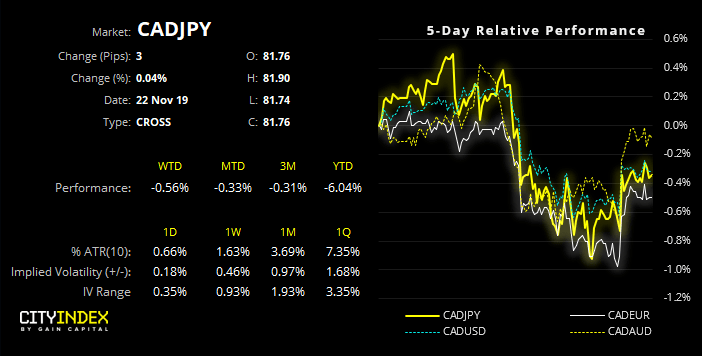

Failing to back up his colleague, CAD bears closed out after Poloz gave his neutral stance. Given the dovish remarks by BOC’s Deputy Governor Wilkins earlier in the week, all Poloz had to do was vaguely back them and we’d have likely seen a much weaker Canadian dollar. Only he didn’t. Instead, he diverged from Wilkins and said that monetary policy as “about right". Naturally, this saw the Canadian dollar strengthen which changes the picture over the near-term and could provide mean reversion for traders to capitalize on.

On a personal note, I suspect BOC will indeed shift towards a dovish narrative (or at least less neutral) over time, but yesterday was not the day. Therefor the analysis is bullish on CAD over the near-term only, which can be reassessed as data unfolds.

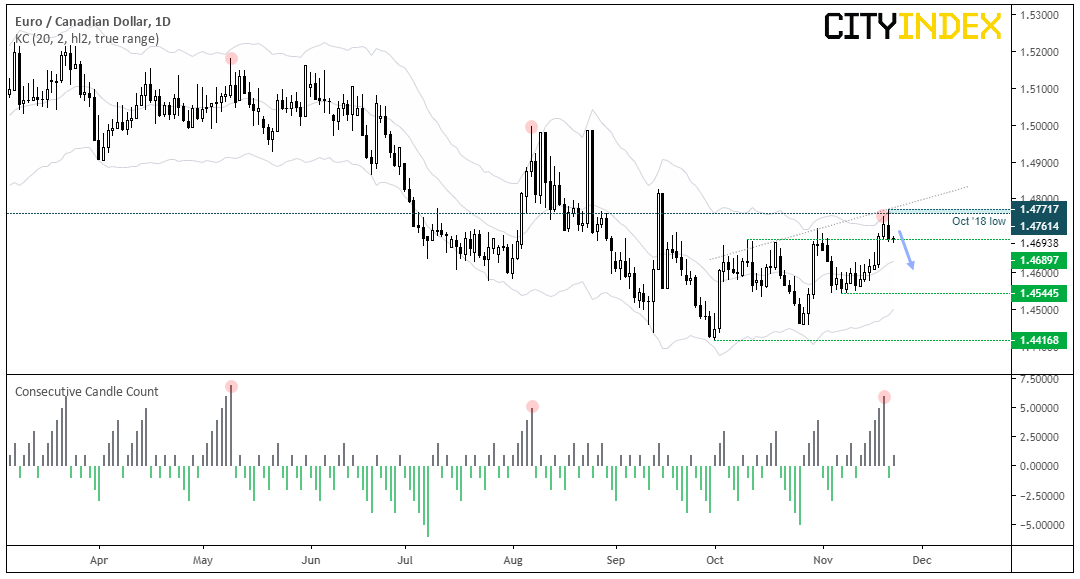

EUR/CAD: Ahead of Poloz giving his talk, the cross was teasing a break above the October 2018 low. Yet resistance held and the day closed with a bearish outside day at the highs. Given this also respected a rising resistance level and it tested the top of the upper Keltner channel, we suspect an interim top is in. Also note that we saw a 6-day rally ahead of yesterday’s bearish outside day which also suggests prices need to at least retrace, if not reverse.

