There has been a sharp reversal in the Saudi exports of oil into the US with the Kingdom seemingly turning 180 degrees over the last month. Having flooded the US market with crude oil in April and May, oil imports from Saudi Arabia have now shrunk to a minimum. During the first two weeks of June only one Saudi cargo ship reached the US, according to Bloomberg, the equivalent of about 133,00 bbl/d, or a fraction of the 1.3m bbl/d offloaded in April. This should begin to be reflected in the API and EIA weekly petroleum data on Tuesday and Wednesday, but more importantly it will trigger a significant change in stock levels from mid-July onwards. It takes 45 days for Saudi tankers to reach the US and barely any have left the country this month.

Combine this with a return in domestic transport demand to almost 80% of the pre-corona levels, and rising, unless the process gets stalled by the new outbreaks in the Southern states, the supply picture towards the end of July will be significantly different from the present oversupply.

EasyJet earnings

Budget airline easyJet will report its results on Tuesday. Unlike the big state flagship names like Lufthansa, British Airways-owner International Consolidated Airlines, or Air France, easyJet is unlikely to see any state support in battling with the corona-induced losses and its results will to some degree more closely reflect the reality of European travel demand.

Having in the past flown hundreds of flights into every sunny corner of Europe and the Middle East, the company resurrected only a few of the most popular flight routes across Europe on 15 June. The most interesting part of the company’s results will not be so much the actual earnings, or rather losses, caused by the pandemic, but a sense of whether the European tourist market is recovering and at what rate, particularly as the borders keep closing and opening daily. With temperatures rising in the UK and the Health Secretary threatening to close domestic beaches because of a breakdown of social distancing, Britons may have an extra reason to want to swap Britain for one of the southern European countries where the coronavirus is now already in the rearview mirror.

In the US the airline earnings calendar kicks off on 9 July with Delta Airlines.

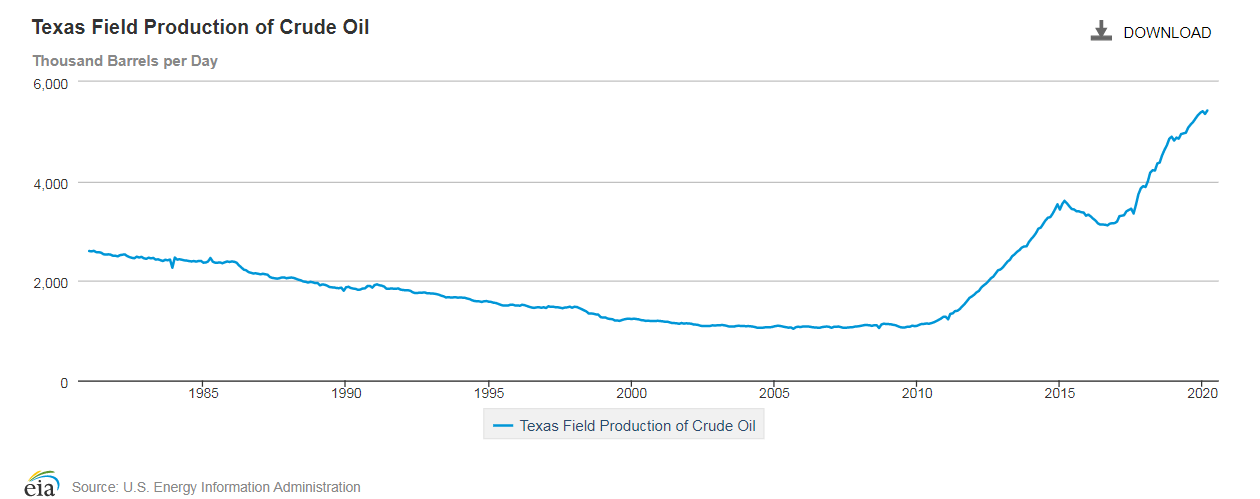

Dallas Fed Manufacturing Business Index

The Dallas Fed Texas Manufacturing Outlook Survey would normally not be a major indicator for the oil market but under the current circumstances, where the new COVID-19 case count in the state has risen to over 5,000 each day, this week the monthly outlook survey for the Texan industry will provide an insight into how much of the state’s industrial demand for oil still remains intact. The indicator, which shows changes in output, order levels and prices, is expected to have dropped to –59 in June compared with -49 in May, despite the reopening of the state in April.

Source: EIA

|

When |

What |

Why is it important |

|

Mon 29 Jun 08.00 |

Dallas Fed June manufacturing business index |

An insight into the Texas manufacturing as the spread of the pandemic picks up |

|

Tue 30 June 07.00 |

Easyjet earnings |

A proxy for European air travel demand. Look out for the company’s outlook for the summer travel season |

|

Tue 30 June 21.30 |

API weekly crude oil stocks |

Previous increase 1.749m |

|

Wed 1 Jul 02.45 |

China June manufacturing PMI |

China’s manufacturing is back to expansion mode, but only just |

|

Wed 1 Jul 08.55 |

Germany June manufacturing PMI |

German manufacturing is unlikely to show much change from May, still in contraction |

|

Wed 1 Jul 15.00 |

US June manufacturing PMI |

Manufacturing has improved from May and is expected to show a reading of 49, just below the key 50 level which indicates expansion |

|

Wed 1 Jul 15.30 |

EIA US crude oil stocks |

The weekly rises should show either a significant slowdown or even a reversal |

|

Wed 1 July 20.30 |

US total June vehicle sales |

A proxy for future transport demand |

|

Thu 2 July 13.30 |

US initial jobless claims |

Last up 1.62m |

|

Thu 2 July 18.00 |

Baker Hughes June International rig count and weekly US rig count |

A change in the weekly schedule because of Independence Day |

Latest market news

Today 08:15 AM

Today 05:45 AM

Yesterday 11:09 PM