Perform Group offered a sporting chance

Perform Group Plc. has not been living up to its name particularly well on a share-price basis lately. This has left the provider of sports […]

Perform Group Plc. has not been living up to its name particularly well on a share-price basis lately. This has left the provider of sports […]

Perform Group Plc. has not been living up to its name particularly well on a share-price basis lately.

This has left the provider of sports video and data, and owner of sporting event rights with quite a dilemma.

It doesn’t want to give Access Industries, the conglomerate holding company that made a bid of £702m earlier this week, the impression it will sell out on the cheap.

On the other hand, Perform looks to be steadily running out of options: the bid values the group at a little more than 2.4 times book value, yet the company has traded at the same 2.4 ratio in price-to-book terms for the last twelve months, without having paid a dividend.

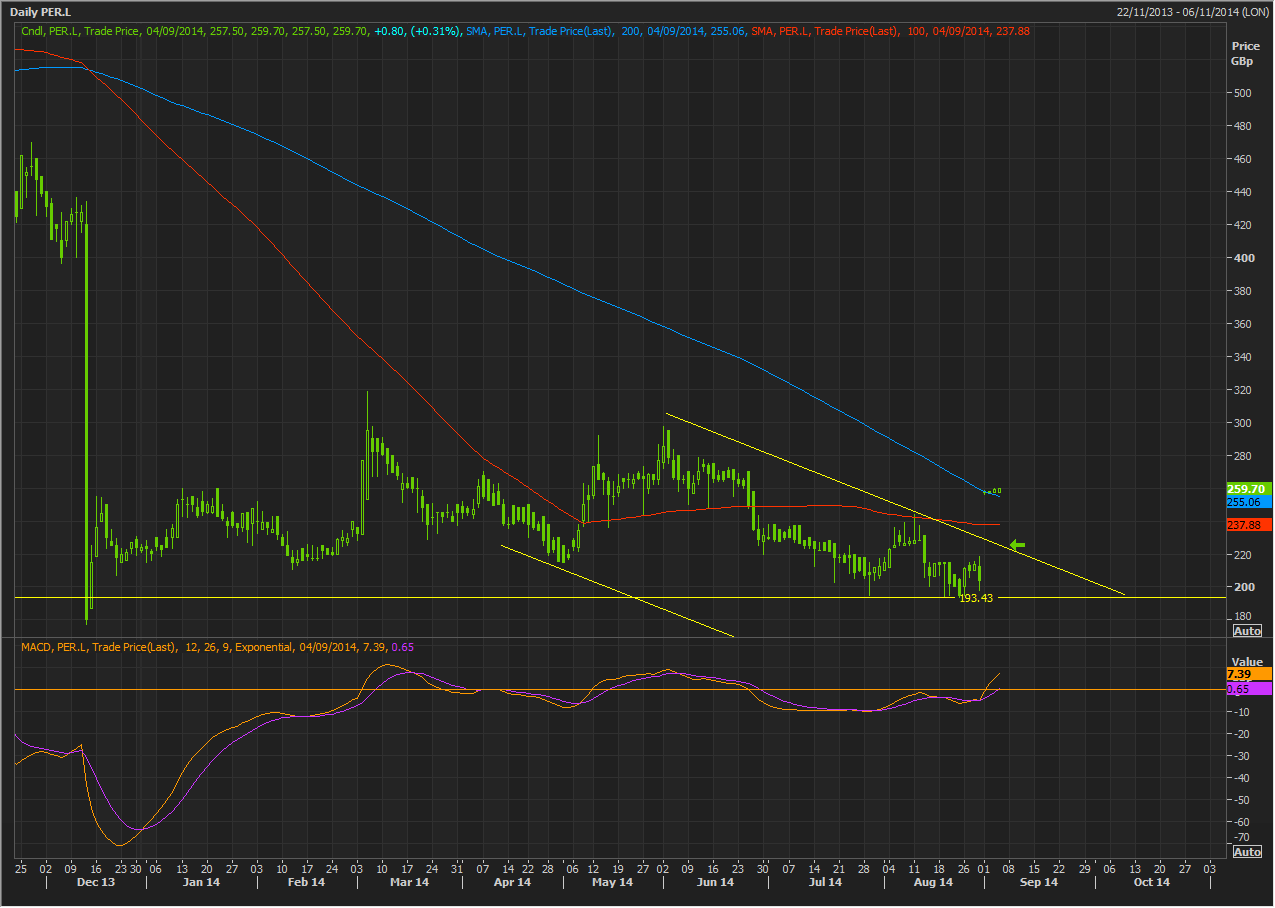

Perform Group’s shares gapped more than 18% higher following news on Monday this week (1st September) of a bid from privately held Access Industries.

But the chart makes clear the massive hit Perform shares took in December, losing 57% on 12th December alone, after it warned full-year revenues would be about £6m lower than previously forecasted.

Access Industries is owned by American businessman Len Blavatnik, also the owner of Warner Music, and already the holder of 42.5% of Perform.

If the Blavatnik wins sufficient support from Perform Group shareholders, his offer will effectively take the group private and the shares will be delisted.

Blavatnik has devised an offer that, at 260p per share, a premium of almost 28% versus Friday’s closing price, can either be described as generous, or at worst, the most shareholders can expect given the business’s current circumstances.

News reports suggest Blavatnik only made the offer because he is effectively forced to by Takeover Panel rules.

Blavatnik is obliged to make an offer for the entire amount of outstanding shares, instead of increasing his holding to 50%–reportedly his original intention.

In any case, Blavatnik will only need acceptances from the equivalent of 7.5% of shareholders to control the 50% of the shares required to have the shares delisted, under Takeover Panel rules.

These rules seem to me to be a little moot in Perform Group’s case, after a quick perusal through its key metrics.

Let’s start with debt-to-equity.

Promisingly, this is only a modest 16.5%.

Half of Perform’s close peers are mostly above 40% on debt/equity and the other half well into the realms of meaninglessness above 200%.

Perform Group’s contained leverage (no doubt linked to its recent troubles) has enabled it to keep the equivalent of BBB+ in credit rating, comparing well with its peer group’s average of BBB-, according to Thomson Reuters data.

But the all-important operating margin is still a worrying 3.4% on a trailing basis and the net margin an even more precarious 1.5%.

Perform appears amongst the weakest of its competitors on a return-on-equity (ROE) basis too, returning 1.75%, whilst similarly sized Sportsworld Media Group trades on a 4.15% ROE and BSkyB (a worrying sight in the rear view mirror of any outfit the size of Perform) is on 83.01%.

Investors and shareholders should also bear in mind the quality of Perform Group’s earnings when considering whether to tender their shares.

A model based on a wide range of values assembled by Thomson Reuters gave the group a score of 35 versus the benchmark of 100 for Developed Europe, after Perform Group’s earnings 3 days ago.

Perform shows particular weakness in an ‘Other non-current liabilities’ component, which rose 21.7% in the period ending June 2014 at Perform, compared to just 0.4% on average, according to the model.

Another kink is that Perform made 18% of revenues from the same customer, in 2012, the last year for which this set of figures is available, a 2.7 percentage point increase of revenues made from the customer in 2011.

Despite all this, on Wednesday, Perform told investors to reject the approach from Access Industries.

“The board values Access Industries as a long-term shareholder and supporter of the company but has concluded that the final cash offer undervalues the Company and its prospects,” Perform said in a statement.

Access Industries does not appear to have made any further comment since, although it said on Monday its offer was final.

Overall, it very much looks like shareholders ought to judge very carefully whether any improved offer is likely before rejecting the current one.