Prepping for D day China Greece and the Federal Reserve in focus

Wednesday could prove to be a big day for financial markets ahead of the summer lull. Some major events are taking place, first up is […]

Wednesday could prove to be a big day for financial markets ahead of the summer lull. Some major events are taking place, first up is […]

Wednesday could prove to be a big day for financial markets ahead of the summer lull. Some major events are taking place, first up is the Chinese GDP figure for Q2, which is due for release at 0300 BST. Later in the day we should hear whether or not the Athenian parliament passes the reform package necessary to secure a third bailout. At 1330 BST Federal Reserve chair Janet Yellen is delivering her semi-annual testimony to the US Congress, so the markets will have a lot to wade through to determine the direction of markets for the rest of the week, or even the next few months.

To understand the potential market impact from these events, we will look at each of them individually:

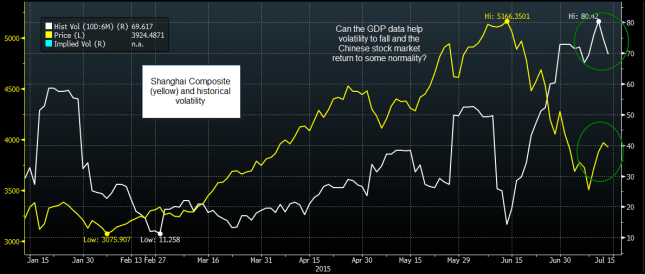

1, Chinese GDP data

This is important for two reasons: 1, the recent volatility in Chinese shares could be aggravated if we get weak GDP data, 2, the economy is expected to slow, we want to know if growth is in free-fall, or if it will slow at a measured pace.

As we mention above, the pace of the Chinese slowdown is critical to market sentiment, especially as the PBOC (Chinese central bank) has said that it will maintain “prudent” monetary policy going forward. The market expects a decline to 6.8% for annual GDP from 7%, while the YTD GDP figure is expected to slip to 6.9% from 7%, which was considered a line in the sand for Chinese growth. In fairness, the Chinese authorities have prepped the markets to expect a slowdown in growth in recent years, however, if we get a figure of 6.5% or lower than we think that this could spook global financial markets.

How this could impact markets: A weaker than expected reading of Chinese GDP could trigger a rout in commodities and further declines in the Aussie dollar and other Australian assets, which are sensitive to Chinese rates of demand. If we get a large data miss, we would expect volatility in the Chinese share market to surge, and stocks to fall, which could hurt overall global sentiment towards risky assets. (See figure 1).

2, Greece: To vote on reforms, or not to vote on reforms…

The next 24 hours will determine whether or not Greece will secure its next EUR 86bn bailout. The Athenian parliament has to agree to implement reforms by the deadline of 15th July, or this date could be used to commemorate another revolution –potentially the end of the currency bloc as we know it.

The consensus seems to be building that PM Tsipras will manage to secure enough support to pass the reforms and secure the cash. However, the political fall-out could be huge. Already some in Tsipras’s own Syriza party have said that they will vote against the reforms tomorrow, so Tsipras may need to rely on the opposition to get the bill passed. There is a chance that the current government could fall between now and Wednesday night, which could pave the way for a national or technocratic government during this time of crisis. While political uncertainty is usually a bad thing for financial markets, a technocratic government could be seen a positive thing as it could get the required bills passed through the Athenian parliament in order to release much needed funds during this period of crisis.

There is still a lot of uncertainty around bridging finance for Greece, which is vital if Greece is to meet its EUR 3.5bn repayment to the ECB next Monday. We also need to hear when the banks will re-open and capital controls lifted. Essentially, none of this will be secured until the Athenian parliament votes to accept the bailout reforms. If that doesn’t happen then all bets are off as the bailout will be invalid.

How this could impact the markets: Greece is still a trigger point for market volatility. If there is no vote, and no reforms are passed then we would expect risk to sell off across the board, particularly European stock markets.

The EUR is more difficult to predict. We would expect EURJPY to sell off sharply if there is an adverse outcome to the Greek crisis at this stage, sue to its sensitivity to risk sentiment. However, EURUSD actually fell on the back of Sunday’s agreement, so, if the vote is passed then we could see further EUR declines. If the vote is not passed and volatility spikes then downside for the EUR could be limited, especially if it causes an aversion to the carry trade. The EUR is a favoured funding currency for the carry trade, so if volatility spikes and carry trades unwind this could actually boost the EUR, at least in the short term.

Ultimately, if a Grexit looks like it will tear the currency bloc apart then we would expect a prolonged downtrend for EURUSD to parity and even beyond.

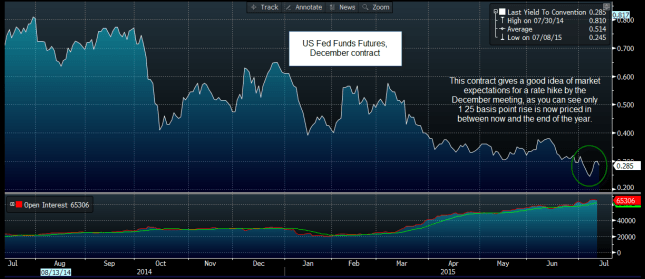

3, Yellen testimony: can the rate hike band wagon keep going?

The last time that Yellen addressed the public, she sounded fairly upbeat on the US economic outlook and the prospect for a rate rise this year. However, the financial markets (measured by the Fed Funds futures market) are less upbeat with just one hike priced in by the end of this year. Her semi-annual testimony to the US Congress on Wednesday is worth watching to see if she will: 1, look through the recent weakness of retail sales and stick to her guns that a rate rise is coming, and 2, whether or not financial markets will rush to price in further rate hikes this year, which could reignite the dollar rally. (See figure 2).

How this could impact the markets: If Greece calms down thenYellen’s testimony could be the last chance for some real market-moving action ahead of the quiet summer period. As we mention, if Yellen looks through the weakness of the US retail sales data and touts the prospect of another rate hike, then we could see the dollar reverse Tuesday’s losses and rally further. We need to get above the May 27th high at 97.75 to open the way to life above 100.00. If Yellen is considered too hawkish this week, then we could see US stocks struggle.

Overall, it could be a volatile second half of the week. This guide should give you some idea as to how markets may react on the back of these major events.

Figure 1:

Source: City Index, Data: Bloomberg

Figure 2:

Source: City Index, Data: Bloomberg