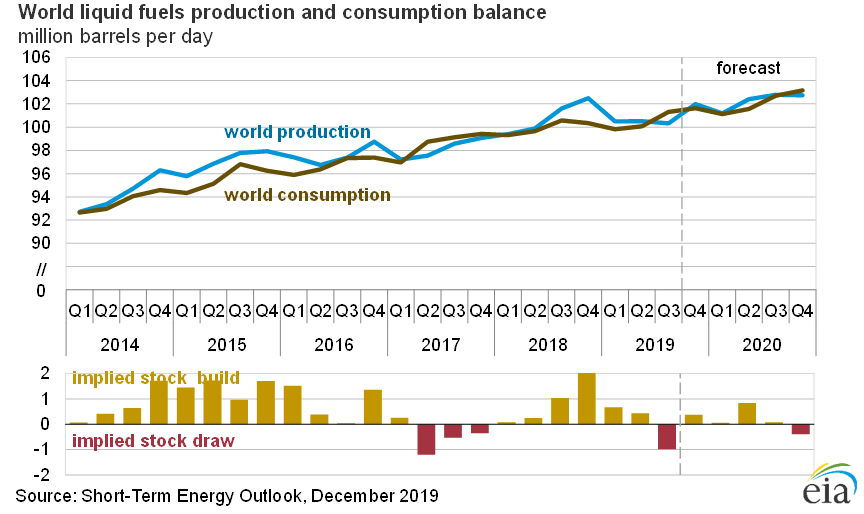

Whether the slight shift in the trade balance between the US and China over the last few months represents a sustainable long-term trend remains to be seen, but what is definite is that in September, the US - for the first time - exported more oil than it imported. These exports are contributing to an expected increase in global oil inventories likely to be the most pronounced in the first half of next year.

The US Energy Information Agency (EIA) expects Brent crude prices to be on average $3 cheaper next year at $61/bbl, and WTI prices to be on average $5.5/bbl below Brent crude prices:

|

When |

What |

Why is it important |

|

Monday 16 Dec |

OPEC Monthly oil market report |

Insight into the oil output changes from OPEC members |

|

Monday 16 Dec |

US manufacturing PMI |

Still in expansion territory, last at 52.4 |

|

Monday 16 Dec |

US housing market index |

Last at 70 |

|

Tuesday 17 Dec |

EU trade balance |

Trade data with China of particular interest |

|

Tuesday 17 Dec |

US housing starts |

Health of the US construction industry |

|

Tuesday 17 Dec |

US industrial production |

Taking the pulse of US industry, last up 0.8% |

|

Tuesday 17 Dec |

US capacity utilization |

Look out for oil industry utilization rates |

|

Tuesday 17 Dec |

API weekly crude oil stocks |

For the week ending Dec 13 |

|

Wednesday 18 Dec |

ECB’s Lagarde speech |

Ms Lagarde set out her rate policy on Thursday but any new comments about the health of the Eurozone could move markets |

|

Wednesday 18 Dec |

Germany IFO business climate |

Expectations for German business |

|

Wednesday 18 Dec |

EIA crude oil stocks |

Last at 0.822m |

|

Wednesday 18 Dec |

CFTC commitment of oil traders |

CFTC publishes the report early this week. It is normally released on Fridays. |

|

Thursday 19 Dec |

US initial jobless claims |

Insight into the state of the US job market |

|

Thursday 19 Dec |

US Philadelphia Fed manufacturing survey |

Indicator of manufacturing sector trends |

|

Friday 20 Dec |

China interest rate decision |

Rates currently at 4.15% |

Pollution rule expected to affect US refinery runs

From the start of next year, new rules brought in by the International Maritime Organization will restrict the amount of sulphur in marine fuel oil in ships and tankers from 3.5% to 0.5%. Some ships will make smaller adjustments to avoid paying for the new type of fuel, but only about 30% of the ships will be able to do that while the rest of the vessels at sea will have little option but to switch fuels.

Even with shippers attempting to avoid compliance for as long as possible, global refineries will start to increase their refinery runs to upgrade as much of their high-sulphur heavy fuel into low-sulphur distillate fuel compliant with the new requirements as possible. The knock-on effect on crude oil prices will come from higher refinery utilization rates, which typically tend to dampen oil prices. According to the US EIA, US refineries are expected to increase their refinery runs by 3% by next year to a record level of 17.5 million b/d. This would boost refinery utilization rates to an average of 93% in 2020.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM