Primark expansion keeps ABF shareholders sweet

Cheap and cheerful clothing is still a bigger money spinner than sugar beet processing. Once again, that’s the main takeaway from Primark-owner Associated British Foods’ […]

Cheap and cheerful clothing is still a bigger money spinner than sugar beet processing. Once again, that’s the main takeaway from Primark-owner Associated British Foods’ […]

Cheap and cheerful clothing is still a bigger money spinner than sugar beet processing.

Once again, that’s the main takeaway from Primark-owner Associated British Foods’ latest sales update out on Thursday, as it has been for at least a year.

Whilst the high street retailer of a full spectrum of discount clothing and accessories shows little sign of falling off its growth track—with gross sales up 9% (or +13% excluding currency impact) –ABF expects its sugar business to sour even further this year.

Profits from the division, most of which are lumped under the subsidiary AB Sugar, are forecast to fall significantly, as world sugar prices remain in a downtrend that has seen 66% wiped off prices since their peak in February 2010.

Currency impact is another considerable drag.

ABF said today currency effects are expected to take £25m off full-year revenues if current rates persist, bringing a “more significant” impact on results in the 2016 financial year, than the current one, which ends in September.

But investors appear quite unperturbed.

Much like the shoppers who flock in remarkable volumes to flagship Primark stores, ABF buyers continue to lap up the discount fashion story, and treat the rest of the group’s businesses as if they don’t exist.

That includes both the poorly performing sugar ops and the more solid ingredients division.

The stock has had two of its biggest one-day jumps during the last month since hitting two-year lows in October.

Including today’s rise, the stock is pretty much 30% higher since then, and more than 180% higher in a little under four years.

Primark store opening, Burleigh Street, Cambridge, November 2009. By Keith Edkins

Yet whilst the retail division continued to burn brightly in the third quarter, the group outlook for the year is more steady than stellar.

At the same time, Associated British Foods compares less favourably to both pure sugar rivals, and sugar-free retail competitors.

Net margins at both Marks & Spencer and Sports Direct beat ABF’s by 0.7 and 2.5 percentage points respectively, looking at their last complete fiscal years.

Struggling Tate & Lyle still managed 7.8% compared to ABF’s 4.4%.

Nor is free cash flow yield expected to be better at ABF than any of the above (apart from Tate).

It’s the expanding retail division, stupid – Primark revenues as a proportion of group total have now reached about 40%, compared to 23% in 2008. All other divisions are flat or slightly lower over the same seven years.

Even if ABF continues to run the ‘foods’ part at a loss for the next seven years, a rate of retail expansion that at least half matches its past would appear to stand the group in good stead with investors.

During that time, the sugar production glut may correct itself, at least enough to tilt in ABF’s favour, especially if we take the company at its word: it said on Thursday EU sugar prices, as reported by the European Commission, have shown some signs of recovery in keeping with quota inventory reduction.

Additionally, whilst another market that ABF participates in, bioethanol, is also weak, it expects a gradual rise of inclusion in fuel towards EU mandated targets by 2020, to move the market “from surplus to deficit”, leading “to a price increase over time.”

In the meantime, ABF will have to continue its retail expansion at the same near-breakneck pace.

Associated British Foods said it would open its first store in Italy in 2016, expanding into its tenth European market, whilst noting that preparations were well advanced for its first US store, in Boston, by September 2015.

So long as retail rivals stand still over the next few years, ABF can continue giving the impression of making gains at their expense.

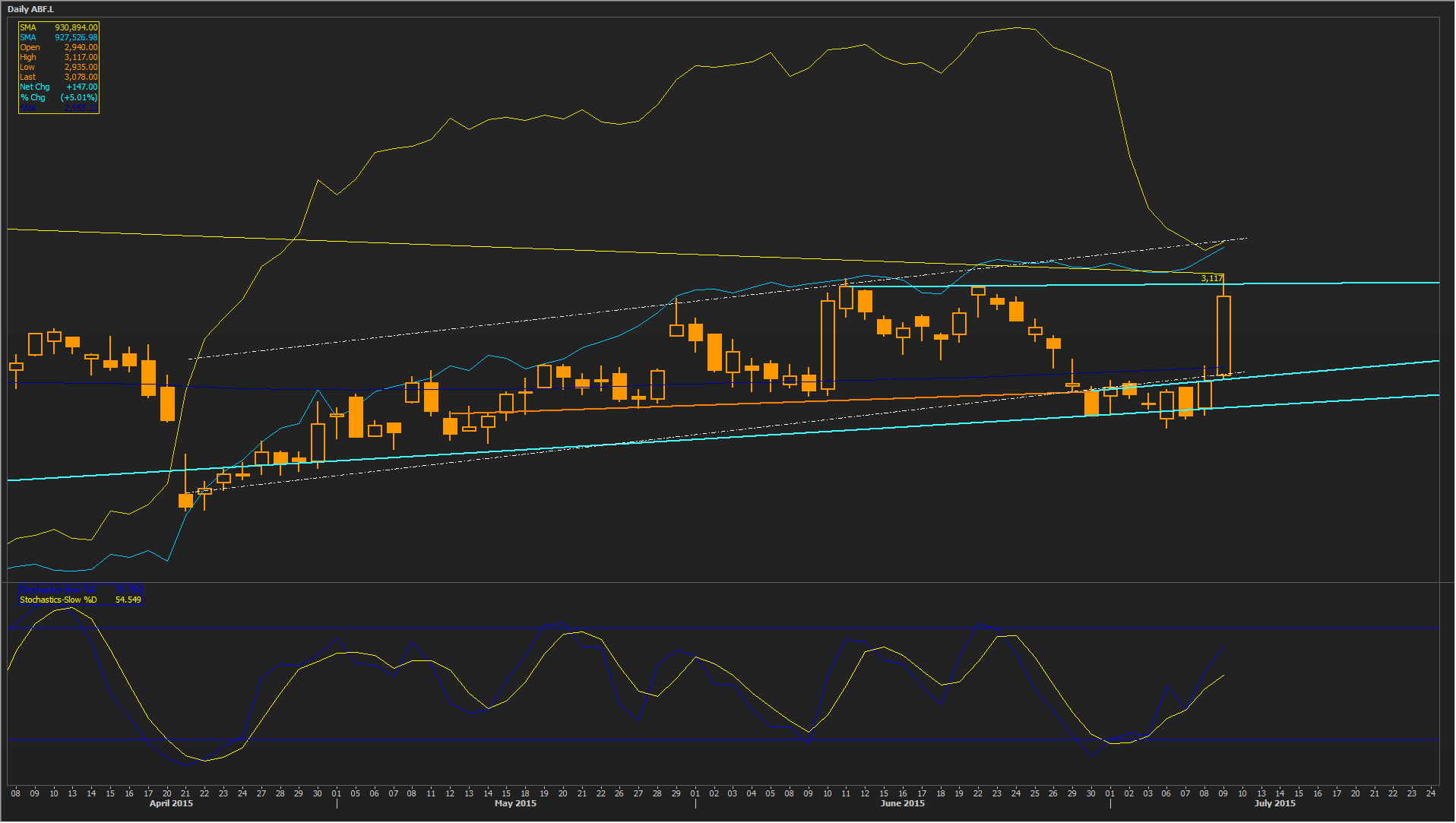

For now, the share price action looks constructive over the medium term, with what looks to be a more sustainable path back to all-time highs above 3280p seen in December, than the surge towards them last year.

Please click image to enlarge