A lack of major fresh Brexit developments gifts sterling breathing space

With the biggest single parliamentary party out at conference there was always the chance that Brexit machinations would pause. Salacious details and highly conditional fiscal projections aside, a break is what the markets have got. It translates to a gap in the ‘headline impetus’ that’s been sterling’s chief driver for many weeks. That’s allowed the pound to drift somewhat higher from Friday’s almost 3-week bottom. Yet volatility implied by one-to-six-month options trades is only moderately down from the third-highest levels of the year, reached earlier in September. So speculative and hedging activity remains consistent with the expectation of further pound gyrations before too long.

After all, nothing has changed in Parliamentary mathematics that keep the government hamstrung whilst preventing a move towards a deal capable of winning Commons support. Chances that MPs may use their recently affirmed supremacy to take more direct control also remain remote. Formation of the type of ‘unity government’ needed in the event that the government is toppled by a no-confidence motion would be “impossible”, if headed by Labour’s Jeremy Corbyn, noted Dominic Grieve. He was among 21 Conservative MPs expelled from the party this month. For his part, Corbyn hasn’t deviated from a stance that ‘no-deal’ must be taken off the table before an election is triggered.

Johnson remains adamantly against an extension, though avoided confirming, at the weekend, that he would resign rather than seek one, a less drastic option than being ‘dead in a ditch’, which he infamously declared he’d prefer earlier this month. Downing Street has flagged the end of this week for when it will present more detailed alternative Brexit deal proposals. EU officials last week hardened the tone of complaints about a lack of engagement from UK negotiators, implying that any concrete plans will need to go the extra mile to be deemed cogent.

Before or after these arrive, could Boris Johnson’s private life provide the necessary spark to bring a quicker culmination? Well Monday’s sterling trade looks far less intriguing than allegations about the PM, so the answer is probably ‘no’. At least not whilst The Conservative’s base maintains pragmatic support for the PM. Polling is another clue. An Opinium/Observer poll over the weekend put the Tories 12-points ahead of Labour, broadly stable since the Conservatives regained their 2019 lead in May, having ceded it to the opposition for a couple of months. Additionally, BoJo disapproval ticked up to 43% from 41% last week. So for all the lurid headlines, neither the Conservative Party nor most voters appear much more concerned than they already were at the start of the month.

As such, a raft of leading economic indicators coming this week appear more likely to kindle short-term swings in the pound than Westminster events.

Key UK macroeconomic releases this week

Source: Bloomberg/City Index

The Conservative Party conference ends on Wednesday.

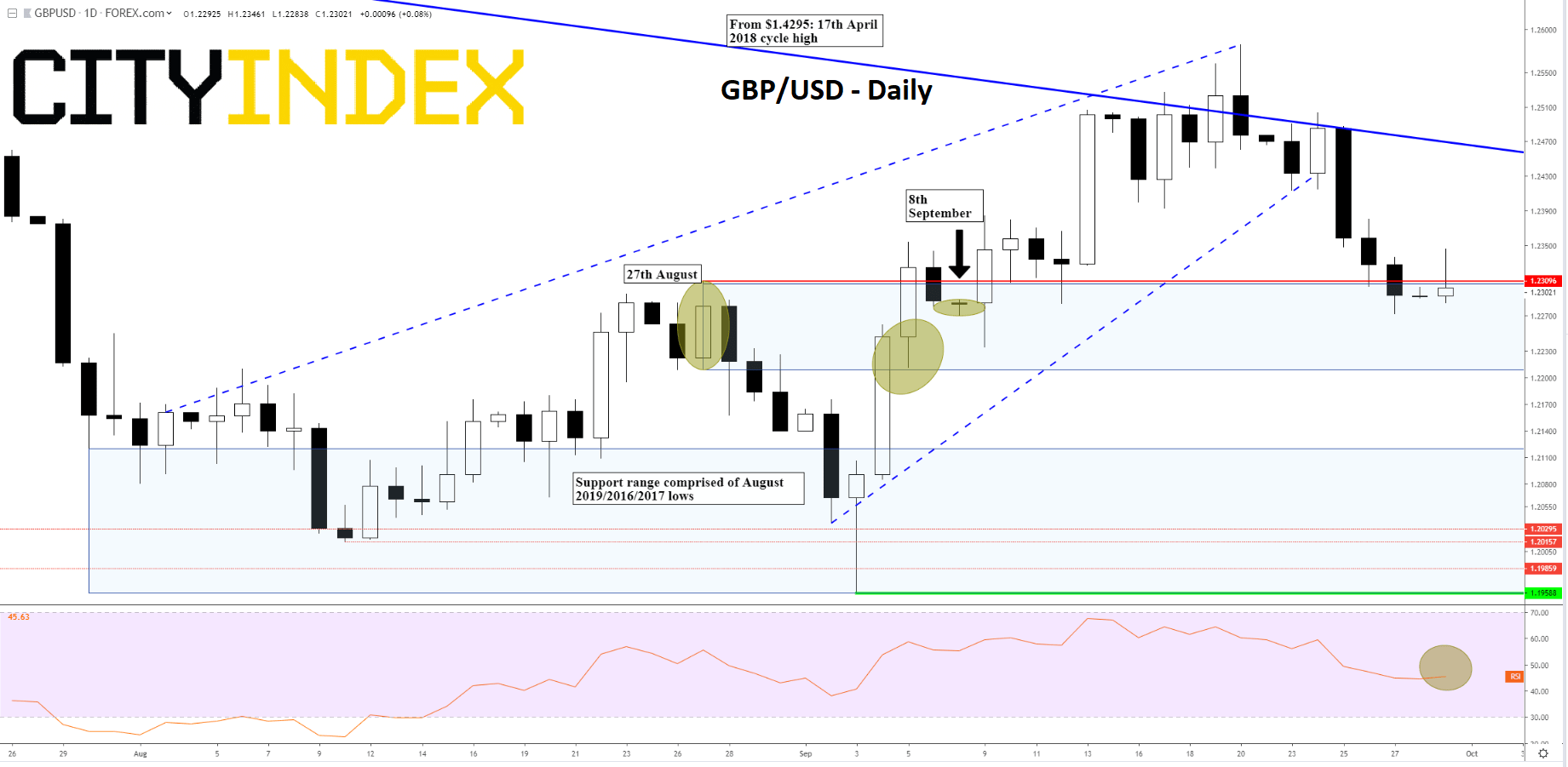

Chart thoughts

The year’s downtrend remains very much intact after the pound’s worst week since early August, with a 1% slide against the dollar. True, the pound retains around half of its 5.2% ramp off virtual 34-year lows between the start and the middle of this month but the up leg that topped at $1.2583 on 20th September is immaterial for the broader picture.

- Diagonal line bisected on 19th and 20th September falls from GBP/USD’s cycle high on 17th April 2018. Now poses resistance.

- Price has been forced back into a band of support. (Range: 27th August swing high circa $1.2310 to 27th August low c. $1.2210

- Range has broken but was tagged as support on 5th September near $1.2210 low, with subsequent bounce

- Momentum, signified by flattish RSI, is neutral

- But break of wedge/pennant continuation pattern break last week keeps bias to the downside

- Possibility of a return to August lows; near multi-year bases seen during 2016 and early 2017

GBP/USD – Daily

Source: City Index

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Sterling articles

March 29, 2024 10:00 PM

October 7, 2022 08:58 AM

October 7, 2022 08:58 AM

March 5, 2020 04:13 PM