Pearson shares spell 8216 capitulation 8217

Pearson unfortunately has underscored what many investors suspected was the folly of getting out of the media business entirely.

Pearson unfortunately has underscored what many investors suspected was the folly of getting out of the media business entirely.

Whilst not growing fast enough it was at least cash-generative and relatively stable. Instead, the group’s decision to recast itself as a pure-play 21st Century educational publisher could scarcely have been timed more inauspiciously, though some of Pearson’s troubles are also beginning to look like fumbles.

For instance, a business that is at least partly, tacitly, dependent on an inactive labour force in the states was never going to be sustainable. At some point, workers who had been opting to continue education instead of looking for work were going to switch horses, and that’s what happened. The resultant 30% slide in quarterly education revenues is perhaps more than management could have been expected to foresee. But investors can rightly question the effectiveness of the group’s self-help measures, assuming it showed much foresight at all. Investors will also struggle to see how the threat from the second-hand and rental course market was a new one.

Further bumps in the road back to a sustainable U.S. education business had always been inevitable, given well-flagged disruption from the move to digital delivery. Even so, the £180m profit ‘miss’ now expected in the group’s forthcoming financial year is alarming–implying the return of profitability to levels last seen more than a decade ago. Market forecasts had been creeping below official guidance for months, but the operating profit downgrade implies investors were still more than 70% wide of the mark.

Further underlying concerns are exacerbating the punishment of Pearson’s shares on Wednesday, and suggesting that the stock is not quite at a floor yet. These include confirmation that the dividend, which has looked at risk of going ‘uncovered’ since final quarter of 2015, will need to be “rebased”, and that the stake in Penguin could be sold into a buyer’s market.

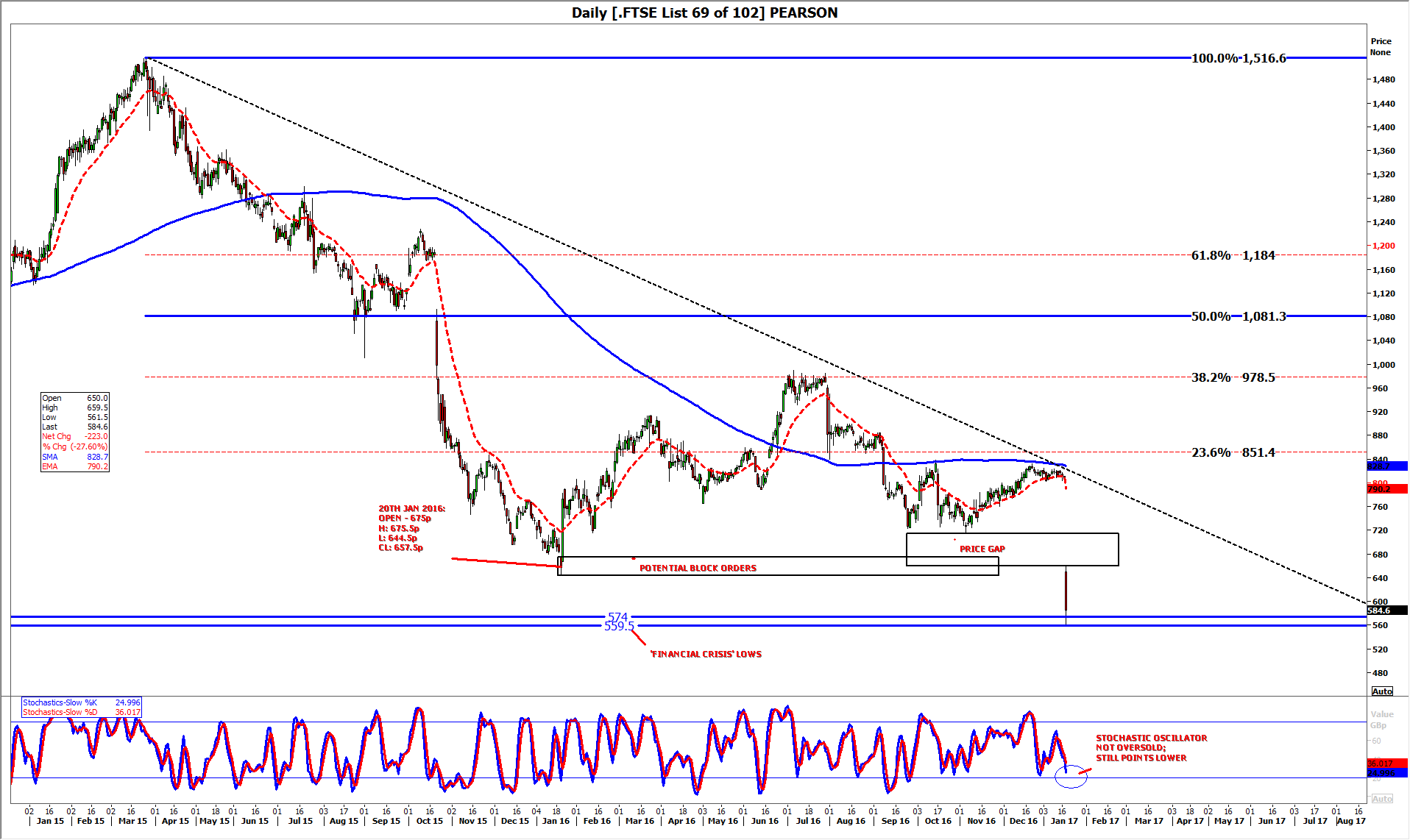

Few investors will doubt that another tough year for the group is now in the offing after the stock completely erased gains made into the middle of last year. Unfortunately for investors, prices around 400p, last seen at the turn of the previous decade, are beginning to beckon.

On balance, whilst traders would normally expect shares to naturally gravitate to a ‘gap fill’ within a fairly short space of time, in Pearson’s case, stochastic momentum isn’t helping. It is significant that the oscillator has not yet reached its oversold boundary (normally regarded as lying beyond the ’80′ level) despite the shares seeing their biggest ever one-day tumble.

Logically, there is a probability that prices could soon bounce, but at the time of writing, ‘financial crisis lows’ between c. 575p-560p—seen during December 2008-July 2009—were too compelling.

Traders should also note that price action at the beginning of last year revealed what may be signs of the market structure of Pearson’s predominantly institutional shareholder base. Keeping in mind the assumptions that only orders by the largest shareholders (in large blocks) can move the market, and that these purchases will tend to be at lows, we can see that the stock swung higher on 20th January 2016 following a decline throughout most of the year before.

PSON then went on to advance more than 50% to highs around 990p in July before again declining. Until Wednesday, at least the fall had been orderly. Today’s near-crash of as much as 30% careers well past the zone in which we suggest Pearson’s biggest buyers got on board at the end of last year.

The word ‘capitulation’ has been bandied around on Wednesday, though in reference to the company’s traditional business model for the supply of educational materials in the U.S. We think the term is just as apt for some shareholders too, and suggest that the price collapse today reflects that aspect of psychology for a big chunk of shareholders.

If we are correct, the powerful downtrend in Pearson’s shares will almost certainly lead to a breach of the 575p/560p support zone, absent a great deal more certainty from the group about what level of profitability can be salvaged over the next two years. Such clarity will necessarily take some time to achieve.

Bearish orders are likely to have replaced those buying orders we mentioned between 657p and 675.5p, and we expect that range to cap any attempted recoveries until increased certainty about Pearson’s outlook is forthcoming.

Source: Thomson Reuters; please click image to enlarge