The markets have been very enthusiastic over the last few days about how the worst of the decline in oil prices is now over, how the supply surplus in the US market is beginning to clear as states reopen, and how the belo- zero prices seen at the end of April are a thing of the past. While there is some substance to the rebalancing of market story, the risks are far from over, particularly as many oil tankers off the US coast have yet to be unloaded.

Departing from its usual restrained norm, the CFTC poured cold water over the market exuberance, warning brokers, exchanges and clearing houses to be ready for crude oil prices to move yet again into negative territory. Obviously expecting a certain amount of turmoil before the WTI June contract expires on 19 May, the CFTC asked exchanges to monitor the markets and to use their emergency authority if needed to suspend trading if a contract becomes disorderly. Monday will be the highest risk day for volatility given that oil prices have risen 11% in the course of last week.

Russia, Brazil and the virus

Over the last ten days Russia and Brazil have become the new hotbeds of coronavirus with cases in Russia rising by around 10,000 per day and Brazil seeing daily increases of almost 14,000. Both economies will emerge ravaged by virus and if anything, will be tempted to pump more oil to plug income gaps. Russia has been in tight lockdown for roughly the same period of time as the US and Europe but has slowly started reopening this week and the damage to its manufacturing has been on a similar scale as in the other two regions. In April its manufacturing PMI dropped to a record low of 31.3 while services PMI sank to 12.2.

For the moment Brazil has a smaller number of cases than Russia but unfortunately a galloping death toll of over 800 per day. While Russia’s oil output will technically be constrained by an agreement with Saudi Arabia, its usual compliance rate of around 80% may end up slipping. There are no such constraints on Brazil which in January decided not to join OPEC exactly for that reason, to be able expand production at will.

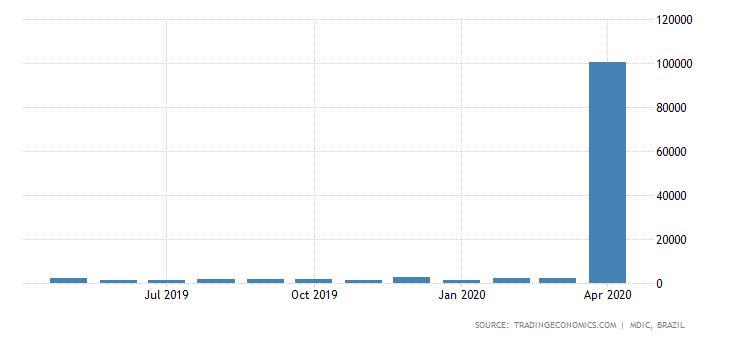

Brazilian exports of crude oil:

Source: Trading Economics

The opposite of lockstep

The American Petroleum Institute (API) oil inventory data published on Tuesdays and similar data from the Energy Information Administration (EIA) on Wednesdays each week typically move in lockstep, reflecting the weekly change in US demand trends, but that correlation diverged last week. The sudden disparity between the non-governmental API and official government data provided by the EIA has left investors wondering which of the two is showing the real demand picture. Given that oil companies are required to report their inventories to the EIA while providing information to API is optional, markets tend to place a greater emphasis on the EIA’s data. The disconnect could create some confusion next week, unless the two sets of data move back into sync.

|

When |

What |

Why is it important |

|

Tue 19 May 10.00 |

German ZEW May economic sentiment |

A proxy for the demand trend in Europe’s largest economy |

|

Tue 19 May |

WTI June Crude oil contract expires |

Expect higher volatility in the lead up to contract expiry |

|

Tue 19 May 15.00 |

Fed chairman Powell testifies before Congress |

Powell warned this week that there could be more economic turmoil on the horizon |

|

Tue 19 May 21.30 |

API weekly US crude oil stocks |

Inventory levels are still rising but the speed of increases has been slowing for the last three weeks. Last up 7.58m |

|

Wed 20 May |

Public holiday in Germany and a number of European countries |

Brent crude volumes expected to be thinner than usual |

|

Wed 20 May 15.30 |

EIA crude oil stocks change |

Last week showed a surprise decline of 745,000bbl |

|

Thu 21 May 08.30 |

Germany May manufacturing PMI |

German manufacturing should show signs of improvement as the country started lifting lockdowns. Previous reading at 34.5 |

|

Thu 21 May 09.00 |

Eurozone May manufacturing PMI |

Same as for Germany. Last reading at 33.4 |

|

Thu 21 May 13.30 |

US initial jobless claims to May 15 |

The state of the job market is a good proxy for domestic US oil demand |

|

Thu 21 May 14.45 |

US May manufacturing PMI |

Should show a slight uptick from 36.1 in April as some businesses restarted operations over the last two weeks |

|

Fri 22 May 18.00 |

Baker Hughes US oil rig count |

|

|

Fri 22 May 20.30 |

CFTC oil net positions |

Changes in money managers’ net positions |

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Yesterday 08:18 AM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM