Prepare for market aftershock Brexit or not

Let’s face it, whatever happens Britain’s economy and financial markets are going to be stuffed for a while, whichever way the referendum vote goes.

Let’s face it, whatever happens Britain’s economy and financial markets are going to be stuffed for a while, whichever way the referendum vote goes.

The pound was still smarting on Friday after being ambushed earlier this week by polls showing a sudden swing back to Brexit. Bookies’ odds for ‘Leave’ have backed away from the shortest yet seen on Tuesday at 3/1 to 11/4. But sterling/dollar remained more than 2% lower than Tuesday’s highs.

Up until last week, the anti-Brexit trade was edging ahead, just like the ‘Remain’ camp. Sterling was buoyant, just ticks away from the year’s best levels set in May, and stocks strengthened enough to take all major British indices into the black year-on-year for just the first time since April.

Fast forward to now and the FTSE 100, FTSE 350 and the FTSE SmallCap Index are all back in the red year-to-date.

Well, British stock indices will almost certainly break out of tight ranges seen since March (apart from a couple of weeks in April). But whether they’ll sustainably rise or fall once the vote is out of the way is another question. The same goes for the pound. The Bank of England’s Sterling Currency Index was still down 4% for the year , after a bounce of about the same from 2016 lows in February.

Obviously post-vote market sentiment will very much depend on whether Britain decides to stay or go.

Let’s look at the market outlook in the event of the ‘Remain’ outcome first.

The remaining 4% trade-weighted pound decline will be erased. Maybe not immediately, but it will. Most sterling options trades have ‘skewed’ to puts—i.e., bets that the pound will fall near, or at expiry, enabling traders to sell the pound at higher than market prices.

But if Britain votes ‘Remain’, and the pound jumps, some losing traders will be obliged to buy the rocketing pound. That will exaggerate the move. Also, some punters eyed gains by the pound against the dollar of almost 20 cents, with ‘strikes’ as high as $1.65—14% above Thursday’s rates—expiring on 23rd June.

A more conservative estimate is that the pound would jump at least 4%-5% on the day a ‘Bremain’ result emerges.

However, there will also be an ‘aftermath of the aftermath’. When markets ‘unwind’ too fast, they almost invariably re-wind a bit pretty quickly too.

And that’s even before external risks to sterling are factored back in. Some pre-date the referendum campaign. The UK’s record current account deficit won’t have gone away. Slowdowns on the consumer side, in the job market and economy as a whole (GDP) won’t evaporate overnight and will drag the pound back.

Elsewhere, the Federal Reserve will still be beating the drum for a hike in July, powering the dollar and pressing on sterling, especially as a UK rate rise will probably be off the cards until 2H 2016 at the earliest.

Since the fate of the single-currency is as tied to the pound as the UK is to the Eurozone, sterling instability will be mirrored in the euro across the board.

The euro is up 5.8% this year, even after an erratic decline since April. Elevated euro volatility should bring a fall vs. the pound of at least 3% on the day a ‘Remain’ is confirmed.

Other influences, like a relatively resurgent Eurozone economy will then kick back in. But even the ECB said on Thursday it saw economic recovery “dampened by subdued prospects in emerging markets”, and the central bank lifted some inflation and GDP forecasts by just 0.1 of a percentage point.

Furthermore, the euro also faces dollar impact. Data last week showed the world’s biggest speculators on aggregate boosted bets in favour of the greenback for the first time in six weeks. That backed global consensus amassed by Thomson Reuters which sees the dollar ending 2016 under $1.10 vs. euro from $1.1155 on Thursday night. The same consensus calls EUR/GBP 3% lower by December.

The standard deviation of the last 20 sessions of FTSE 100 trading point to a maximum one-day move of just 1%. That makes sense considering how stagnant the index has been lately. But conversely, based on those maths, a relief rally should shoot far higher.

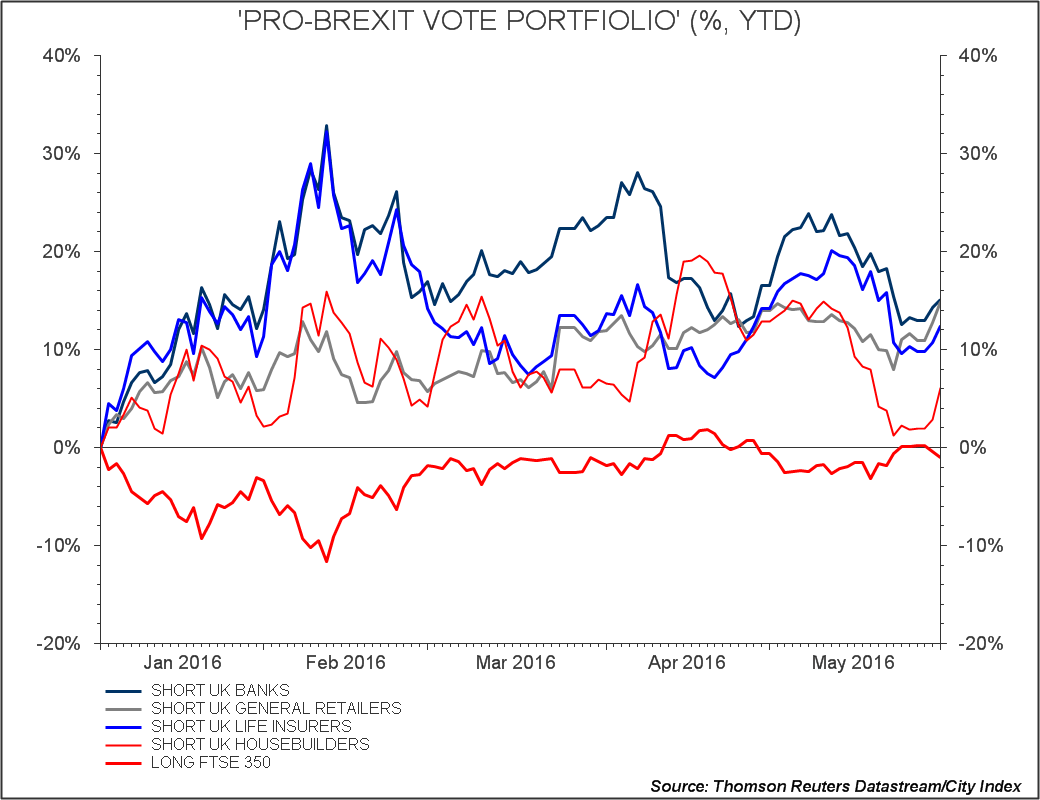

As for individual shares, we note the biggest UK losers have boosted returns in our ‘pro-Brexit portfolio’ well above the UK stock market average so far this year.

After the euphoria dies down though, these shares will still face outsize consequences for the vote taking place, regardless of the outcome. That’s because of their higher sensitivity to the pound. At worst, any lingering British and European political rancour which impacts UK economic expectations or trade, will bring continued headwinds for big banks, housebuilders, retailers and insurers, Brexit or not.

The best run companies in the above groups, with the most solid cash positions, will weather the post-referendum climate best.

Key takeaways:

If Britain votes to leave the European Union, the immediate reaction by markets will be extreme. Details are in Part 2 of this article.