When is a cut not a cut?

When OPEC agrees on curbing production that is already not there!

After two arduous days in Vienna, the cartel seems to have agreed to cut output by 500,000 barrels a day, which, given that OPEC has been underproducing over the last few months, will more or less just formalize the existing situation rather than meaningfully change the overall supply/demand balance. The bigger factor will be rising output in the US, Norway and Brazil which, together with a slowdown in global demand, is nudging the oil market into oversupply, expected to become more visible in the first half of 2020.

Investment banks are already putting out their commodity price forecasts for next year and most are leaning towards lower prices for WTI and Brent Crude in the first half of the year, followed by recovery in the second half. The week ahead is the last full trading week before markets start scaling down for the holidays and is likely to bring more predictions on price moves.

UK and Algeria go to polls

If the polls are right, and that’s a big if, it should be a straightforward win for the Tory party in the UK election on Thursday. The Conservatives have been generally supportive of the oil industry and permissive towards the development of the UK shale gas sector, despite fairly vocal local opposition, so a Conservative win is unlikely to bring any changes for the oil industry. However, a hung Parliament or a Labour-led majority could mean that UK oil producers will end up with a massive tax bill in the region of £11 billion for their contribution to climate change.

Thursday is also election day in Algeria where public protests against the ruling military have been becoming more vocal. The election will not provide a real choice given that all the presidential candidates have been shortlisted and vetted by the ruling army figures and once elected will become only pro-forma heads. However, this also means that any changes to the country’s oil policy are very unlikely.

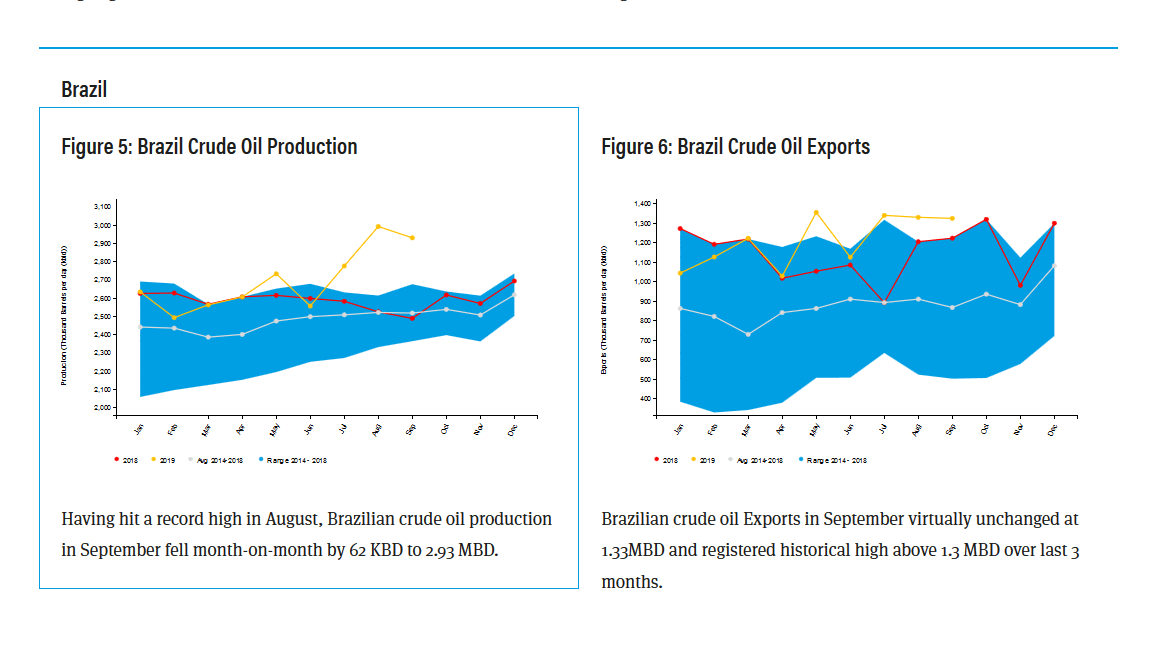

COUNTRY BRIEFING: Brazil

During Brazil’s state visit to Saudi Arabia in October, the country’s president said he was keen for Brazil to become an OPEC member, a move which, if approved, would mean that Brazil would be OPEC’s third-largest producer. The country has gone through a period of expansion between 2013 and 2018 and then notched up a gear this year when it installed eight new units in its subsalt region. The fast-growing offshore production increased the country’s output to a record 2.92M bpd in August and although that level has marginally tailed off over the last few months, it still remains close to record highs.

Understandably the oil industry has greeted the idea of joining OPEC with skepticism, saying that this was only a political move by the president that doesn’t really have merit for the industry, primarily because OPEC would likely force the country to curb its production and reign in further expansion plans.

|

When |

What |

Why is it important |

|

Sunday 08 Dec |

China trade balance |

A glimpse into effects of the US-China trade war |

|

Monday 09 Dec |

German exports |

Trend in car exports of particular interest for oil industry, particularly exports to Asia |

|

Tuesday 10 Dec |

China FDI |

An indicator showing if the trade war is eroding FDI |

|

Tuesday 10 Dec |

China CPI, PPI |

Taking the pulse of the Chinese economy |

|

Tuesday 10 Dec |

Germany ZEW economic sentiment |

A proxy for the health of the Eurozone economy |

|

Tuesday 10 Dec |

API weekly crude oil stocks |

Last down 3.72m |

|

Wednesday 11 Dec |

OPEC Monthly Oil report |

Clearer picture on latest production levels |

|

Wednesday 11 Dec |

FOMC economic projections |

Expectations for the US economy in the coming quarter |

|

Wednesday 11 Dec |

Canada Q3 Oil industry utilization rate |

Has been on the rise this year, last at 87% |

|

Wednesday 11 Dec |

EIA crude oil stocks |

Last down 4.856m |

|

Thursday 12 Dec |

UK Elections |

Not crucial for the oil market but will deflect attention away from trading. Polls are forcasting a Conservative win |

|

Thursday 12 Dec |

IEA 2020 World oil outlook |

Reflecting on carbon impact from oil production |

|

Thursday 12 Dec |

US Jobless claims |

Taking the pulse of the US economy |

|

Friday 13 Dec |

US retail sales, including cars |

Insight into future US crude oil demand |

|

Friday 13 Dec |

CFTC Oil commitment of traders report |

Changes in oil future positions by money managers and trade/hedge positions |

Into January

Once the oil markets close for Christmas, they will not be fully operational until early February as the holiday season will travel around the globe. In Russia, where Orthodox Christmas falls on 7 January and the old New Year on 13 January, the markets will remain closed for the better part of the first two weeks of 2020. Then a brief full global trading week before 24 January when China shuts down for five days for the annual Spring Festival. Looking ahead, this could mean more volatility than usual in January when thinner markets will make for more pronounced price moves.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Brent articles

February 21, 2024 03:30 PM

November 28, 2023 09:05 PM

November 20, 2023 08:26 PM

November 8, 2023 06:11 PM