- Bias remains bearish below 1.4772.

- Bears could look to enter a break beneath today’s low (as this also taken it beneath 1.4690). Alternatively, they could fade into rallies beneath the October high if convinced the top is indeed in.

- Targets include the 20-day ~1.4620 and the 1.4545/50 low.

- Keep an eye on European PMI data and Canadian retail sales. A miss from Euro PMI’s and strong Canadian retail sales would be constructive for the near-term bearish bias.

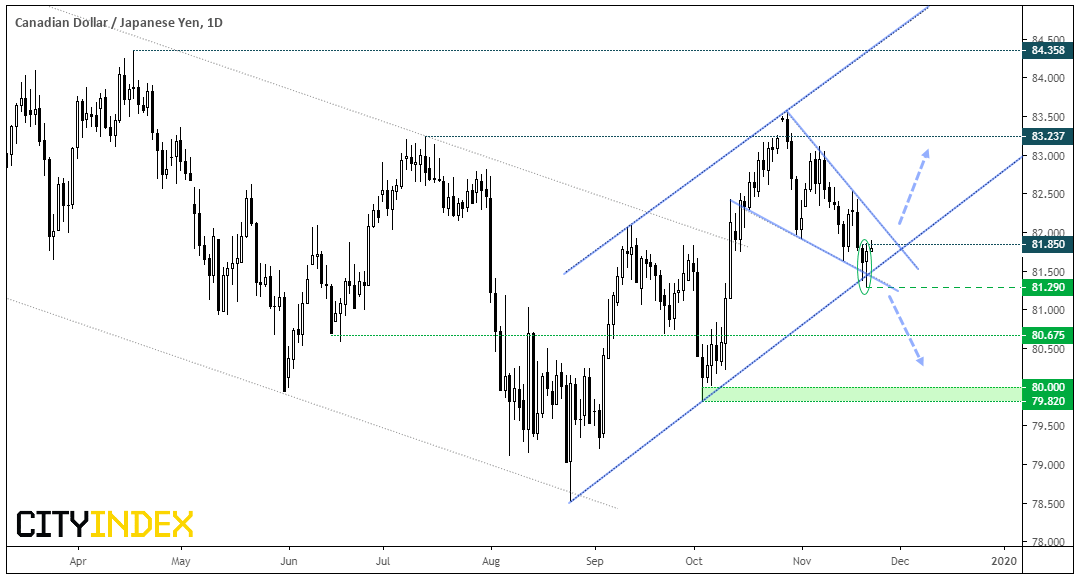

CAD/JPY: This pair very much remains in the hands of how well US-China relations are perceived to be. Trump is expected to sign the HK Democracy Bill which could put further strain over their relations and, therefore, trade talk progress.

Technically we remain neutral but here are the scenario’s which could see a decisive break in either direction.

- Bullish: Strong Canadian retail sales, Trump doesn’t sign the HK bill and trade talks are on track to eb signed sooner than later. Technically, we’d look for the bullish channel to hold and break out of its bullish wedge and head towards the base around 83.50. Note the two bullish hammers at the lows which shows a hesitancy for this to break lower, for now.

- Bearish: Weak Canadian data, Trump signs the HK bill and trade relations deteriorate yet again. A break beneath the two hammer lows would also invalidate the bullish channel and bearish wedge. Bears could target support around 80.68 and the lows around 80.

NZD/CAD Update: Whilst the bias for the cross to eventually push higher, it appears poised for a correction over the near-term following yesterday’s bearish engulfing / key reversal candle. Prices are currently testing 0.8500 and it looks like support could give way. However, whilst the 0.8430 low holds (bullish engulfing candle) we’ll monitor its potential for a higher low.

Related Analysis:

Bank of Canada Governor Poloz Makes It Clear where the BOC Stands

Wilkins Lays The Groundwork For BOC To Ease | AUD/CAD, NZD/CAD

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM