One chart that explains the pound s decline

While Theresa May’s speech is hogging the limelight and being blamed for the sharp decline in the pound at the start of this week, it […]

While Theresa May’s speech is hogging the limelight and being blamed for the sharp decline in the pound at the start of this week, it […]

While Theresa May’s speech is hogging the limelight and being blamed for the sharp decline in the pound at the start of this week, it is worth remembering other factors are also keeping the pressure on sterling.

While we wholly concur that the realities of a hard Brexit may not yet be priced in by the market, and that further downside for the pound could hinge on what Theresa May says on Tuesday, this political noise is not the only thing that pound watchers need to be aware of. From a volatility perspective politics is king, however the fundamentals for the pound are also eroding support for the currency.

Don’t forget about inflation

Tomorrow also sees the release of UK inflation data for December. This is worth watching as rising prices could also undermine the pound in the long term. The market is expecting an uptick in the annual rate of inflation to 1.4% from 1.2%. The core rate of inflation, which strips out energy and food prices, is expected to remain steady at 1.4%. However, an upside surprise in the core rate of inflation could have a more damaging impact on the pound in the longer term, compared to May’s speech.

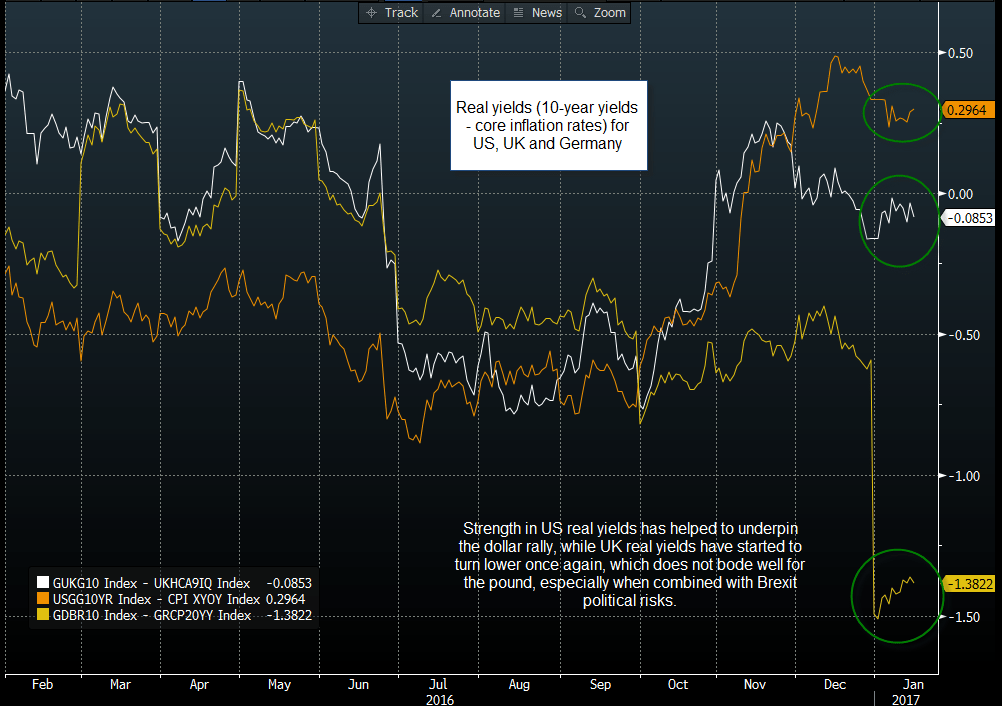

Why real yields matter for pound bears

It’s time to sit up and take notice of real yields, which are also working against the pound these days. Real yields are government bond yields adjusted for core inflation. So when inflation rises, real yields decline. The chart below shows 10-year real yields for the UK (white line), the US (orange line) and Germany (yellow line).

As you can see, the US has the highest real yield, which is underpinning the dollar rally. In contrast, the UK’s real yield is below zero, and if we get a larger than expected reading of core inflation on Tuesday, then we could see a move deeper into negative territory for real yields, which is likely to further weigh on the pound. While Germany’s real yield is by far the worst at -1.38%, it has been improving of late, while the pound’s real yield has declined, which is another reason to ditch the pound in favour of another G10 currency.

A negative outcome from May’s speech combined with rising inflation on Tuesday could be the perfect storm for GBP, and could send the currency below the flash crash lows from September at 1.1840 (according to Bloomberg prices).

Chart 1:

Source: City Index and Bloomberg