Global manufacturers would be hit hard…and China would be dented too

Rare earths weigh heavily

China's signal that it is "seriously" considering restricting exports of rare earths to the U.S. and that it has a detailed plan on how to do so, has helped extend the global stock market malaise beyond the one-month mark. As per other inflection points throughout the U.S.-China trade conflict, investors potential economic impact from disruptions to global supply chains whilst bracing for possible further escalation.

Rare earths are 17 minerals with highly sought-after properties that are difficult to synthesize on an industrial scale. The materials therefore see huge demand by manufactures of an ever-growing list of goods. Everything from batteries, lasers, lighting, automobiles (electric and combustion-driven) to electronic components, mobile phones, cameras, aircraft parts, X-ray and MRI equipment, require forms of ‘rare’ materials. And then there are the myriad military applications like missile guidance systems, satellites, night vision devices and beyond. Consequently, global supply chains could suffer severe disruptions that upend corporate profits and drag global economies into outright recession if China opts for aggressive restrictions.

Two-way street

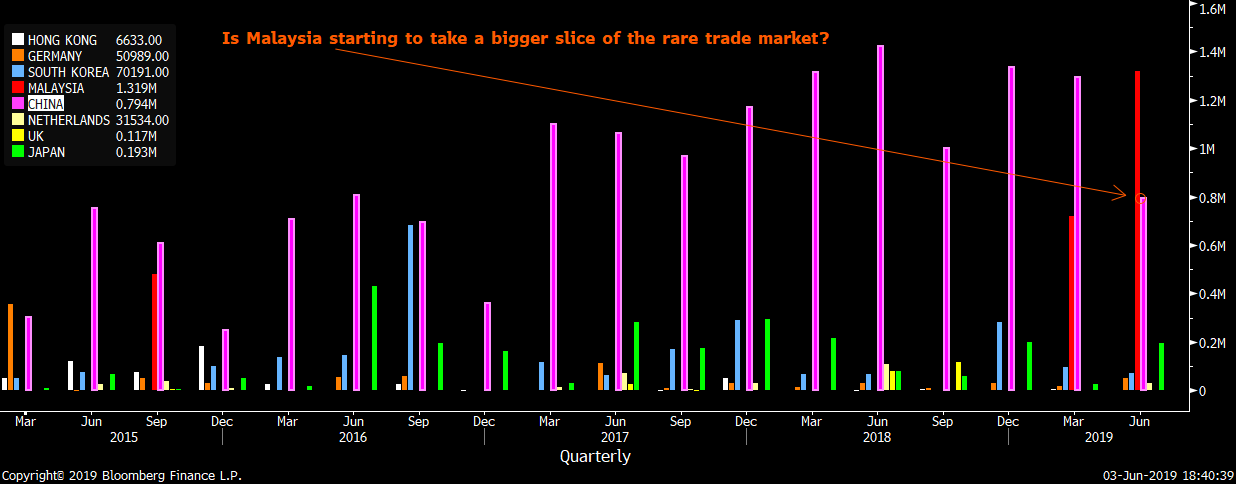

Still, if the world’s third-largest economy carries out its threat, recent history shows the damage wouldn’t be a one-way street. Sure, China dominates rare earth production, mining around 70% last year, whilst controlling 40% of global reserves. But it's more accurate to define rare earths as difficult and costly to mine than truly rare. As such, similar restrictions in the past enabled other countries attempting to scale production to grab market share. Malaysia and Japan itself are now also notable producers. Malaysia’s output has ramped in recent quarters as shown in the graphic below. With plentiful reserves in Brazil, Vietnam, Russia and elsewhere, such regions are likely to be inundated with incentives to hike their currently modest output; though that will of course take time.

Volume chart: principal country exporters of rare earth metals, including inorganic/organic compounds – March 2015 to June 2018

Source: Bloomberg / City Index

Unintended consequences

The history of attempts to ‘weaponize’ market resources also shows consumers generally reduce dependence, which eventually calls into question the benefits of any blockade relative to costs. China last attempted to leverage dominance of rare earths in 2010, when Beijing fell out with Tokyo over ownership of certain Islands south of Taiwan. China slashed export quotas and stopped shipments to Japan, but in many ways the move backfired. China went from 97% of global production to 71% in the five years that followed. Global consumption reversed from growth of 27% between 2005 and 2010 to a 7.2% fall in 2010-2015. China also faces erosion of an already patchy store of goodwill and reputation for reliability if it messes with rare earths.

Partly with these risks in mind, China is unlikely to immediately go all in with cuts. Instead, Beijing will probably burnish its leverage to Washington by curbing a little at first, as a deterrent.

Deep impact

Either way, rare earth prices will probably still spike. The cost of dysprosium oxide, a compound of a rare metal used in lasers and lighting, soared from $109 a kilogram on average in 2009, to $1,508/kg in 2011. There’s little reason why a jump in coming months would be more measured.

The 'cold trade war' between the world's two largest economies is unlikely to be resolved for several months. So stocks will be on the back foot for the foreseeable future, regardless of whether China takes a more aggressive stance or not. But the near future for risky assets will be even more turbulent with an added rare earth dimension.

The immediate stock market impact will probably be focused on sectors like tech hardware - including semiconductors and other components; automobiles and parts as well as large industrial manufacturers in general. That implicates the Asia-Pacific and European markets that dominate those spheres as well as the U.S.

Latest market news

Today 05:00 PM

Today 07:55 AM

Today 04:47 AM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM