Some rivals are beginning to look more credible

Growing support for Boris Johnson among Conservative MPs voting for a new leader has been confirmed after he extended his lead in a second ballot. As such, the pound remains close to its latest five-month lows on rising risk that Britain could face a chaotic exit from the European Union, with Johnson refusing to rule one out.

Still, sterling has staged modest rallies against the euro and the dollar on Tuesday. The pound regained a bid in the wake of the ballot results, resuming a 60-pip improvement versus the euro that began in Asian hours. Sterling also edged back higher against the greenback to slightly extend its small bounce off lows to almost 60 pips. These moves are obviously modest, but they hint at a return of some stability—perhaps even optimism—after sterling’s 2% tumble this month.

Here are a few takeaways from the second leadership ballot that may point to why:

- Boris Johnson extended his vote to 126 vs. 114, but the rise was not so much to make him a complete shoe-in

- Rory Stewart, widely perceived to be the only remaining outsider, paced Home Secretary Sajid Javid by 4 votes, securing 37. Stewart has been the least willing to promote a no-deal Brexit

- Former Brexit secretary Dominic Raab was eliminated, after receiving 30 votes, the lowest count. He indicated in recent days that he would suspend Parliament if necessary to ensure Brexit occurred

- His exit reduces the risk of crashing out in the worst way possible. It may also reduce the tendency of remaining candidates to tack in an even harder Brexit direction

- Michael Gove, Environment Secretary, won 41 votes, ceding little ground in third place for the second time against Secretary of State Jeremy Hunt, who won 46. Gove would be prepared to delay Brexit again and for as long as necessary to get a deal over the line

Even so, probabilities still weigh heavily against Boris Johnson’s opponents. Further possible drop outs, who might back him, as happened with Matt Hancock, would improve his odds even more. It would take an almost entirely unforeseeable mishap on Johnson’s part to prevent him making it into the final two. On that basis, any pound rebound based on UK politics is likely to remain sickly. The Federal Reserve statement and press conference on Wednesday offers better opportunities for sterling to break higher. There are decent chances that the Fed will disappoint the market’s huge hopes of easing, which see up to four cuts by the end of the year, with the first in July.

Chart thoughts

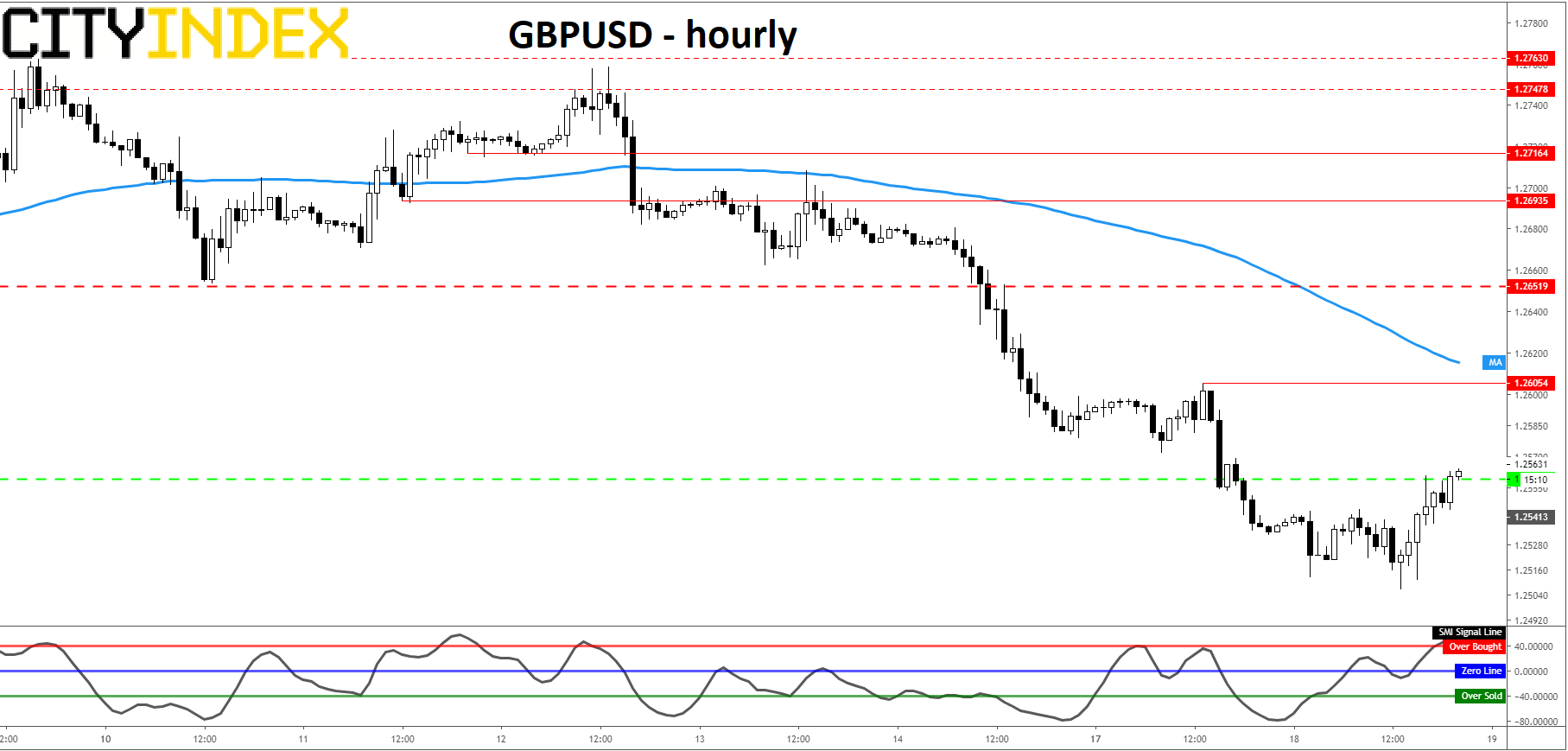

The pound against the dollar must soon confirm the viability of its $1.2556 breach by pulling away fast. Assuming GBP/USD holds above $1.2556, Wednesday’s Asian selling should bring the first test of the bounce’s momentum depending on how quickly sterling heads to almost $1.26 dead, Monday’s non-committal swing high. Indicators are stacked against the rate. Cable has adhered to stochastic prescriptions rather well of late and is overbought by such oscillators in hourly intervals. There’s no doubt the bias is towards selling and failure to reach even marginal near-term endpoints would confirm it.

Sterling/U.S. dollar – hourly

Source: City Index

Latest market news

Latest EUR articles

April 13, 2024 08:00 PM

March 25, 2024 02:55 AM

January 22, 2024 04:19 AM

January 18, 2024 04:46 AM