More than any macroeconomic data scheduled for next week, the tone of trading will be set by what Iran does next after the assassination of Qassem Soleimani, the head of the Iranian Revolutionary Guard’s overseas forces on Friday. Iran has already threatened some form of retribution, leaving the questions of where and when unanswered. Predictions are complicated by the fact that instead of hitting back directly, Iran may choose an ally from a network that has built up in the region, for instance using sympathetic rebel groups as it did in the case of the attack on Saudi Arabia’s key refinery complex in September.

On the question of where, most analysts seem to lean towards Iraq becoming the proxy battlefield for a conflict between Iran and the US with the former likely to try and hit US army points in the country. Alternatively, it may opt for a number of vulnerable points in the Straits of Hormuz and the Arabian peninsula. Iran may also choose to delay its response until it regroups after Soleimani’s death. The only thing that is certain is that Iran’s fury makes further clashes as good as inevitable, raising the geopolitical risk premium in oil.

It will be too early to analyze CFTC’s Commitment of Traders (COT) oil positions next week because they will reflect the position changes in the past seven days, but in the weeks ahead there could be an increase not only in outright long oil positions but also in oil hedges as the Middle East situation remains fluid.

|

When |

What |

Why is it important |

|

Mon 6 Jan 07.00 |

German Nov retail sales |

Last up 0.8% on year, down 1.9% on month |

|

Mon 6 Jan 20.30 |

CFTC Oil net positions |

Last 536,400 |

|

Tue 7 Jan 10.00 |

EU Nov retail sales |

Last -0.6% MoM |

|

Tue 7 Jan 13.30 |

US Nov trade balance |

|

|

Tue 7 Jan 15.00 |

US Nov factory orders |

Up 0.2% MoM in October |

|

Tue 7 Jan 21.30 |

API weekly US crude oil stocks |

Last down 7.8m |

|

Wed 8 Jan 07. 00 |

Germany Nov factory orders |

Last -5.5% on year, down 0.4% on month |

|

Wed 8 Jan 10. 00 |

EU Nov business climate |

Last -0.23 |

|

Wed 8 Jan 10. 00 |

EU Nov industrial confidence |

-9.2 in November |

|

Wed 8 Jan 12. 00 |

US MBA mortgage applications |

|

|

Wed 8 Jan 15.30 |

EIA crude oil stocks |

Last down 11,463 on month |

|

Thu 9 Jan 07.00 |

Germany Industrial production |

Down 1.7% in October |

|

Thu 9 Jan 07.00 |

Germany trade balance |

|

|

Thu 9 Jan 13.30 |

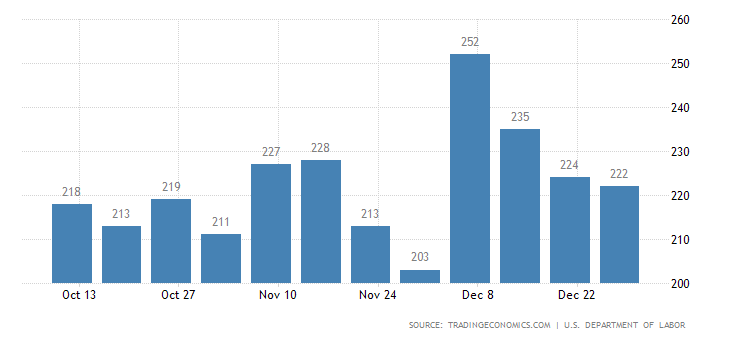

US initial jobless claims |

Last 222,000 |

|

Fri 10 Jan 13.30 |

US nonfarm payrolls |

Last 266,000 |

|

Fri 10 Jan 18.00 |

Baker Hughes US oil rig count |

Last at 805, down 278 on year |

|

Fri 10 Jan 20.30 |

CFTC oil net positions |

|

OPEC economic projections vs. real US macro data

OPEC’s supply and demand growth projections for this year are based, among projections for other countries, on the assumption that US growth will slow down slightly in 2020 to 1.8% from 2.3% last year. Trade balance data and industrial orders due out on Tuesday, mortgage growth on Wednesday, initial jobless claims Thursday and non-farm payrolls on Friday should all be analyzed in this context. OPEC has built in some space for a slowdown in demand not only from the US but also from other OECD countries when it prepared its projections for necessary production cuts.

The picture becomes more complicated if those macroeconomic numbers fall faster than expected, as was the case with US manufacturing PMI data for December. In contrast, jobless and mortgage data has fluctuated quite a bit over the last few months but has not been building up a picture of consistent decline. Instead the overall US economy still seems to be fairly healthy, at least as of writing!

Source: TradingEconomics

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM