RBA 8217 s Aussie Quandary

Reserve Bank of Australia Governor Glenn Stevens demonstrated today he’s running out of options to contain the rising Aussie. The RBA faces the quandary of […]

Reserve Bank of Australia Governor Glenn Stevens demonstrated today he’s running out of options to contain the rising Aussie. The RBA faces the quandary of […]

Reserve Bank of Australia Governor Glenn Stevens demonstrated today he’s running out of options to contain the rising Aussie.

The RBA faces the quandary of an overheating housing market, rock bottom interest rates but a strengthening currency. The central bank cannot cut rates any further due to fear of endangering a re-emerging housing bubble, while simultaneously facing a rising currency in a tepid economy.

RBA’s Stevens sought to cool off FX traders’ enthusiasm with the Aussie by indicating “…that at some point in the future the Australian dollar will be materially lower than it is today.’’ Stevens also acknowledged the Fed’s decision to put off tapering has been instrumental in the Aussie’s recent climb and that normalization of Fed monetary policy “would lessen some of the difficulties we face in our own policy choices.’’

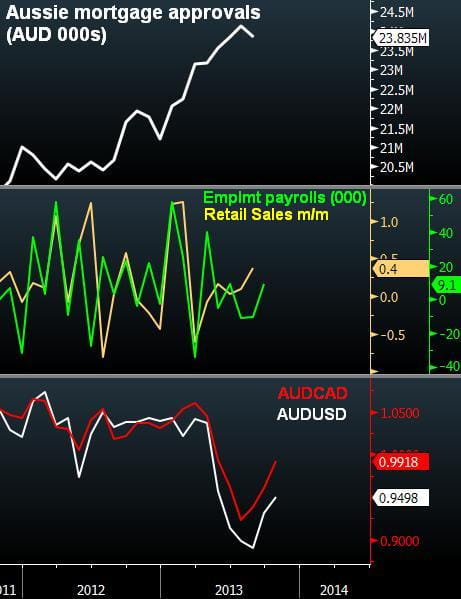

Caught between the taperless status quo in the US and a robust China, the Aussie’s path of least resistance is up. Verbal intervention may encounter diminishing returns as traders see little scope for another rate cut from the current 2.5%. Unlike in spring of this year when talking down of the Aussie was combined with aggressive easing, the situation is different. And with the value of mortgage approvals increasing 12% so far this year to attain 6-year highs, there is little room for easing.

When central bankers run out of policy options, they resort to verbal means as the Fed, ECB and BoE have demonstrated via vocal forward guidance. The RBA’s currency bluff may no longer work and as long as the Fed offers the opportunity for persistent carry plays, the Aussie will likely continue retracing against USD and CAD, regaining 0.9900 and 1.0400 respectively.