There will be a sprinkling of mainly US and Canadian economic indicators over the next week but activity will die down in the UK, Europe and most of Asia where the festive hangover will not clear until the second week of January.

With very few economic indicators due to be published in the next two weeks, some of the key trade prompts could come from the oil producers themselves. Shell is the first of the oil majors to warn that full-year results could bring lower annual sales with the key themes being trade tensions between the United States and China, relatively limp global growth and rising output in the US. Chevron will open the reporting season at the end of January and most other oil majors will publish their results in early February

Investment themes for January:

- US-China trade negotiations: Although phase one of the trade deal has been completed, most of the punitive tariffs are still in place and are either slowing down or re-routing Chinese imports. The deal is due to be finalized in January, barring yet another setback.

- A shorter trading month in China because of Chinese New Year on 25 Jan - expect increased Chinese stockpiling ahead of week-long holiday.

- At current Brent crude prices, the fiscal deficits in several OPEC nations are widening which will not incentivise some of the smaller members to stick to production cuts.

- Following on Shell’s trading update, look for producers warning of sales declines in the coming quarter sales.

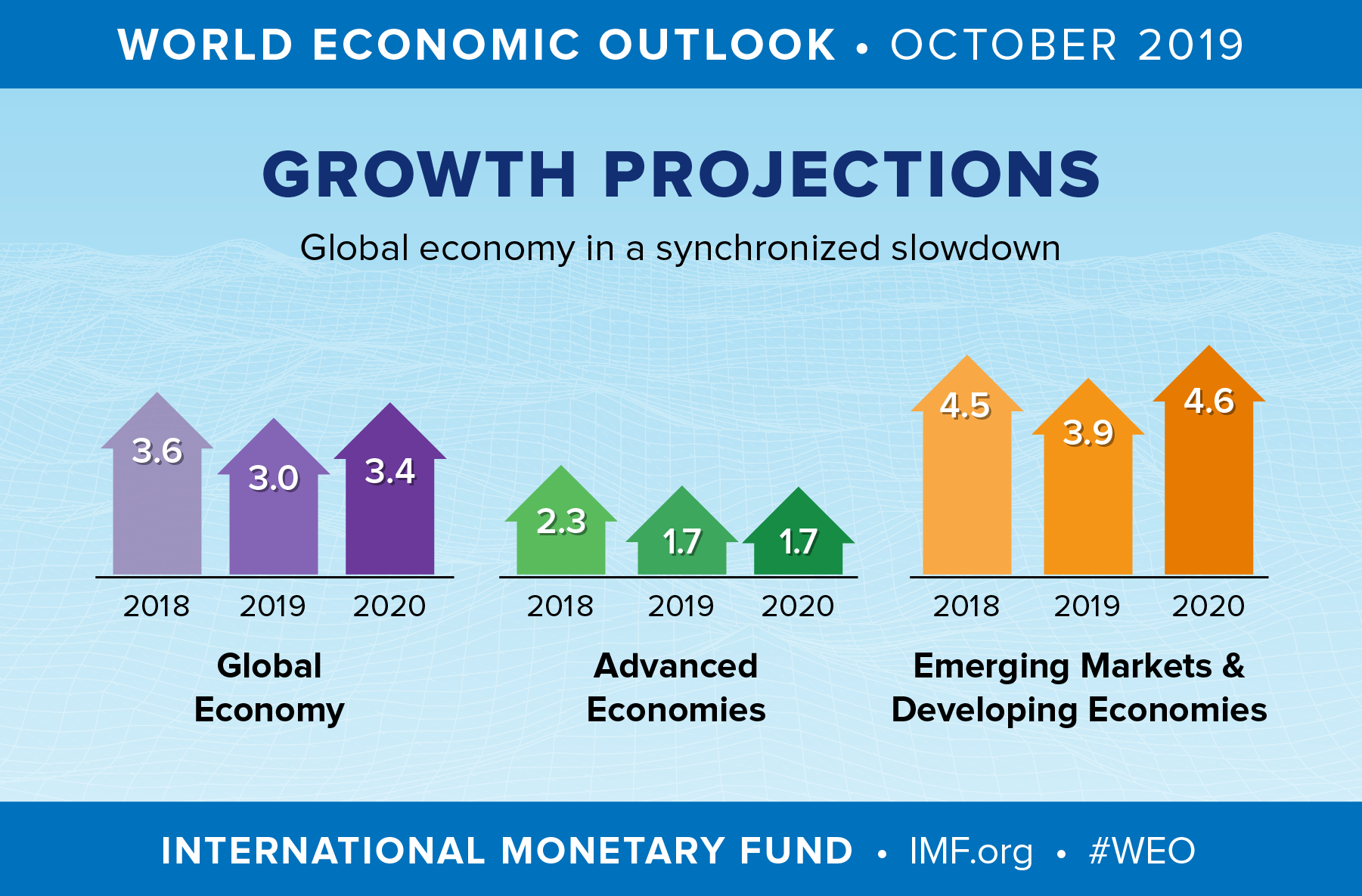

- China and US economies are expected to slow down slightly in 2020 although this will be balanced out by growth in emerging economies in South America, the Middle East and Asia.

- Twenty-two new electric cars are due to be launched in 2020, most of them in the first half of the year.

- New regulation on marine fuels starting in January will affect refinery runs

- Chevron kicks off reporting season on the 31st of January

A small increase in global growth could help demand

Now that OPEC and Russia have committed to deeper cuts for the next six months, the major driver for oil prices is more likely to come from the demand side rather than the supply side. According to the IMF, global growth is expected to pick up in 2020 to 3.4%, up from 3.0% in 2019 mainly driven by emerging markets in Latin America, the Middle East and developing European countries. At the same time, both China and the US, the two largest oil consumers, are expected to go through a slowdown. The market could remain close to a delicate balance next year because the picture for China is more complicated thanks to the ramp up of several new mega state-owned and private refineries in Zhejiang and elsewhere which will create additional demand beyond the demand related to GDP and industrial growth. China is still breaking records for crude oil imports even though its economic growth is slowing, and the country has imported 11.18m bbl/day in November.

|

What |

When |

Why is it important |

|

Monday 23 Dec |

US New home sales, November |

An insight into the strength of the US housing market |

|

Tuesday 24 Dec |

US Redbook index, December |

US sales growth |

|

Tuesday 24 Dec |

US markets close at 13.00 |

|

|

Tuesday 24 Dec |

API weekly crude oil stocks |

Last at 4.7m |

|

Wednesday 25 Dec |

Markets closed |

|

|

Thursday 26 Dec |

UK, European markets closed |

|

|

Thursday 26 Dec |

ICE crude oil trading reopens |

|

|

Thursday 26 Dec |

US initial jobless claims |

A stronger job market correlates to higher oil consumption |

|

Friday 27 Dec |

China industrial profit Nov |

Last down 9.9% YoY |

|

Friday 27 Dec |

EIA crude oil stocks |

Last -1.085m |

|

Friday 27 Dec |

Baker Hughes US oil rig count |

|

|

Saturday 28 Dec |

CFTC Commitment of traders report |

Money managers position changes |

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM