Poundland shares could still get cheaper

Are you a Lidl person or a Poundland person? You’re likelier to favour Lidl, if your shopping habits have evolved with the new UK norm. […]

Are you a Lidl person or a Poundland person? You’re likelier to favour Lidl, if your shopping habits have evolved with the new UK norm. […]

Are you a Lidl person or a Poundland person?

You’re likelier to favour Lidl, if your shopping habits have evolved with the new UK norm.

But Poundland really needs to become the budget choice of more High St. shoppers, and that showed on Thursday.

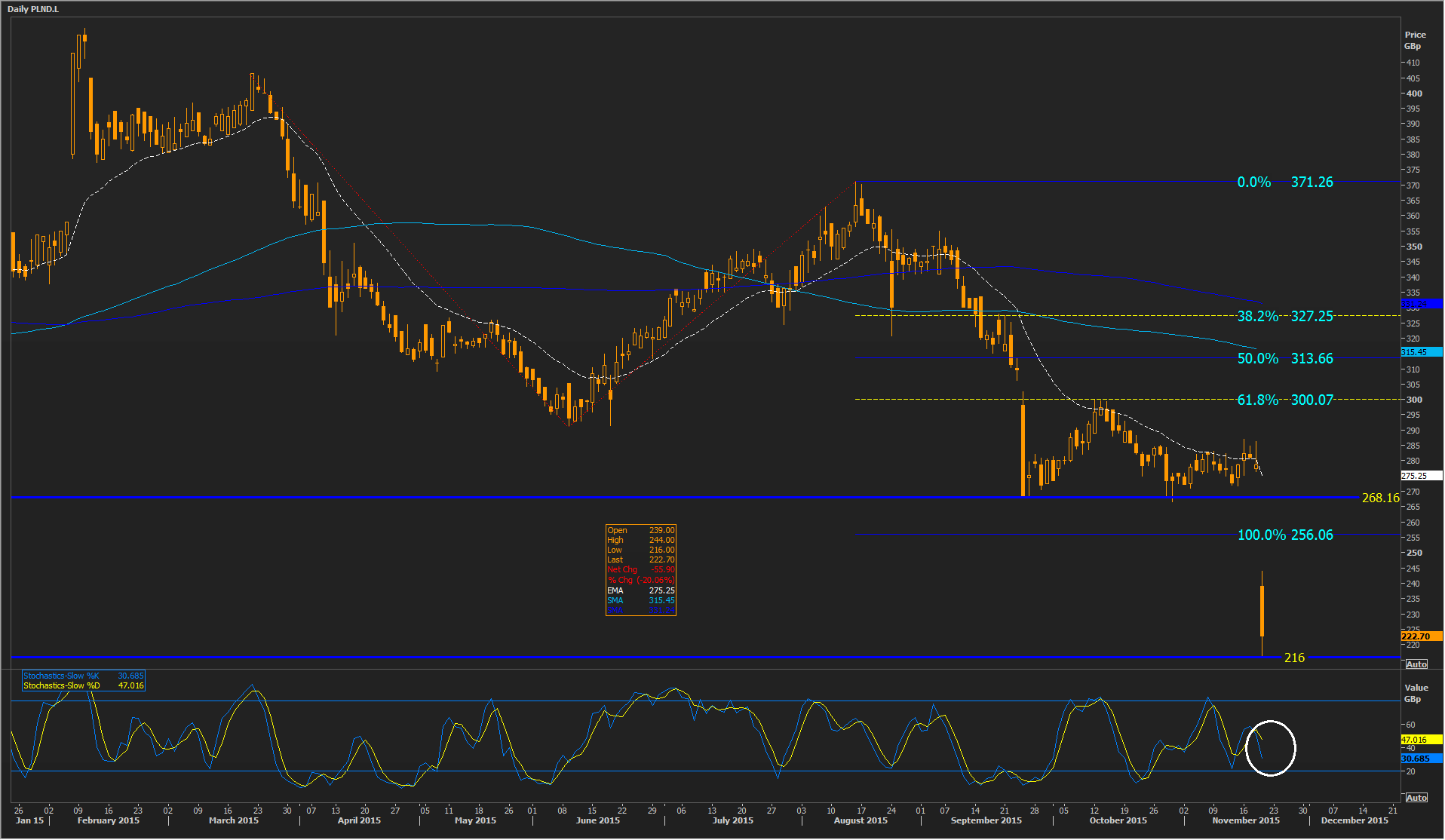

Shares of the UK’s leading ‘single-price’ retailer set a new floor at 216p after half-year profit dipped 26% to £9.3m.

(IPO share price: 355p).

Cheap and cheerful as they are, the Lidls and Aldis of the discount world are not hamstrung by a business model that pretty much bakes-in the price of most items.

Poundland, founded in the West Midlands in 1990, is also still struggling to shake-off a down-at-heel image which high-profile German rivals dispensed with years ago, enabling them to attract more affluent clientele.

An exasperated Jim McCarthy, Poundland’s CEO, has evidently heard this criticism one time too many.

On Thursday he hit back against a related ‘misconception’; that as the economy continues to recover, customers will shop elsewhere.

In other words, the ‘£1-per-item’ model is unsustainable.

A quarter of Poundland’s UK customers are from the more affluent “AB” demographic, McCarthy countered.

And to be fair, at 25 years old, Poundland is a relative youngster, in single-price.

The US’s Dollar Tree has been trading on the same business model for more than 60 years.

Japan’s Daiso for over 40.

That’s all well and good.

Just don’t tell Poundland’s CEO the proportion of wealthier shoppers at Aldi and Lidl has risen about 200% in the space of 10 years.

Research by consultancy Him!, published in The Grocer magazine in March, found 31% of shoppers at the cut price upstarts were “AB”.

In 2005, only 1 in 10 of this group would deign to step into a Lidl.

The pace of discounters’ growth therefore continues to present long-term challenges for Poundland, though the shorter-term is no less dicey.

PLND is still in the throes of integrating perhaps the biggest acquisition ever seen in the UK discount space, after buying 99p Stores for £55m in September.

The desperate chase of market share, scale and volume—a must for any sort of growth on its typically tight margins—continues to come at a cost.

Poundland opened 55 stores in the UK and Ireland in the six months to 27th September, against 34 in the same period a year ago.

A late Easter that didn’t fall in its last half year, and the kiddies’ ‘loom band’ (!) craze that boosted the comparable half, were also factors, it said.

But the market seemed to most dislike Poundland’s explanation for like-for-like store sales slipping 2.8%.

This performance—worse than recent trading at most established retailers—was due to “volatile” conditions in the run up to Christmas.

There’s a developing notion that widening adoption of US-style ‘Black Friday’ promotions in late November has mutated more typical UK pre-Christmas shopping.

“It is a shape that we haven’t seen before,” McCarthy said, noting other retailers were experiencing similar.

But of course, the complaint didn’t stop him from falling back on this year’s Black Friday to project when Poundland trading would normalise.

Thursday’s punishment of the stock by as much as 23% shows shareholders’ patience is thinning further, with the fall for the year now close to 50%.

After all, PLND’s 21 times forward rating is still rich against closely matched retailers, including Sainsbury’s at 11.6 x.

The current UK No.2 pays a far better 4.3% yield than the discounter.

Closer still, B&M European Value Retail, which trades as B&M in its Northern England home turf, achieved an operating margin of 6.3% in its last full year against Poundland’s 0.3%.

Although lower key, B&M is currently expected to grow faster too, shares are rated at 26 times EPS forecast for 2016.

Despite the above, Poundland’s share fall into uncharted waters does make it less unattractive than before, by default.

Even if momentum (see sub-chart) suggests the downswing isn’t quite exhausted yet.

Please click image to enlarge

Any takers will be those who those who take Poundland at its word, once again.

To quote from the company’s statement in November 2014, it is “dependent on delivering a good Christmas”.