Q2 earnings season gets off to a flying start

The markets had been expecting Q2 earnings season to be negative, with earnings and sales growth both dipping. However, that is not the way things […]

The markets had been expecting Q2 earnings season to be negative, with earnings and sales growth both dipping. However, that is not the way things […]

The markets had been expecting Q2 earnings season to be negative, with earnings and sales growth both dipping. However, that is not the way things are going so far. There have been some notable earnings beats with Google, Bank of America, and Citigroup all posting better than expected results for the three months to June.

Thank the consumer for the positive results so far:

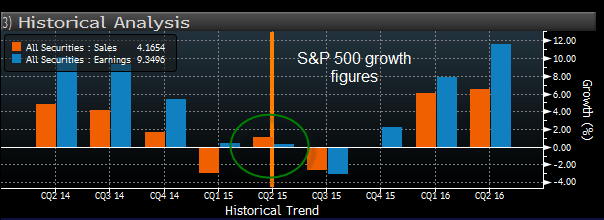

Although it’s early days and only 10% of all companies on the S&P 500 have reported earnings, the results look promising as both earnings and sales figures have surprised on the upside. Notable outperformers include the consumer goods, and financials sectors on the positive surprise front. On the growth front, basic materials, financials and technology have seen positive sales and earnings growth so far.

This has helped to drag S&P 500 sales growth back into positive territory, after it was negative in Q1, and earnings growth is also on track for a quarterly rise this year. This doesn’t mean that there are no weak links in this earnings season, the industrial and oil and gas sectors have been very weak so far. However, we will give them the benefit of the doubt at this stage since only 5% of oil and gas companies have reported earnings, so there is time for the earnings data to improve. Added to this, the bar for growth in both of these sectors is so low that some companies are bound to beat these forecasts.

Watch the technology sector:

The technology sector could be one to watch this earnings season after Google reported a 17% rise in profits in Q2. The detail of its earnings report was also strong, with an 11% rise in advertising revenue, and a strong pick up in volume.

Google reported earnings per share of $6.99, the market had expected EPS of $6.72, this was the first time that Google had beaten estimates for several quarters and the good news was duly reflected in the share price, Google’s pre-open quote on Friday suggested that Google’s share price could open approx. 11% at the open.

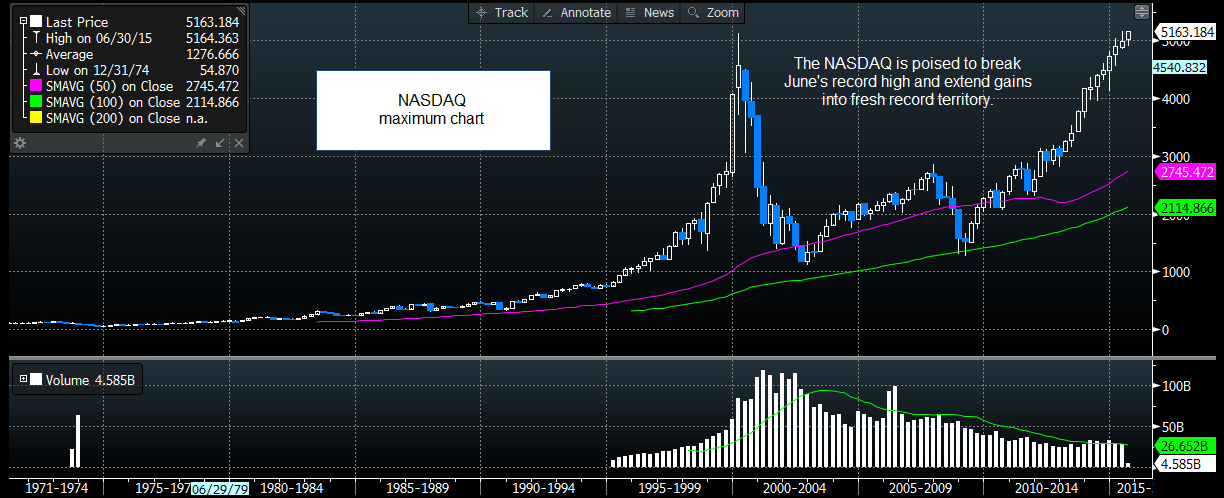

A rise of this magnitude could be enough to boost the NASDAQ technology index into record high territory. This sector has already had a fantastic run in the last 12 months and is up some 25% since October 2014. A sharp rise in Google’s share price on Friday could boost this index even further.

But can the tech sector sustain these lofty heights?

This may depend on how the other large tech companies fare during earnings season. Yahoo, Apple, and Microsoft all release earnings next week, while Twitter and Facebook both release earnings the week after. Watch out for Apple’s results. It has managed to consistently beat earnings forecasts in recent quarters, one quarter it has to slip up, surely? If it does so during this quarter then it may be the trigger for investors to take profit on their long NASDAQ positions.

Conclusion:

Overall, if we continue to see Q2 earnings season beat expectations then US markets may be able to extend recent gains and withstand the prospect of a rate hike from the Federal Reserve later this year. Currently the earnings season looks supportive of further gains in the US index.

However, the NASDAQ could be vulnerable to profit-taking now that it is close to a record high, and specifically if tech giant Apple finally misses earnings expectations when it reports next week.

Figure 1:

Source: FOREX.com, Data: Bloomberg

Figure 2:

Source: FOREX.com, Data: Bloomberg