

AUD Firmer On Lower Unemployment | AUD/JPY, AUD/NZD, EUR/AUD

RBA Cut Rates To A Fresh Record Low

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM