Poundland sales hit 1bn but shares still can 8217 t break free

Updated 1349 BST Poundland Group has passed a milestone by ringing-in about a billion of its eponymous sales in one year. Europe’s biggest ‘single-price’ discount […]

Updated 1349 BST Poundland Group has passed a milestone by ringing-in about a billion of its eponymous sales in one year. Europe’s biggest ‘single-price’ discount […]

Updated 1349 BST

Poundland Group has passed a milestone by ringing-in about a billion of its eponymous sales in one year.

Europe’s biggest ‘single-price’ discount retailer said on Tuesday it now expects to fulfil full-year profit expectations helped by a surge in fourth quarter sales that bumped annual revenues over the £1bn mark for the first time.

Analyst consensus compiled by Thomson Reuters places average pre-tax profit for 2014-15 at £44m.

Poundland this morning said it expects FY 2015 underlying pre-tax profit to range between £42.0m and £44.6m.

However, despite good operational prospects for the year ahead, the group has also been presented with its first stumbling block of the New Year too.

Last week Poundland was informed by the UK’s Competition and Markets Authority (CMA), the main business competition watchdog, that it should be ready to sell a number of stores in order for its proposed £55m deal to buy rival, 99p Stores Ltd., to be approved.

The CMA said the deal, which would add as many as 251 further stores to Poundland Group, could reduce competition materially.

Poundland would face an enhanced investigation unless acceptable undertakings were offered by 16th April, the watchdog said.

Poundland said on Tuesday it would make an announcement in due course.

PLND’s business model relies primarily on scale in store space in order to provide margin viability, so any threat to increased space could potentially be significant.

If Poundland’s gross revenue performance in the fourth quarter is anything to judge by, its top line growth trend shows that few chances can be taken with its business model.

This is why we expect the company to expedite compliance with the UK competition authority in order to get the 99p Stores deal done.

In fact though, PLND’s dependence on store space expansion is symptomatic of wider threats and risks it faces from an intensely competitive environment and its particular business model.

PLND appears to be constrained by its business model (and to an extent, even by its name).

These have tended to limit its flexibility and adaptability amid volatile consumer trends, placing hurdles in front of its margins.

Such straits are compounded by Poundland’s image problem: Poundland shops do not appear to be places at which aspirational classes and the well-heeled are prepared to shop at frequently, if at all.

The same cannot be said, nowadays about rivals on Poundland’s grocery side, like discount supermarket chains Aldi and Lidl.

The latter two especially, have made great efforts over the last few years to portray themselves as important components of the average weekly shopping routine for consumers who must make dwindling pay checks go further, but who have become savvier about sleuthing-out value using the Internet.

That seems to place Poundland in the disadvantaged position of facing threats on two broad competitive fronts.

It is not only occupying the same space as the ‘hard discount’ grocers, but also looks prone to forays onto its territory by battle-hardened established supermarkets, which tend to have deeper resources.

Poundland referred in its trading update to ‘tough trading conditions’; an acknowledgement perhaps that established grocers’ ‘investments in margin’ are starting to bite.

For instance we note Morrisons’ gross operating margin slackened 0.5% into the red in its previous fiscal year, the weakest among any listed UK supermarket.

MRW is unlikely to let this situation continue. But the negative margin still demonstrates how aggressive on price Morrison and no doubt the larger supermarkets can be if necessary.

Poundland is also competing directly with Tesco on operating margin with both booking 3.4% on that metric in their fiscal year before last.

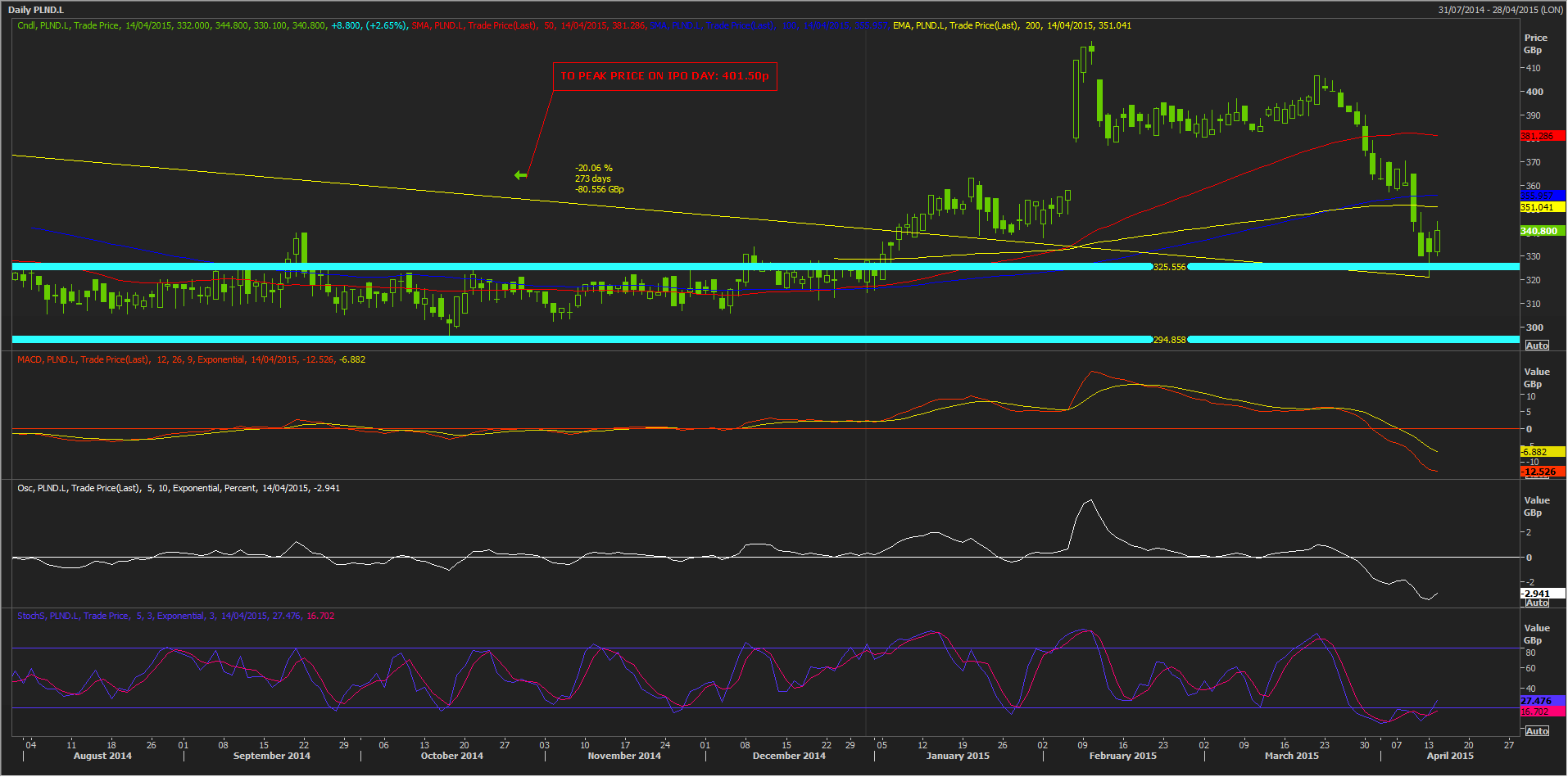

I believe margins and consumer appeal are the broad factors that have pressed on Poundland’s share price since its IPO a year ago leaving the stock still about 20% lower.

Is there any compelling reason to see the shares any higher than the band which they seem to keep reverting to as if it’s magnetic?

I’m not convinced.

It might be that vague hints from The City about consolidation in the sector may have played a part in pushing Poundland stock up almost 4% by early afternoon on Tuesday.

Ironically, the price looks oversold in the daily timeframe, although, strictly speaking a stochastic indicator has not yet presented ideal conditions to re-enter the trade.

Simpler momentum studies (Oscillator, MACD) show underlying market support is at low ebb although could be verging on a turn.

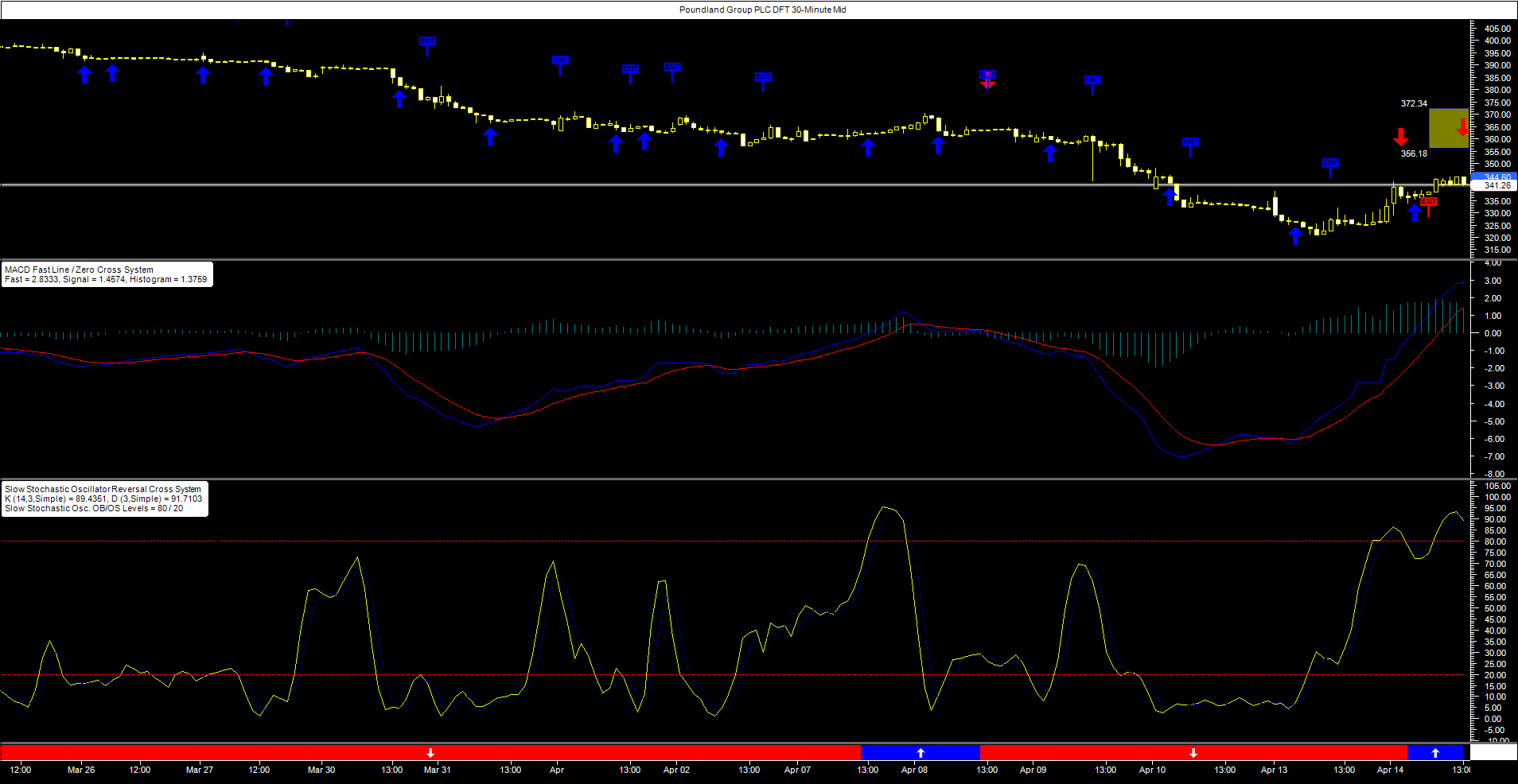

Shorter-term, as this article is updated for the afternoon, City Index’s Poundland Daily Funded Trade was looking increasingly overbought.

The Slow Stochastic trading signal signalled at 1030 GMT that short positions should be closed.

But sure enough, stretched upside in the half-hourly time frame, also shown in Moving Average Convergence/Divergence, triggered another ‘sell’ from the Stochastic Oscillator within the 1300-1330 BST interval.